Showing posts with label Global Housing Watch. Show all posts

Monday, May 28, 2018

A Look at Housing Affordability: From a Design Perspective

Global Housing Watch Newsletter: May 2018

This post is written by Laura Wainer. She is a doctoral student at the MIT’s Department of Urban Studies and Planning, and Housing+ conference curator.

The provision of housing is a global challenge with an urgent need for innovation. Design is typically not an approach that comes to mind when one refers to housing affordability, whether at the scale of the house, neighborhood, or city. In its third biennial theme, “Housing+“, the MIT Norman B. Leventhal Center for Advanced Urbanism (LCAU) at the Massachusetts Institute of Technology explored this global phenomenon through the lens of interdisciplinary and multi-scalar approaches.

The structure of the biennial leaded by Adèle Naudé Santos was inspired in a “learning by doing” process. In association with local and national governments, philanthropic institutions, and international agencies, the LCAU hosted seven workshops where faculty and graduate students of Architecture and Urban Planning focused on different challenges of affordable housing provision in Africa, Asia and Latin America. The biennale culminated in an international exhibition and conference hosted on May 3 to 4 at the Media Lab, MIT.

The Housing+ conference included 33 practitioners and academics from all over the globe, who explored the interpretations of the “+,” extending the design dialogue beyond the scale of the housing unit. Panels investigated the ways in which housing design interacts with aspects of community building, large scale planning, public space, construction industry and infrastructure. The following summary presents the key topics of the two-day discussion.

Revisiting the housing challenge…

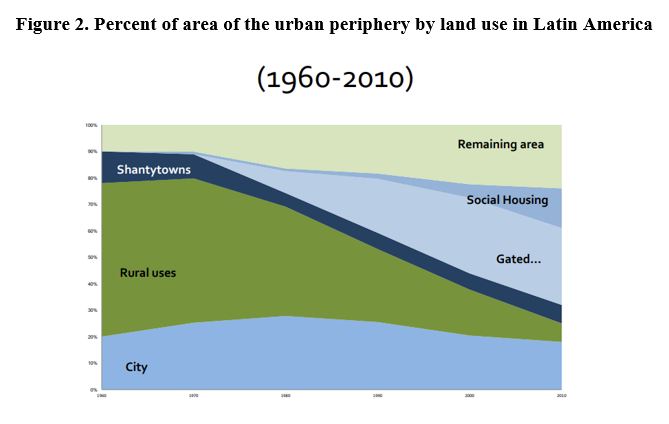

Most of the participants of the conference emphasized on the transformed nature of the current housing deficit. They argued that today, the most significant housing deficit, in both emerging economies and developed countries such as the U.S., is qualitative rather than quantitative. For the last twenty years, national governments have delivered subsidized houses for the lowest income populations at massive scale. Contrary to performing poorly, governments in Africa, Asia and Latin America had proved great efficiency in this housing delivery scheme. For instance, summing up the figures of the countries of the MIT workshops (Brazil, Colombia, Guayana, India, Peru, Rwanda), the national governments delivered about 4,609,600 housing solutions for the lowest income populations.[1]

However, this sudden, extraordinarily simultaneous expansion of low-income national housing subsidy programs, targeted to both the demand and supply, shows that despite the different political, institutional, demographic and economic contexts, their housing policies produce the same industrial-like neighborhoods located on the outskirts of cities. We also see a homogenization of house design and construction technologies that look similarly inadequate. Empirical research in Mexico, South Africa and Colombia demonstrates that families often abandon these houses looking for proximity to jobs, education centers and health care institutions.

Nora Libertun, a housing market expert at the Inter-American Development Bank, presented her research about the housing developers’ decision making for building in peripheral areas in Latin America. She said that one of the biggest challenges for housing policy is how to shift from a rationale of ‘economies of scale’ production to an environment where building affordable housing in inner cities is an attractive investment opportunity. Diane Jones, Program Director for Landscape Architecture at the University of Texas, studies the relationship between housing and infrastructure access in the U.S., specifically the phenomenon of “transit desserts.” Jones argues that this scenario is not as different in the U.S., and that the qualitative housing deficit is “a hidden problem” in suburban areas of the country.

