Showing posts with label Global Housing Watch. Show all posts

Friday, March 16, 2018

Housing View – March 16, 2018

On cross-country:

- Mortgages, developers and property prices – Bank for International Settlements

- FT Special Report on Property Market – Financial Times

- The US homeownership rate has lost ground compared with other developed countries – Urban Institute

On the US:

- It All Adds Up: The Cost of Housing Development Fees in Seven California Cities – Terner Center for Housing Innovation (UC Berkely)

- “Sand castles before the tide”: How can America’s most expensive cities keep themselves affordable? – American Economic Association

- Student Debt vs. Homeownership – Federal Reserve Bank of Richmond

- Rising Mortgage Rates Threaten Housing Affordability and Inventory – Zillow

- The Trump Administration’s War on New Housing – Citylab

- Black homeownership rates haven’t changed much in the 50 years since the Fair Housing Act – Curbed

- With Some Homeownership Incentives Gone, Will More Americans Actually Rent? – Governing

- White Flight’ Persists in America’s Suburbs – Citylab

- Want Affordable Housing? Just Build More of It – Bloomberg

- Panel Discussion Explores Potential for Small Unit Housing in New York City – NYU Furman Center

- First-Time Homebuyer Counseling and the Mortgage Selection Experience in the United States: Evidence from the National Survey of Mortgage Originations – Federal Housing Finance Agency

- Mortgage Experiences of Rural Borrowers in the United States: Insights from the National Survey of Mortgage Originations – Federal Housing Finance Agency

On other countries:

- [Australia] The Effect of Zoning on Housing Prices – Reserve Bank of Australia

- [Australia] The Distribution of Mortgage Rates – Reserve Bank of Australia

- [Australia] Making Better Economic Cases For Housing Policies – University of New South Wales

- [Belgium] Housing Market in Belgium – IMF

- [Canada] Vancouver’s empty-homes tax might not affect as many homeowners as predicted – The Globe and Mail

- [Malaysia] Housing Market in Malaysia – IMF

- [Netherlands] Gentrification through the sale of rental housing? Evidence from Amsterdam – EconPapers

- [New Zealand] Getting the best out of macro-prudential policy – Reserve Bank of New Zealand

- [Portugal] Increasing number of foreigners snap up beachside homes in Portugal – Global Property Guide

- [Sweden] Sweden Responds to Worst Housing Slump Since 2008 With Supply – Bloomberg

- [United Arab Emirates] Dubai: Come Undone – REIDIN

- [United Kingdom] Housing Crisis: Big Speeches, Small Steps – New Economics Foundation

Photo by Aliis Sinisalu

On cross-country:

- Mortgages, developers and property prices – Bank for International Settlements

- FT Special Report on Property Market – Financial Times

- The US homeownership rate has lost ground compared with other developed countries – Urban Institute

On the US:

- It All Adds Up: The Cost of Housing Development Fees in Seven California Cities – Terner Center for Housing Innovation (UC Berkely)

- “Sand castles before the tide”: How can America’s most expensive cities keep themselves affordable?

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, March 13, 2018

A Look at Housing in Latin America

Global Housing Watch Newsletter: March 2018

Nora Libertun de Duren is a housing market expert at the Inter-American Development Bank. In this issue of the Global Housing Watch newsletter, de Duren looks at the developers’ rationale for building social housing in the urban periphery, the cost of living in the periphery and cost of densification, and other housing issues in Latin America.

On social housing in the urban periphery

Hites Ahir: You have a new paper on: Why there? Developers’ rationale for building social housing in the urban periphery in Latin America. What did you find? Any surprises?

Nora Libertun de Duren: This paper examines some of the mechanisms behind the location of privately developed affordable housing in peri-urban areas of Goiania, Brazil and Puebla, Mexico. It shows that developers choose peripheral locations based on three factors: the time required by the approval process, the cost of land and infrastructure, and the number of units they can accommodate on the site. The surprise was that economies of scale – and not cheap land prices– explain developers’ preference for building in peripheral areas. Large lots –which are available almost exclusively in urban peripheries – enable developers to achieve significant cost savings because these large lots allow developers to build more than 500 units.

Hites Ahir: Could you talk a bit more about what you find in terms of the costs of land, infrastructure, and services?