These industrial-like housing landscapes are re-shaping the urban form of cities and have ecological implications at a broader territorial scale. Kazi Ashraf, Director of the Bengal Institute, argued that the unprecedented scale of development in Bangladesh is transforming the natural landscapes of the country with significant impacts on food production and climate change.

Source: Presentation by Nora Libertun

Scaling-up innovation and the limits of standardization…

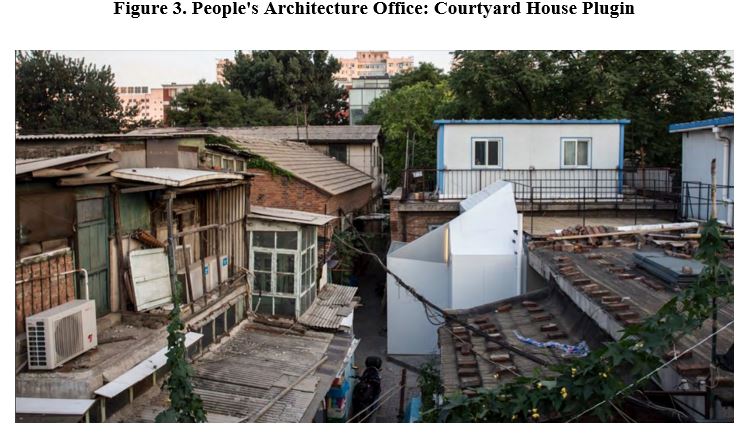

A great deal of the H+ conference consisted of sharing international and U.S cases that successfully interconnected design, financial and social innovation. Practitioners discussed about the challenge of scaling-up micro practices to systemic housing solutions. Andy Bolnick, Director of Ikhayalami, presented the “re-blocking system,” an in site upgrading, participative design intervention that couples innovative shelter and infrastructural solutions with the spatial reconfiguration of informal settlement layouts. She claimed that scaling-up is not just matter of quantitative replication but also how innovations are adopted by the public sector. While Slum Dwellers International was capable of spreading the re-blocking system among the grassroots federation, the city of Cape Town presented several difficulties to incorporate re-blocking in their informal settlements upgrading policy. James Shen, founding director of Beijing-based People’s Architecture Office, presented the Courtyard House Plugin, a prefab system that efficiently upgrades and expands homes without demolition or relocating inhabitants. He explained that their approach is to think of scaling-up in terms of customization –instead of standardization– by creating flexible solutions that focus on systems rather than an architectural output.

Source: Presentation by James Shen

Associate professor in the MIT Department of Architecture Larry Sass told the audience that to build prototypes is easy but to scale them up to systemic housing solutions represents one of the most difficult challenges in the construction industry. He and Anupama Kundoo highlighted the importance of “contextual technologies.” Reducing costs often relates to standardization, mass production, industrialization, but in a post-industrial era reducing costs must pair to be flexible enough to adapt innovation into different contexts and expressions. From the same perspective, Nathalie de Vries director and co-founder of MVRDV, and Christoph Heinemann from the Institute for Applied Urbanism in Berlin, showed examples of “suited standards,” a combination between participatory processes and the architect’s ability to transform users’ decision making into standardized design solutions. Successful but not mainstream, these approaches should be a core agenda of the design education in the future. Andrew Freear, Professor at Auburn University Rural Studio, and his team consider participatory design as a quintessential part of low-cost housing innovation in Alabama.

Scaling up innovation and successful micro experiences is not simple. The intrinsic relationship between innovation and informality stresses two main challenges. On the one hand, how can the public and private sectors incorporate innovative solutions that many times come from pushing the boundaries of legality within policy schemes and market strategies. On the other hand, low income users are often the ones who must deal with innovation’s burden. Local governments’ lack of capacity to coordinate successful cases into a territorial strategy may represent a liability at the aggregate scale. As Sheela Patel, founder and Director of the Society for Promotion of Area Resource Centres in India, claimed: “poor people do not want to live in islands that are pilot renders of founders, philanthropic institutions, and creative architects, where each project is isolated, is different and has its own autonomous logic.”

Housing policy or housing politics?

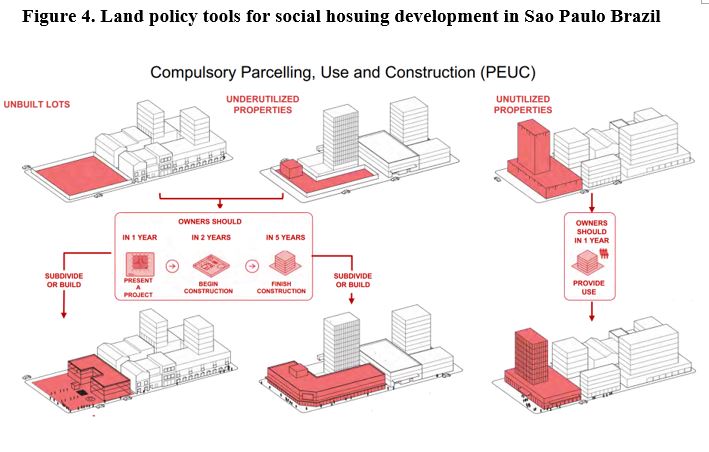

Unfortunately, rarely public expenditures are structured in a way that will improve housing affordability and result in more inclusive cities. Indeed, in many places the programs could have long-term detrimental effects. Moreover, as the experience of many countries presented in this conference indicates, once an approach has taken root it is very difficult to change. Nora Libertun and Fernando De Mello Franco, former Secretary of Urban Development of the Municipality of São Paulo, said that the greatest challenges for housing policy is how to promote the private sector to build in the inner city and how permeate tacit political agreements between large scale developers and governments. De Mello Franco argued that the politics of land access has transformed good policies in bad results, like the infamous “Minha Casa Minha Vida.”