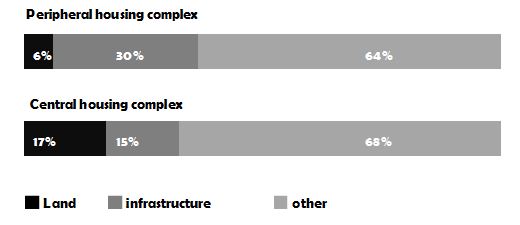

Nora Libertun de Duren: Developers establish a “land-plus-infrastructure” cost parameter that should not exceed a third of total housing costs. Within that parameter, the trade-off between land and infrastructure costs allows for many different project locations to meet the standard. For example, in the case of Goiania, land for central developments accounts on average for 17 percent of the investment, while infrastructure expenses average below 15 percent. Conversely, land in peripheral developments accounts on average for about 6 percent of the investment, while infrastructure expenses average some 30 percent. That is, the lower cost of peripheral locations is offset by the higher cost of the onsite infrastructure required.

Figure 1

Land and Infrastructure Costs as Percent Shares of Total Housing Costs

Source: Libertun de Duren, N. (2018). Why there? Developers’ rationale for building social housing in the urban periphery in Latin America. Cities, 72, 411-420.

Hites Ahir: In your paper, you note that developers are much more regulated in terms of construction quality than in terms of location of their products. Why this is the case?

Nora Libertun de Duren: This has to do with several dynamics. One is that programs that subsidize affordable housing construction are regulated by the national government, while land use plans are determined by municipal authorities. National programs have a legal limitation on how much they can change local land uses. Another one is that national housing programs have quantitative targets -numbers of units built- and disregard qualitative ones. Last, and in close connection to the former point, the policy has a strong bias towards promoting housing ownership at the expense of attending to housing location.

Hites Ahir: Typically, a household decides on the tradeoff between housing amenities and housing location. But you are saying that this trade-off decision between housing amenities and location has shifted from households to developers. What are the consequences of this?

Nora Libertun de Duren: Current housing subsides do not allow households to participate in the main urban real-estate market but stimulate developers to produce ad-hoc housing units at below market prices. Thus, shifting the trade-off decisions between amenities and location from households to developers. For low income households, this implies choosing between a housing unit built by the informal economy but well located or a housing built by the formal market in faraway locations. Besides the negative impact on households, this pattern of development has negative externalities in terms of urban productivity, congestion cost, and environmental pollution.

On the cost of living in the periphery and cost of densification

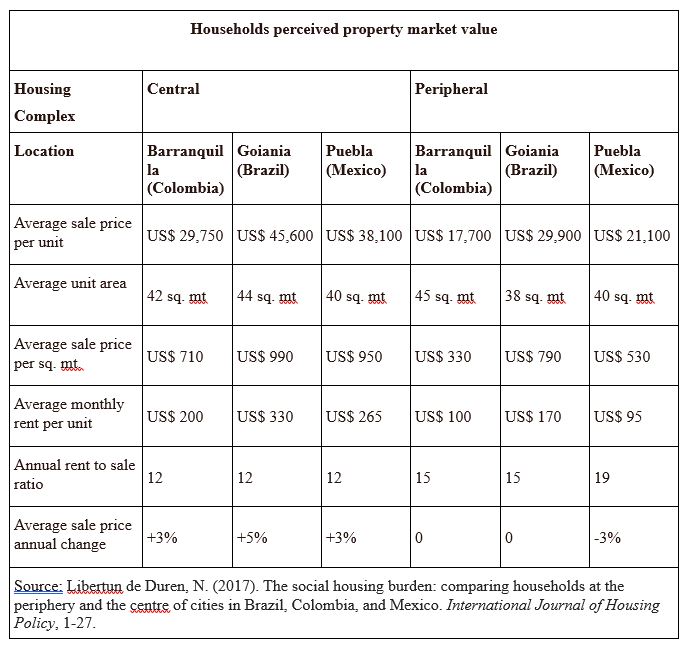

Hites Ahir: You have another paper on: The social housing burden: comparing households at the periphery and the centre of cities in Brazil, Colombia, and Mexico. How does the findings of this paper fit in with the previous one?

Nora Libertun de Duren: That paper analyzes how living in the periphery affects the livelihoods of low income households, through cases in mid-size cities in Brazil, Mexico and Colombia. The magnitude of the impact of housing location is staggering; households living in the periphery spend twice the money and three times the time in commuting than those who live in central locations. In addition, their property depreciates – market value of a peripheral housing unit is about 40 percent less than for a similar unit in the center; and their social capital declines as they stop seeing their relatives. These impacts are a serious policy concern since the programs that sponsor these housing projects are meant to improve the material conditions of low-income households, who are a captive market with very limited housing options.