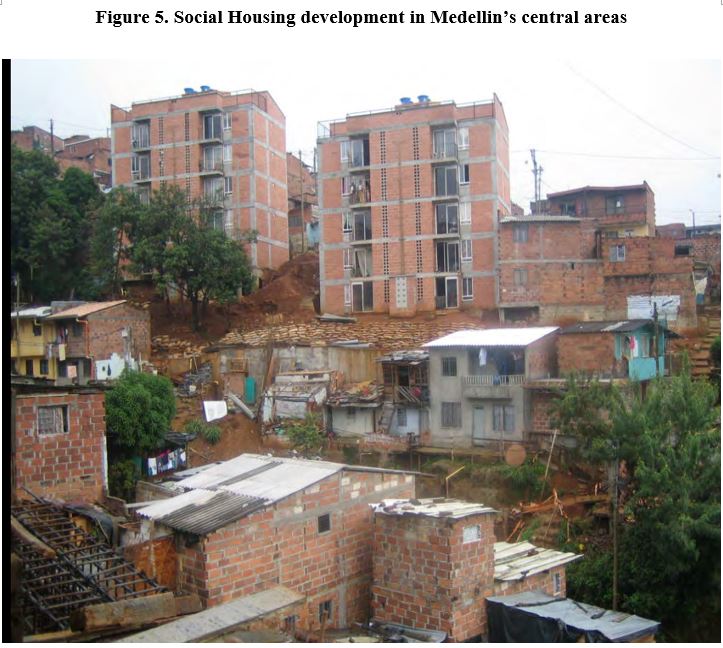

Alejandro Echeverri, director of URBAM, presented his insights about Medellin’s successful redevelopment, which included the construction of thousands of well-located, affordable housing units in the city. For Echeverri, Medellin’s success relied on a “political momentum,” that the city is not experiencing today. He asked, how can non-governmental actors interested in social justice create governance conditions for reducing inequality in our cities? Echeverri, Libertun, De Mello and housing expert Robert Buckley also questioned whether the housing agenda is a matter of social justice or political agreements with large scale developers and the construction industry. In this line, housing expert professor Lawrence Vale asked: what affordable housing should afford? And Steve Weir, from Habitat for Humanity claimed that integrated solutions for systemic change should include multi-scalar and multi-sectorial approaches that include public, private, civil society, and also households.

Source: Presentation by Alejandro Echeverri

Better data, not just more data…

Focusing on qualitative aspects of housing implies revisiting how we measure housing deficit and monitor the impacts of interventions in the short and long term. The new UN Sustainable Development Goals and Habitat 3 called for increased attention to improve measures of urban issues and housing. However, many speakers at the H+ conference highlighted that more data is not necessarily better data. Like the attempt to construct new cities without addressing the fundamental problems besetting the existing ones, attempts to create new urban indicators fail to appreciate just how weak existing data is. Without better data, accountability for public expenditures cannot be achieved. Diane Jones showed how aggregate transport data is built on racial biases in the U.S., MIT professor James Wescoat asked how we can develop metrics to measure and evaluate quality of life, Anupama Kundoo spoke about the challenges of measuring design impacts in both affordability and quality of life.

The limits of data and how we monitor the impacts of housing policy also speaks to a timing question: When is the appropriate time to measure the outcomes of a housing intervention? Philip Yang, founder of URBEM, showed award-winning affordable housing projects in Brazil that ended up in decayed, failed experiences for the families in the long term. Thus, better data implies to think of which metrics can be more sensible to context, geographies and culture; and at the same time, which metrics we should standardize to understand the scope of the housing challenge at a global scale in a market that responds to both local and international dynamics.

[1] Data Source: Cámara de la Construcción Colombiana, Indicadores de Vivienda y Construcción (2017); Congressional Budget Office. Federal Housing Assistance for Low-Income Households (2015); Gopalan, K., & Venkataraman, M. (2015). Affordable housing: Policy and practice in India; Instituto Nacional de Estadística e Informática de Perú, Encuesta Nacional de Programas Presupuestales (2016); Joint Center for Housing Studies, The State of the Nation’s Housing (2017); Ministry of Statistics and Programme Implementation, India. HOUSING – Statistical Year Book India 2016; Ministerio de Vivienda, Construcción y Saneamiento de Peru. Plan Nacional de Vivienda 2006 – 2015 “Vivienda Para Todos.”; Rwandan Housing Authority. Projects (2017)

Global Housing Watch Newsletter: May 2018

This post is written by Laura Wainer. She is a doctoral student at the MIT’s Department of Urban Studies and Planning, and Housing+ conference curator.

The provision of housing is a global challenge with an urgent need for innovation. Design is typically not an approach that comes to mind when one refers to housing affordability,

Posted by at 6:00 PM

Labels: Global Housing Watch

Friday, May 25, 2018

Housing View – May 25, 2018

On cross-country:

- New York property jitters herald declines elsewhere – Financial Times

- Real Estate Summary – UBS

On the US:

- Housing Constraints and Spatial Misallocation – Centre for Economic Policy Research

- Young left out of US boom in housing wealth – Financial Times

- An uneven housing recovery – Financial Times

- How I Caused California’s Housing Crisis: Efforts in the 1980s to curb the state’s explosive growth are having unintended consequences three decades later. – Bloomberg

- California Turns to Homeowners to Help Solve a Crisis – Bloomberg

- How to Rescue Neighborhoods That Are Down and Out – Bloomberg

- A Housing Boom, Then a Volcanic Eruption – Wall Street Journal

- Your Guide to the Fair Housing Act – Trulia

- A Healthcare Giant Enters the Battle for Cheaper Housing – Citylab

- Concrete measures: the rise of public housing and changes in young single motherhood in the U.S. – Journal of Population Economics

- Amazon has been a generous neighbor to a Seattle homeless shelter. Why is its generosity such a pain? – Slate

- How Do We Proactively Preserve Unsubsidized Affordable Housing? – Harvard Joint Center for Housing Studies

- New York Today: Fixes for a Broken Housing System – New York Times

On other countries:

- [China] China housing ministry to step up checks on local government efforts to tame prices – Reuters

- [Finland] Wide regional disparities in Finnish house prices and household indebtedness – Bank of Finland

- [Finland] The Finnish real estate investment market – Bank of Finland

- [India] Indian homebuyers now have a new weapon to fight errant real estate developers – Quartz

- [New Zealand] Left behind: why boomtown New Zealand has a homelessness crisis – Reuters

- [South Korea] UN housing expert calls for human rights shift in South Korea – United Nations

- [Spain] The Risk of Job Loss, Household Formation and Housing Demand: Evidence from Differences in Severance Payments – Banco de España

- [Spain] Real Estate Situation Spain. May 2018 – BBVA Research

- [Spain] La fuerte subida de precios resucita la creencia de que “alquilar es tirar el dinero” – El Pais

- [United Kingdom] Rent and its Discontents: A Century of Housing Struggle – University of Glasgow

- [United Kingdom] London Home Price Declines Seen Continuing for Next Three Years – Bloomberg

- [United Kingdom] London’s Long Housing Boom Is Over. Is a Bust Coming? – Bloomberg

- [United Kingdom] Why are London house prices falling? – Office for National Statistics

Photo by Aliis Sinisalu

On cross-country:

- New York property jitters herald declines elsewhere – Financial Times

- Real Estate Summary – UBS

On the US:

- Housing Constraints and Spatial Misallocation – Centre for Economic Policy Research

- Young left out of US boom in housing wealth – Financial Times

- An uneven housing recovery – Financial Times

- How I Caused California’s Housing Crisis: Efforts in the 1980s to curb the state’s explosive growth are having unintended consequences three decades later.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, May 24, 2018

Housing Market in Estonia

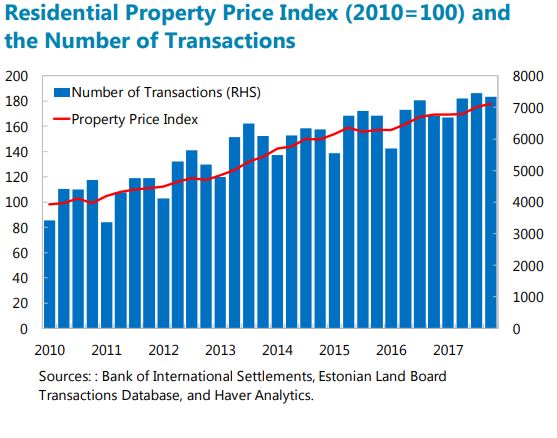

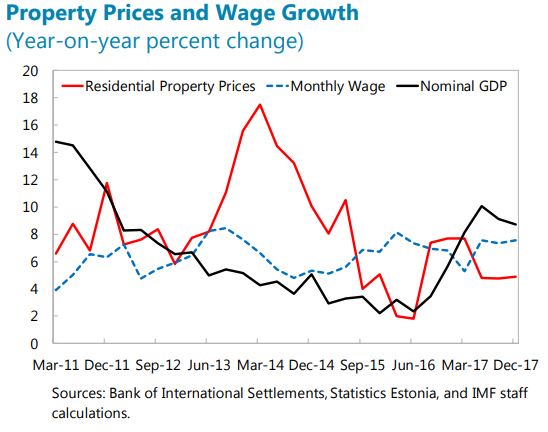

The IMF’s latest report on Estonia says:

“Residential real estate market activity has increased, but prices remain well anchored to income and nominal GDP growth (figures below). The number of transactions in 2017 rose by

8 percent compared to the level in 2016 and the real estate price index increased by 5 percent, driven partly by the growing share of new apartments. Going forward, the number of permit applications suggest construction activity should be sufficient to just maintain the current housing stock.”