Table 1

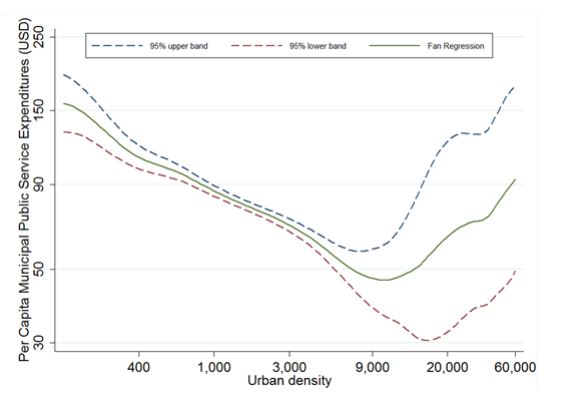

Hites Ahir: You have also written about the cost of densification (here and here). What do you find?

Nora Libertun de Duren: We find that municipal spending on public services -water, sanitation, electricity and trash collection- is strongly and non-linearly correlated to population density. The per capita expenditure on these services is lowest when population density is close to 9,000 residents per square kilometer. In our study of about 8,600 municipalities of Brazil, Chile, Ecuador and Mexico, 85 percent of all municipalities are below this ideal density level. This implies that, from the perspective of municipal expenditures, there is an argument for promoting density. Having said that, we should be aware that, similar density levels could be achieved through different configurations and that there may be many reasons -besides expenditures- that should be considered when planning a good city.

Figure 2

High quality municipal service coverage per capita on urban population density, by type of service (data from Brazil, Mexico, Ecuador and Chile)

Note: Non-parametric fan locally weighted regression, conditional on regional fixed effects and country specific time trends.

Source: Libertun de Duren, N., & Guerrero Compeán, R. (2016). Growing resources for growing cities: Density and the cost of municipal public services in Latin America. Urban Studies, 53(14), 3082-3107.

On Latin America

Hites Ahir: Can you tell us a bit about the condition of housing in Latin America?

Nora Libertun de Duren: In the last ten years, Latin America has improved in terms of the percentage of households with access to adequate housing. However, 55 million households -about 45 percent of the Latin American population- are in a housing-deficit situation. Of the households with deficits, 75 percent are subject to a qualitative deficit (overcrowding, lack of basic services, substandard building materials or lack of secure tenure), and the remainder is subject to a quantitative deficit (makeshift housing or two households under one roof). This situation is attributable to the shortcomings of the mortgage market, the high level of labor informality, and the relative high cost of housing units mostly due to the scarcity of urban lots with municipal services.

Hites Ahir: Slums tend to be closer to the city and amenities. Are there subsidies for upgrading the slums—making them a better place to live?

Nora Libertun de Duren: One of the main ways in which national government deal with slums is through neighborhood upgrading programs. These programs have been around for more than 30 years, one of the most famous ones is Favela-Bairro in Rio de Janeiro, Brazil. These programs fund the improvement of the physical environment by supporting household access to water, sanitation, electricity and by building and upgrading public infrastructure such as roads, sidewalks, and community facilities. Interventions may also include direct home improvements and support for land titling. Lately, such initiatives have tended to include activities for improving social interaction and local education. But these programs are remedial and cannot replace good planning, since their cost is three to seven times higher than the cost of formal urbanization. In addition, establishing an effective system of governance for the long-term maintenance of upgraded neighborhoods remains a challenge.

Hites Ahir: What about support for rental housing?

Nora Libertun de Duren: Programs supporting rental housing for low income households are scarce in the region. Experiences of the state as a landlord have not worked well, and private landlords are reluctant to participate in as much as they perceive legal procedures as slow and onerous. In addition, there is a culture that prizes homeownership, particularly in a context of high economic volatility. The good news is that recently, we are seeing some interesting developments when it comes to younger households. They strongly favor housing location over area and are open to new models of housing tenure.

Hites Ahir: Typically, how much funding is allocated to housing programs?

Nora Libertun de Duren: Latin American countries spend significantly in housing programs, national budgets allocation has typically ranged between 1 and 2 percent of their respective GDP. By comparison, the United States allocates about 0.55 percent of its GDP to support housing programs, and member countries of the OECD allocate an average of less than 1 percent of their GDP. Currently, expenditure on social housing programs in Mexico and Brazil amounts to about 1.7 percent of their respective GDPs. The contribution of these funds to increasing the housing supply is considerable. In Brazil, the flagship national program Minha-Casa-Minha-Vida, has been responsible for about 30 percent of the annual housing production in the formal sector. In Mexico, about 70 percent of the housing mortgages filed each year are linked to national programs for social housing.

Global Housing Watch Newsletter: March 2018

Nora Libertun de Duren is a housing market expert at the Inter-American Development Bank. In this issue of the Global Housing Watch newsletter, de Duren looks at the developers’ rationale for building social housing in the urban periphery, the cost of living in the periphery and cost of densification, and other housing issues in Latin America.

On social housing in the urban periphery

Hites Ahir: You have a new paper on: Why there?

Posted by at 5:00 PM

Labels: Global Housing Watch

Rethinking and Expanding Research on Housing Policy with a Global Perspective

Global Housing Watch Newsletter: March 2018

Paavo Monkkonen is Associate Professor of Urban Planning at the UCLA Luskin School of Public Affairs. In this issue of the Global Housing Watch newsletter, Monkkonen talks about housing policy in Indonesia, Mexico, United States, and across countries.

On housing policy in general

Hites Ahir: Is it correct to say that most of the studies on housing policy have focused mostly on ways to subsidize housing or to design financing schemes? Why?

Paavo Monkkonen: It is hard to characterize an entire field, but several dimensions of housing policy that need more attention. Matthew Desmond’s book on eviction clearly demonstrated the importance of the topic in an eye-opening manner, and he makes a similar point about housing vouchers having received a disproportionate amount of scholarly attention. Similarly, Richard Rothstein’s recent book The Color of Law reveals not only the malicious intent of many kinds of land use regulations – especially single-family zoning – but also their lack of justification in the present day. We need more research in several areas, for example, the role of regulations and supply in ‘neighborhood’ housing markets. Also, the way in which policies affect the housing filter, which is essentially the rate at which older housing becomes more affordable and depends to a significant extent on regional housing supply elasticity. Another area is the behavior of property owners, for example, how do corporate vs. ‘mom and pop’ landlords treat tenants. Finally, the role of impact fees – for local community benefits – in the rate of new housing construction merits more study. This is especially important in the United States, where governments are increasingly saddling new development with obligations such as community benefits and contributions to funds for affordable housing.

A big reason is that many of these issues are hard to study. Measuring and modeling the impacts of land use regulations is very challenging, for example, because of problems with endogeneity, the fragmented and inconsistent nature of land use rules in US cities, and inconsistent enforcement across regulatory bodies. Not to mention, high quality data on local regulations and rents are notoriously hard to come by.

Hites Ahir: You have written an introduction to an upcoming Special Issue of the International Journal of Housing Policy (IJHP). In the introduction, you argue that housing policy studies should focus more urban land and planning policies, legal systems, and social movements. Why this is important?

Paavo Monkkonen: In the last two decades, economists have convincingly demonstrated the role of land use rules in metropolitan housing markets. Yet there are many unanswered questions – and consequential political debates – about land use rules in housing supply and rents at the neighborhood level. We also understand that legal treatment of renters and property rights – including enforcement – are crucial for most people’s housing stability. Most international organizations want to support and promote rental markets as a viable option for many people, but how to do it effectively is not yet established. Finally, housing politics is so important because the most well-designed subsidy scheme will be completely ineffective without funding, and funding for housing subsidies depends on political support.

On housing policy in developing economies

Hites Ahir: Land Use Regulations and Urbanization in the Developing World: Evidence from Over 600 cities—is a paper that you have co-authored. In this paper, you find that regulations are more cumbersome in poorer countries. Why do developing economies continue with strict regulations even though they are associated with higher levels of bribery?

Paavo Monkkonen: Well I think that question partly answers itself. Many public officials are able to exploit strict rules to their own benefit. In many cases, inertia plays an important role as well. Colonial governments often set up land use regulations for their sections of the city – large minimum lot sizes, for example – and ignored the rest. Many countries have kept these rules in spite of very low levels of compliance. Changing them would be politically challenging and probably unpopular among civil servants.

Hites Ahir: You have also co-authored a book chapter on Comparative evidence on urban land-use regulation bureaucracy in developing countries. It finds that in most cases, following the law when developing land for urban use is more cumbersome and expensive in Asia than in Latin America. What explains this difference?

Paavo Monkkonen: My answer to this question would be speculative. Moreover, it is a challenge to characterize these large regions where historical patterns of urbanization and governance are so diverse. The hypothesis in Albert Saiz’s important work on land use regulations in the United States is that places with less available land are expected to regulate it more intensely. Given that population densities have traditionally been higher in much of Asia than Latin America, this might be a contributing factor.

Hites Ahir: What are the policy implications from these two papers?

Paavo Monkkonen: One is that higher levels of government – provincial or federal – ought to pay more attention to local rules and their enforcement. One almost universal hindrance to housing affordability (and the environmental sustainability of cities) is low-density zoning. These rules are frequently municipal and I think state (or federal) governments should be more aggressive in curtailing the powers of municipalities over land use in strategic ways to limit exclusion.

On housing policy in specific countries: Indonesia, Mexico, and the US

Hites Ahir: On Indonesia, you have a paper on Housing deficits as a frame for housing policy: demographic change, economic crisis and household formation in Indonesia. The paper shows the challenges of using the concept of housing deficit for policy-making. Could you talk a bit about this?

Paavo Monkkonen: I am often asked how many housing units a city would need to add to achieve affordability. This is a frustrating question, as household formation, migration, and housing production are such dynamic concepts. Instead, we should ask how responsive housing production is in a region to the demand for housing there. It is interesting for me to reflect on this paper about Indonesia, in which I challenge the use of the shortage discourse to support supply-oriented policies there, as currently, California actually does have a housing shortage. The difference in the two places is found in indicators like affordability, migration rates, and household formation.

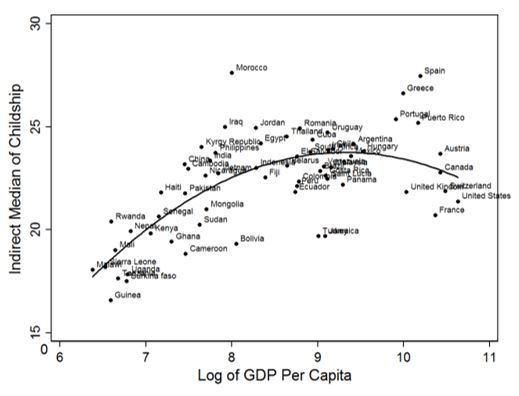

A global perspective is also important in framing this question of adequate numbers of housing units. In a comparative study of household formation in almost 70 countries, I found an interesting quadratic relationship between levels of economic development and the age at which people leave home and form a household. Figure 1 shows one of these relationships using the idea of ‘childship’, or the age at which people cease to be a child in the census accounts of household structure.

Figure 1. Indirect Median of Childship and GDP per capita (most recent census)

Source: Author with data from censuses obtained through IPUMS International, available at: https://international.ipums.org/international/

Hites Ahir: On Mexico, you have recently written a paper on The Role of Housing Finance in Mexico’s Vacancy Crisis. A surprising finding of the paper is that cities with higher levels of mortgage lending have higher levels of vacancy in the city center but not the urban periphery. What explains this?

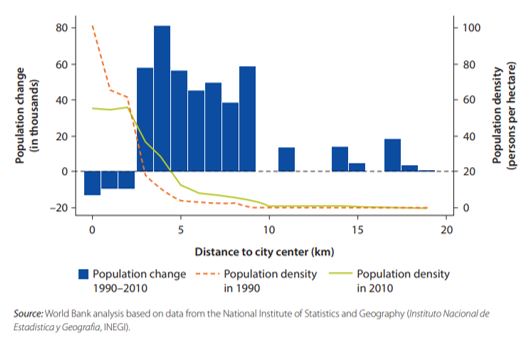

Paavo Monkkonen: There are a several reasons. INFONAVIT financing has until recently been directed at new housing in the urban periphery, simply because it was only available for new houses, which were primarily built on greenfield sites. This has led to fewer households rehabbing and inhabiting older, centrally located housing. Of course, there are other reasons leading centrally located housing stock to be vacant, such as the costs of redevelopment, limited infrastructure, negative externalities such as noise and congestion in the city center, and complications with legal title to land and property. In fact, the trend of central city population loss in Mexico is widespread. Of the 91 largest cities in Mexico, 67 lost population in their central two kilometers between 2000 and 2010. Figure 2 below, from the World Bank’s Urbanization Review, shows one city’s recent changes in population density at different distances from the city center. My analysis suggests that the financing system has exacerbated this trend.

Figure 2. Shifting Population Densities in Queretaro, 1990-2010

Hites Ahir: How can policymakers address this issue?

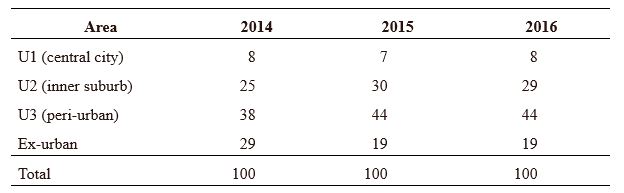

Paavo Monkkonen: Various federal agencies in Mexico are trying to address this problem. The main federal housing finance agency INFONAVIT is trying to direct more financing to ‘used’ housing and housing improvement, rather than new housing. The main federal housing subsidy provider, CONAVI, is directing housing subsidies to more centrally located housing through a system of urban containment perimeters. My critique of that system (here) is that it was limited to CONAVI subsidies not INFONAVIT loans. Table 1 shows where housing loans are going in Mexico, and how this approach has not worked to fund centrally located housing.

Table 1. Share of Housing Loans in Urban Containment Perimeters, 2014-2016

Source: Sistema Nacional de Información e Indicadores de Vivienda; SNIIV, 2016.

INFONAVIT could modify their lending according to these same urban containment perimeters. All levels of government could direct funding to urban upgrading in central cities to improve infrastructure. The corruption in the Mexican housing system that has been carefully documented by the LA Times, must also be addressed.

Hites Ahir: Finally, you have also been working on California’s housing market (here, here, and here). As you know, currently, there is a lot talk about affordability issues. Could you share with us your view on the causes, and how does your view fit with the narrative that is been reported?

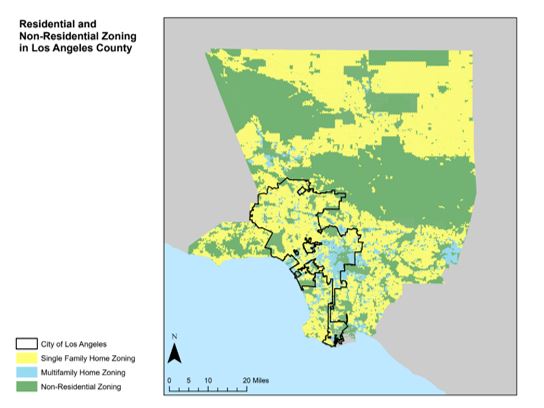

Paavo Monkkonen: California’s metropolitan regions have strong economies and growing numbers of high-wage jobs. This attracts people and capital. At the same time, the state and its many local governments have created myriad rules that dramatically limit new housing supply – especially in neighborhoods where people most want to live. One of the most consequential of these rules is single-family zoning. Roughly three quarters of residential land in the City and County of Los Angeles is zoned for single-family houses only (see Figure 3). Single-family houses are roughly 20% more expensive than houses in multi-family buildings. Therefore, local governments could remove their prohibition on the construction of the less expensive kind of housing across the urban area to greatly improve affordability.

Figure 3. Zoning in Los Angeles County

Source: Author with data from Southern California Association of Governments.

Hites Ahir: What has been the policy response?

Paavo Monkkonen: California’s state government has finally begun taking action to address the housing crisis. They passed several laws last year, including SB 2 and 3, which generate more funds for subsidized housing and SB35, which begins to restrict the ability of local governments to block some kinds of new housing. These are laudable efforts but at a small scale considering the housing crisis facing the state. This year, a radical proposal by Senators Weiner and Hueso, SB 827, would override local zoning near transit and allow mid-rise housing. Currently, many cities have single-family zoning next to metro stations and high-frequency bus routes. I think this proposal is at the level of change the state needs, and also addresses environmental goals. Similarly, aggressive proposals to subsidize housing for low-income households at the state and local level – such as through a broad based tax on land – will be important complements. Removing barriers to new construction is a necessary but insufficient approach to ensuring that all households have decent, stable housing.

Global Housing Watch Newsletter: March 2018

Paavo Monkkonen is Associate Professor of Urban Planning at the UCLA Luskin School of Public Affairs. In this issue of the Global Housing Watch newsletter, Monkkonen talks about housing policy in Indonesia, Mexico, United States, and across countries.

On housing policy in general

Hites Ahir: Is it correct to say that most of the studies on housing policy have focused mostly on ways to subsidize housing or to design financing schemes?

Posted by at 5:00 PM

Labels: Global Housing Watch

Thursday, March 8, 2018

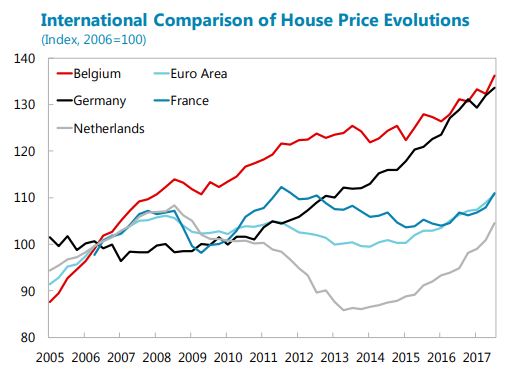

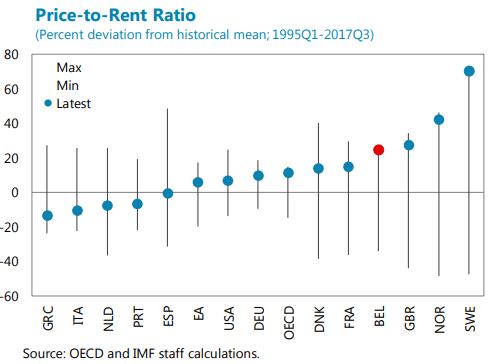

Housing Market in Belgium

The latest IMF report on Belgium says that:

“The housing market appears to be only moderately overvalued, but pockets of vulnerability exist. Having grown rapidly in the 2000s, residential housing prices did not experience a sharp decline during the crisis, and have since risen by about 20 percent in nominal terms. The price-to-rent and price-to-income ratios stand well above their historical averages. More sophisticated measures, however, indicate only a moderate overvaluation. Since 2015 there has been a reversal in the tightening of mortgage lending standards, as evidenced by a growing share of loans with high loan-to-value (LTV) and/or high debt service-to-income (DSI) ratios. Risks are mitigated to some extent by the fact that Belgian households generally hold considerable financial assets. Nevertheless, nearly a third of outstanding mortgage debt is held by households whose liquid financial assets cover less than six months of debt service.

It will be important to stand ready to tighten macroprudential conditions further if balance sheet risks were to grow significantly. To address growing risks in the housing market, the NBB in 2014 introduced a 5 percent risk weight add-on for banks using internal ratings models to determine their minimum regulatory capital requirements for mortgage loans. In 2017, the NBB proposed a tightening of macroprudential policies through a targeted increase in capital charges linked to the riskiness of exposures, proxied by LTV ratios. However, as this proposal was not accepted by the government, the NBB subsequently proposed a new macroprudential measure requiring banks with riskier mortgage portfolios to hold more capital. This measure should be enacted promptly. Looking ahead, it will be important to strengthen the NBB’s ability to deploy cyclical macroprudential measures in the financial sector in a timely manner.”

The latest IMF report on Belgium says that:

“The housing market appears to be only moderately overvalued, but pockets of vulnerability exist. Having grown rapidly in the 2000s, residential housing prices did not experience a sharp decline during the crisis, and have since risen by about 20 percent in nominal terms. The price-to-rent and price-to-income ratios stand well above their historical averages. More sophisticated measures, however, indicate only a moderate overvaluation.

Posted by at 4:26 PM

Labels: Global Housing Watch

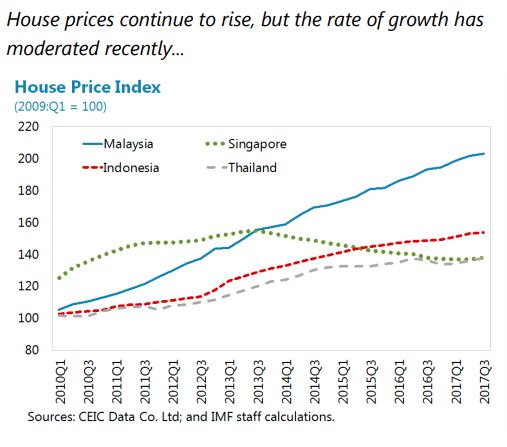

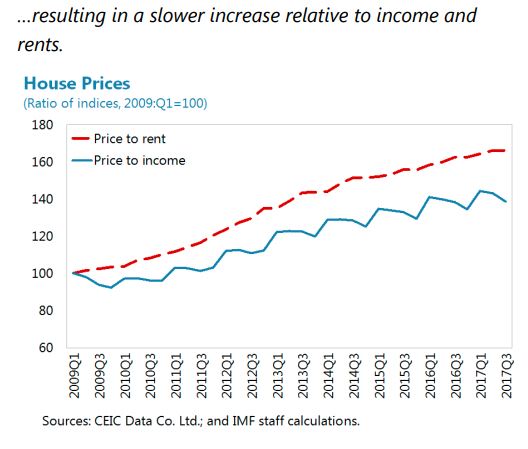

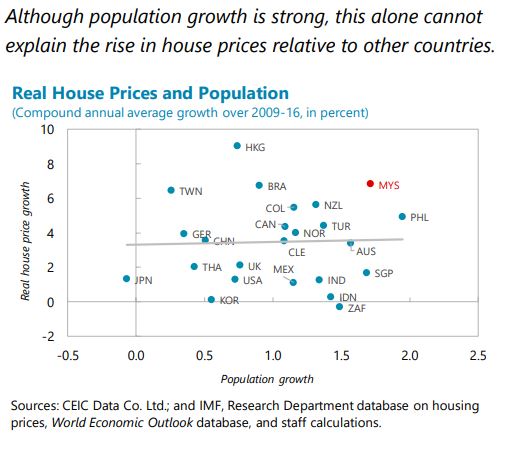

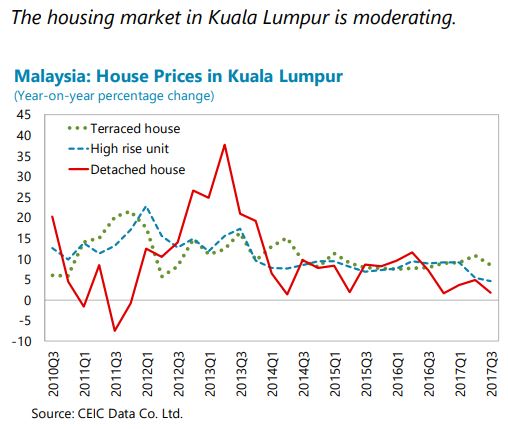

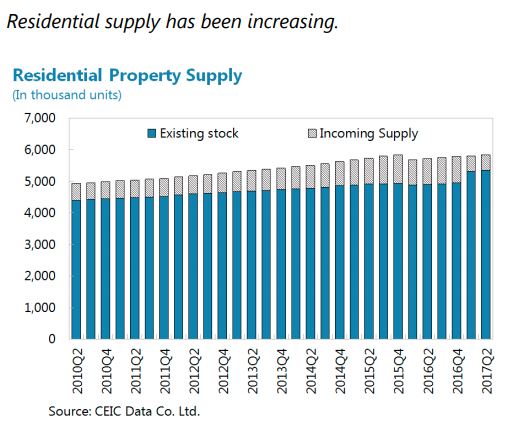

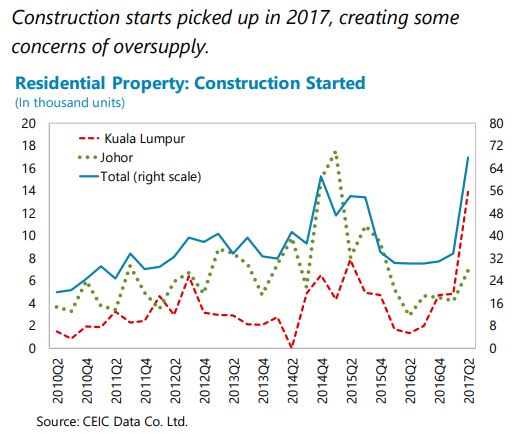

Housing Market in Malaysia

The IMF’s latest report on Malaysia says that:

“Measures could be considered to mitigate risks to financial stability. For the housing (…) market, possible measures could include risk weights and lending limits targeting the construction sector, and measures encouraging developers to lease the housing stock that remains unsold for an extended period. To encourage the rental market, the authorities could look into reforming the regulations pertaining to rents and tenant-landlord relationships or granting developers tax exemptions for rental income on leasing units, within the context of the approved government budget envelope. On mortgage lending, sector-wide LTVs (on the second and first properties) and debt service to income limits could supplement the ones that are presently selfimposed by the banks, complementing the existing limit for borrowers with income under 3,000 ringgits per month. Strong economic conditions offer a good window of opportunity for the above policy adjustments.”

The IMF’s latest report on Malaysia says that:

“Measures could be considered to mitigate risks to financial stability. For the housing (…) market, possible measures could include risk weights and lending limits targeting the construction sector, and measures encouraging developers to lease the housing stock that remains unsold for an extended period. To encourage the rental market, the authorities could look into reforming the regulations pertaining to rents and tenant-landlord relationships or granting developers tax exemptions for rental income on leasing units,

Posted by at 4:20 PM

Labels: Global Housing Watch

Subscribe to: Posts