The report also says that: “Housing market trends, both domestic and abroad, are important drivers of banking sector developments in Estonia. While household indebtedness is moderate, banks’ extension of housing loans accelerated in 2017. Higher interest rates following an eventual monetary policy normalization could pose a risk for household finances and potentially affect future financial developments and economic growth. In addition, developments in cross-border banking linkages indicate that potential spillovers from vulnerabilities in Nordic parent banks, notably the Swedish real estate sector, require further safeguards for financial stability, notably in cross-border banking supervision through the Nordic-Baltic cooperation platform.”

The IMF’s latest report on Estonia says:

“Residential real estate market activity has increased, but prices remain well anchored to income and nominal GDP growth (figures below). The number of transactions in 2017 rose by

8 percent compared to the level in 2016 and the real estate price index increased by 5 percent, driven partly by the growing share of new apartments. Going forward, the number of permit applications suggest construction activity should be sufficient to just maintain the current housing stock.”

Posted by at 5:31 PM

Labels: Global Housing Watch

Friday, May 18, 2018

Housing View – May 18, 2018

On cross-country:

- The Efficiency of Savings-linked Relationship Lending for Housing Finance – Journal of Housing Economics

- Do House Prices Sink or Ride the Wave of Immigration? – IZA Institute of Labor Economics

- Cultural similarities and housing market linkage: evidence from OECD countries – Springer

- ¿Es Airbnb realmente culpable de la subida de precios en los alquileres? – GQ

- ¿Cuáles son y en qué países están los barrios más caros de América Latina? – BBC

On the US:

- Homeownership and Housing Wealth (Presentation, Remarks, Blog ) – Federal Reserve Bank of New York

- The Links Between Affordable Housing and Economic Mobility – Terner Center

- Faced with a housing crisis, California could further restrict supply – Economist

- Boston Wants People To Build Tiny Houses In Their Yards – Citylab

- What the Future of Affordable Housing Already Looks Like – Citylab

- Why universities became big-time real estate developers – Slate

- Rent-Control Initiative Could Obliterate California’s Housing Markets – Reason

- Rising Home Prices Lead To Worries Of Another Housing Market Bubble – NPR

- Housing: High Prices, Few New Units – Mises Institute

- Ben Carson vs. the Fair Housing Act – New York Times

- Wall Street Is Pouring Money Into House Flipping – Slate

- Why Don’t People Who Can’t Afford Housing Just Move Where It’s Cheaper? – New York Times

- California Today: In San Francisco’s Housing Lottery, It’s the Luck of the Draw – New York Times

- Housing Tax Credit Qualified Action Plans Affect the Location of Affordable Housing – National Low Income Housing Coalition

- Rising Rates Vs. The Housing Market – NPR

- The Seattle Area Is Solving One of Housing’s Biggest Challenges – Slate

- How Will the Gig Economy Shape Mortgage Lending? – Fannie Mae

- The Impact of the Tax Cuts and Jobs Act on Local Home Values – Federal Reserve Bank of Cleveland

- The American Housing Crisis Might Be Our Next Big Political Issue – Citylab

On other countries:

- [Australia] Stricter lending restrictions threaten housing markets in Australia – Global Property Guide

- [Australia] Inquiry into social impact investment for housing and homelessness outcomes – Australian Housing and Urban Research Institute

- [Canada] Through the Roof: The High Cost of Barriers to Building New Housing in Canadian Municipalities – C.D. Howe Institute

- [Canada] The World’s Hottest Luxury-Property Market Is a Sleepy Canadian City – Bloomberg

- [Chile] Estudio demuestra que más de la mitad de los santiaguinos no puede comprar una vivienda – CNN

- [China] China’s property market to steadily cool in 2018 – government think tank – Reuters

- [Hong Kong] Could a Colonial-Era Golf Club Solve Hong Kong’s Housing Woes? – New York Times

- [India] Housing demand in Indian metros: a hedonic approach – Emerald

- [Ireland] Cost Rental Housing – A Model for Ireland? – NERI

- [Spain] Spain is cracking down on Airbnb, just in time for the tourist season – Quartz

- [United Kingdom] Britain’s housing supply is perking up at last – Economist

- [United Kingdom] How to make the case for community-led housing on public land – New Economics Foundation

Photo by Aliis Sinisalu

On cross-country:

- The Efficiency of Savings-linked Relationship Lending for Housing Finance – Journal of Housing Economics

- Do House Prices Sink or Ride the Wave of Immigration? – IZA Institute of Labor Economics

- Cultural similarities and housing market linkage: evidence from OECD countries – Springer

- ¿Es Airbnb realmente culpable de la subida de precios en los alquileres? – GQ

- ¿Cuáles son y en qué países están los barrios más caros de América Latina?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, May 11, 2018

Housing View – May 11, 2018

On cross-country:

- Housing and the Business Cycle Revisited – University of Augsburg

- Prime Global Cities Index – Q1 2018 – Knight Frank

- How 3D printing is revolutionizing the housing industry – TechCrunch

On the US:

- Fueling a Frenzy: Private Label Securitization and the Housing Cycle of 2000 to 2010 – NBER

- The Great Housing Reset – Citylab

- Rising incomes, rising rents, and greater homelessness – McKinsey

- This is the Wrong Time to Cut Back on Public Housing – Institute for Policy Studies

- Tax Luxury Housing to Fund Social Housing – Inequality.org

- Black and White Homeownership Rate Gap Has Widened Since 1900 – Zillow

- 50 Years After the Fair Housing Act – Inequality Lingers – Trulia

- Government Remains the Biggest Obstacle to Fair Housing – The American Prospect

- Housing Confidence Hits New All-Time High – Fannie Mae

- Seattle Executives Join Opposition to New Tax to Fund Housing – Bloomberg

- Civil Rights Advocates Sue Ben Carson for Suspending Fair Housing Act Enforcement Rule – Slate

- Why Economists Don’t Like the Mortgage Interest Deduction – Federal Reserve Bank of St. Louis

- With the Foreclosure Crisis Behind Us, Have We Stopped Adding Single-Family Rentals? – Harvard Joint Center for Housing Studies

- How Recent Tax Reform Sounds a Clarion Call for Real Reform of Homeownership Policy – Tax Policy Center

On other countries:

- [Australia] A playful solution to the housing crisis – TED

- [Canada] High House Prices in Urban British Columbia: Foreign Buyer Fact or Fiction? – Kumtuks

- [Canada] Why High House Prices: Vancouver Academics vs Ottawa Economists – Kumtuks

- [Canada] Sam Sullivan blames government policies, not Chinese buyers, for high Vancouver housing prices – Straight

- [Canada] Montreal Is Canada’s Next Hot Housing Market – Bloomberg

- [China] North Korea Border Town Is Now China’s Hottest Property Market – Bloomberg

- [Colombia] Rental Housing in Bogota, Columbia: Challenges and Opportunities for Creating More Multifamily Properties – Cornell Real Estate Review

- [Spain] A Drone’s Eye View of Spain’s Housing Bubble – Citylab

Photo by Aliis Sinisalu

On cross-country:

- Housing and the Business Cycle Revisited – University of Augsburg

- Prime Global Cities Index – Q1 2018 – Knight Frank

- How 3D printing is revolutionizing the housing industry – TechCrunch

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts