Showing posts with label Global Housing Watch. Show all posts

Thursday, June 21, 2018

Housing Market in Denmark

The IMF’s latest report on Denmark says that:

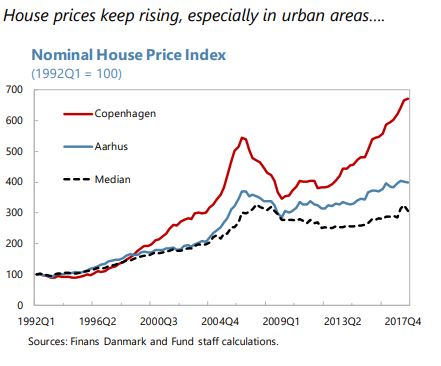

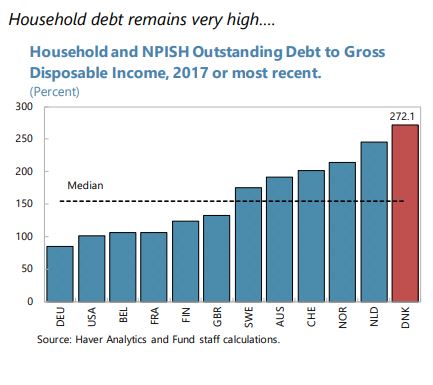

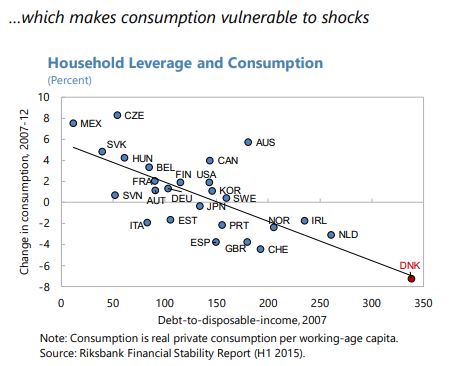

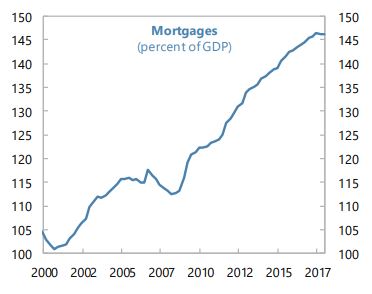

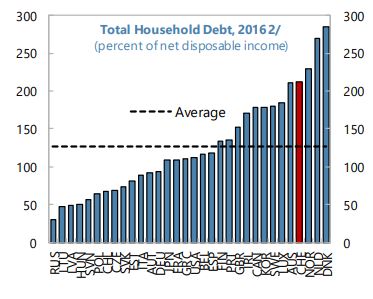

“The adverse feedback loops between housing and the real economy in Denmark are important. The centrality of housing in the Danish economy reflects at least three aspects. First, housing is a major asset of Danish households, together with pensions. Second, MCIs issue covered bonds to fund the mortgages provided to households, transferring part of mortgage risks to investors, mainly financial institutions, including pension funds and insurance companies (Figure 4). Third, because of the high real estate valuations and low interest rates, house purchases typically need to be funded via large mortgage multiples relative to disposable income. These factors help to explain why Danish households’ debt to income ratios are among the highest among advanced economies, and why consumption is sensitive to house price developments.

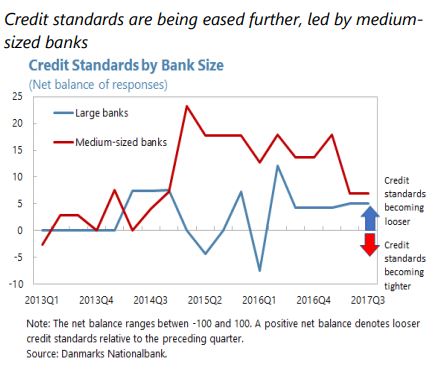

High household leverage combined with high and rising house prices could raise macrofinancial vulnerabilities. There is a risk that high and still rising house prices (particularly in urban areas), the relaxation of credit standards (Figure 4), and mortgage rates near all time-lows, may increase the perception of affordability across a broad spectrum of income levels. In this environment, two types of Danish households are particularly vulnerable to shocks. First, low-income households who spend more than 40 percent of their disposable income on housing (Figure 4). Second, households who have purchased in highly appreciating and potentially overvalued urban areas such as Copenhagen (Selected Issues), where LTI ratios and credit growth are noticeably higher than in the rest of the country. These vulnerabilities are compounded by the large proportion of variable-rate and interest-only mortgages in the system.

In recent years, authorities have implemented an extensive package of policies to address rising vulnerabilities. These include diverse macroprudential policies, 10 various supervisory guidance for MCIs and banks, and a reform of property taxation (Denmark 2017 Article IV report). The authorities continued building their macroprudential toolbox. Following the March 2017 Systemic Risk Council’s recommendation to limit lending via interest-only and floating-rate mortgages to high DTI households in areas with rapid housing prices growth, authorities introduced LTV restrictions. Effective from 2018, changes to consumer protection rules limit lending via interest-only and floating-rate mortgages to highly indebted households. Specifically, there are lending restrictions for households with DTI greater than 4 times and LTV greater than 60 percent: (i) the interest-rate fixation of floating-rate mortgages needs to be at least 5 years, and (ii) deferred amortization is only applicable on 30-year fixed-rate loans.

Coordinated policies are needed to tackle macro-financial vulnerabilities, including those stemming from excessive household leverage combined with rising house prices and affordability. Staff recognized authorities’ efforts and advocated continuing with the deployment of policies as follows.

Macroprudential instruments. The existing macroprudential measures should be tightened further. Staff analysis suggests that the LTV limit should be lowered from 95 to 90 percent to better protect households from house price declines. This decrease would lower aggregate consumption by about 1.5 percentage points one year after introduction, but increase it by 0.2 percentage points in a new steady-state because of lower debt-servicing costs (Denmark 2016 Article IV, Selected Issues). Thus, tightening the LTV limit would have a positive spillover by alleviating demand pressures in the near-term. DTI restrictions should be strengthened for all loans irrespective of LTV considerations. Tighter DTI limits for interest-only and adjustable-rate mortgages should also be considered to contain leverage, increase resilience, and limit the drag on consumption. Highly leveraged households—with debt-to-income above 400 percent—should be subject to mandatory amortization.11 To encourage further reduction of interest-rate sensitivity, the DTI limit could be calibrated to account for lower risk if financing is via fixed–rate mortgages.

Tax policy. Mortgage interest deductibility (MID) should be reduced further than currently planned, as MID distorts investment incentives and incentivizes leverage (Gruber, 2017). During the transition period to a lower mortgage deductibility regime, the current low rate environment would mitigate the adverse impact on homeowners. Also, fiscal savings from this measure could be used to reduce labor tax burden.

Housing supply. Restrictions on the size of new apartments should be relaxed in urban areas where demand-supply imbalances appear to have been a factor pushing valuations higher.

Simpler and more streamlined zoning and planning processes would allow housing supply to respond to increases in demand without steep price increases. Rent controls are among the highest in the EU and should be reduced to incentivize the rental market and alleviate demand for housing. Below-market rents limit the incentive to supply rental units, and incentivize the purchase of housing, adding upward pressure to property prices. Upgrading public and transport infrastructure—especially around inner-city areas experiencing strong house price growth—would help mitigate house prices pressures.The interaction between high household leverage and rising house prices poses macrofinancial risks. Authorities indicated that household resilience to interest rate increases likely improved as more homeowners had shifted towards fixed rate mortgages and longer fixing periods. But if risks continue to build up, the DN sees scope for tighter LTV limit, higher countercyclical capital buffer, amortization requirements and reduction of variable-rate loans. The government argued that additional measures would require further analysis of the effects on the housing market and the overall economy. The government considers unlikely that mortgage interest deductibility will be reduced beyond the planned gradual decline ending next year, and noted that mortgage interest deductibility should take into account balances towards other capital taxation rates.”

The IMF’s latest report on Denmark says that:

“The adverse feedback loops between housing and the real economy in Denmark are important. The centrality of housing in the Danish economy reflects at least three aspects. First, housing is a major asset of Danish households, together with pensions. Second, MCIs issue covered bonds to fund the mortgages provided to households, transferring part of mortgage risks to investors, mainly financial institutions, including pension funds and insurance companies (Figure 4).

Posted by at 11:23 AM

Labels: Global Housing Watch

Wednesday, June 20, 2018

Housing Market in Sri Lanka

From the IMF’s latest report on Sri Lanka:

- “Credit growth decelerated gradually to 14.7 percent (y/y) in December 2017 from its 28.5 percent peak in July 2016. However, credit to construction continued to grow rapidly at around 22.5 percent in 2017, reflecting buoyant real estate markets for both personal and commercial properties. Land prices in Colombo appreciated by 10.4 percent (y/y) in December 2017. Real lending rates stood at above 5 percent for most of 2017 but increased to about 7 percent in February 2018 with the deceleration in inflation. “

- “The authorities viewed the financial system as well-capitalized and stable. They did not see systemic risks arising from credit to the construction sector but agreed on the need to remain vigilant, especially in high segments of the real estate market. “

From the IMF’s latest report on Sri Lanka:

- “Credit growth decelerated gradually to 14.7 percent (y/y) in December 2017 from its 28.5 percent peak in July 2016. However, credit to construction continued to grow rapidly at around 22.5 percent in 2017, reflecting buoyant real estate markets for both personal and commercial properties. Land prices in Colombo appreciated by 10.4 percent (y/y) in December 2017. Real lending rates stood at above 5 percent for most of 2017 but increased to about 7 percent in February 2018 with the deceleration in inflation.

Posted by at 1:31 PM

Labels: Global Housing Watch

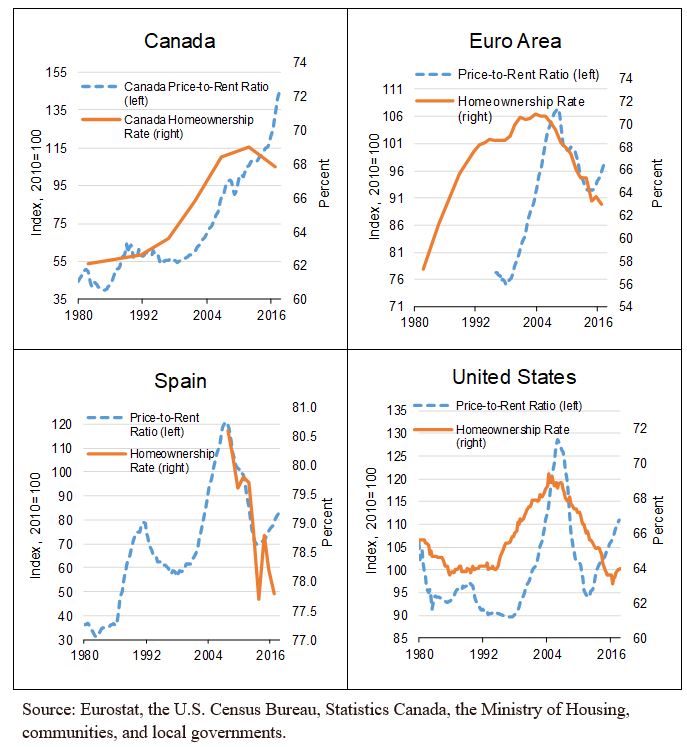

Are House Prices and Homeownership Moving in Tandem?

Global Housing Watch Newsletter: June 2018

In this interview, Carlos Garriga and Pedro Gete talk about their latest research: “Housing Recoveries without Homeowners: A Global Perspective.” Garriga is a Vice President at the Federal Reserve Bank of St. Louis. Gete is a Finance Professor at IE Business School.

Hites Ahir: “Housing Recoveries without Homeowners: A Global Perspective” is a blog that you recently co-authored with Daniel Eubanks (Federal Reserve Bank of St. Louis). What triggered your interest to work on this?

Carlos Garriga and Pedro Gete: Housing markets and housing finance are at the center of our research in macroeconomics. Housing played a key role in the lead up to the Great Recession, but also in the aftermath. Most of the new research has focused on analyzing that boom-bust cycle, ignoring the recovery period. We wanted to study what happened to housing markets after the Great Recession, and we found some new patterns that are surprisingly strong across countries.

Hites Ahir: What did you find?

Carlos Garriga and Pedro Gete: In the postwar period, booms in house prices have been accompanied by sizeable increases in homeownership; that is, an increase in the number of households that own the house they occupy. Historically, these two series have usually been positively related. Our research, however, finds an important change in the correlation between these series in the post-Great Recession period for a large number of countries, including the United States. We currently observe a decoupling of house prices and homeownership.

This shift changes the traditional cyclical view of homeownership and house prices. Normally, during a recovery, households buy houses, driving up house values. In the post-Great Recession period, however, we see global increases in house prices and decreases in homeownership. Thus, we identify a new stylized fact that decouples the variables, hence the title “Housing Recoveries without Homeowners.”

Hites Ahir: Is this good news or bad news?

Carlos Garriga and Pedro Gete: Well, the ownership of housing wealth is becoming concentrated among a smaller number of individuals. Whether this is good or bad news is difficult to assess, as we are still in the early stages of the research project documenting these novel facts. It is essential to understand the key driving forces before assessing the welfare effects and prescribing particular policies. The key issue is that in many countries and cities, the focus of the policy debate has changed: households are complaining that “rents are too high,” when the usual complaint used to be that “prices are unaffordable.”

Hites Ahir: Is this also happening in countries with different circumstances (e.g., diverging monetary policy rates)?

Carlos Garriga and Pedro Gete: The fact is very robust across countries, and in the United States it is very evident across most MSAs. We need more work to understand the exact drivers, but it does not seem to be that monetary policy alone can explain the fact.

Hites Ahir: So, we are transitioning from a nation of homeowners to a nation of renters. Has this type of development happened before?

Carlos Garriga and Pedro Gete: In the United States and United Kingdom, homeownership rates were low until post WWII. It seems this was the case in other countries as well. Going back even earlier, the homeownership rate was even lower, as the absence of credit markets makes it very difficult to undertake such a large investment as a house.

Figure 1: Homeownership and Price-to-Rent Ratio

Hites Ahir: What explains the decoupling of house prices and homeownership?

Carlos Garriga and Pedro Gete: Several factors could be driving the decoupling of the price-to-rent ratio and the homeownership rate. From the housing supply side, there is a trend toward decreased construction of starter and midsized housing units. Developers have increased the construction of large single-family homes at the expense of the other segments in the market. Recent increases in regulatory costs could have encouraged builders to focus on larger homes with higher margins. Supply may be just reacting to developments in demand (discussed next).

From the demand side, there are three leading explanations, which are likely to be complementary and self-reinforcing. The first focuses on changes in individual preferences or attitudes toward homeownership. The second builds on changes in the access to mortgage credit. The third tentative explanation relates to changes in the investment nature of real estate.

Hites Ahir: In your note, you say that the “price of houses is again increasing more quickly than the price of rentals.” But, as you know, in some countries, rents are controlled. So how do you reconcile this fact with your findings?

Carlos Garriga and Pedro Gete: It is true that in some countries and cities rent controls might limit the growth of one factor. There are also areas, however, with units not subject to controls that cause prices to rise faster than rents, for example, San Francisco and New York City.

Hites Ahir: In your blog, you also talk about “changes in the investment nature of real estate.” Could you elaborate on this?

Carlos Garriga and Pedro Gete: There are several types of real estate investors with different goals and targets in terms of the type of investment (i.e., single family vs. multi-family homes): First, there are sole proprietorship investors (i.e., “mom & pop”) looking for investment income. Second, there are foreign investors. Third, there are new institutional property owners, such Invitation Homes and American Homes 4 Rent, among others. In fact, since 2016, the real estate industry group has been elevated to the sector level in the S&P Dow Jones Indices.

Technology and globalization have made it easier for the second and third types to increase. For example, technology now makes it profitable to rent single-family houses. In addition, the widespread use of Internet rental portals such as Airbnb and VRBO has increased the opportunity to offer short-term leases, increasing the revenue stream from rental housing.

Hites Ahir: What is next for your research?

Carlos Garriga and Pedro Gete: A closely related issue is to what extent current homeownership rates are artificially high because of an aging population—a global phenomenon. The decline in the number of homeowners is observed across most age groups, but it is also true that the fraction of households over age 45 that are homeowners is substantially larger than for younger households. For this reason, population aging mechanically increases the homeownership rate. For example, in the United States, eliminating the aging effect would generate a homeownership rate of 60.9 percent instead of the observed 63.9 percent—suggesting the impact of aging is quite large. We have a lot of work to do, but we are enthusiastic the topic is worthy!

Global Housing Watch Newsletter: June 2018

In this interview, Carlos Garriga and Pedro Gete talk about their latest research: “Housing Recoveries without Homeowners: A Global Perspective.” Garriga is a Vice President at the Federal Reserve Bank of St. Louis. Gete is a Finance Professor at IE Business School.

Posted by at 5:01 AM

Labels: Global Housing Watch

Summer Reading: Recommendations by Experts on Housing Markets

Global Housing Watch Newsletter: June 2018

Looking for something to read over the summer? We asked experts for suggestions on books and papers to read on housing markets. Below are their picks:

Modeling Spatial Housing Markets: Theory, Analysis and Policy by Geoffrey Meen

Nominated by: John V. Duca (Federal Reserve Bank of Dallas)

Why? “The book provides a well-organized, systematic treatment of what drives house prices at national, regional, and metro levels. It describes and illustrates the importance of having reasonably complete data sets and well-specified models for estimating robust and useful housing relationships.”

Color of Law: A Forgotten History of How Our Government Segregated America by Richard Rothstein

Nominated by: Svenja Gudell (Zillow Group Chief Economist)

Why? “Rothstein outlines a history of housing discrimination that many people had forgotten – from government redlining to racial covenants – and shows how they have shaped our cities and neighborhoods. He makes the case that residential integration progressed from 1880 into the mid-twentieth century, then stalled. As we mark the 50th anniversary of the Fair Housing Act, this history offers important context for researching and trying to address our current housing issues. It’s a book everyone should read, not just economists and housing experts.”

The effect of housing supply regulation on housing affordability: A review by Raven Molloy

Nominated by: Christian Hilber (London School of Economics)

Why? “I recommend this short review article to scholars interested in understanding why the cost of housing has posed a growing weight on household budgets in recent decades and why genuine housing affordability crises have emerged in many desirable (superstar) cities such as London, San Francisco, or Shanghai. While many commentators recently pointed to lax credit conditions, low interest rates, or foreign investors—all affecting demand for housing—as ‘culprits’, this article focuses on the important role of housing supply regulation. It succinctly reviews the theoretical and empirical literature, identifies gaps in the literature, and provides some directions for further research.”

Evicted: Poverty and Profit in the American City by Matthew Desmond

Nominated by: Steve Malpezzi (University of Wisconsin-Madison)

Why? “Based on Desmond’s months of field research, Evicted recounts the stories of low-income tenants and their landlords in Milwaukee during nine months of 2008-9. From the book: “If incarceration had come to define the lives of men from impoverished black neighborhoods, eviction was shaping the lives of women. Poor black men were locked up. Poor black women were locked out.” Compelling stuff, but the book is even more powerful for the fact that Desmond spends half of his research time in a poor white trailer park, drawing many important parallels between the lives of poor whites and poor blacks, men and women; without neglecting the differences. Desmond goes beyond the simple stereotypical portraiture of rapacious landlords and benighted tenants, to paint complex and realistic portraits of both.”

No Price Like Home: Global House Prices 1870-2012 by Katharina Knoll, Moritz Schularick, and Thomas Steger

Nominated by: David Miles (Imperial College London)

Why? “This paper presents very carefully constructed estimates of house prices across 14 advanced economies since 1870. It uncovers a wealth of new facts about how housing markets have developed over the past 150 years. It presents a challenge to economists to explain some different patterns in prices at different times, in particular why it was that real house prices showed no consistent upwards trend in the period from 1870 to around the middle of the twentieth century but then tripled in the next 60 years.”

Supply restrictions, subprime lending and regional US house prices by André Kallåk Anundsen and Christian Heebøll

Nominated by: John Muellbauer (Nuffield College, Oxford)

Why? “This article analyses metropolitan house prices in the US providing micro-evidence of one aspect of the financial accelerator. They estimate a 3-equation model for the 2000-2006 boom period, including equations for the housing stock and cumulative sub-prime lending volumes, to capture shifting credit conditions, controlling for heterogeneity in supply elasticities. Lagged house price appreciation, a proxy for extrapolative expectations, has consequences for the credit equation, evidence for a financial accelerator, as well as the house price equation. Thus, house prices and credit are mutually reinforcing; tighter supply restrictions lead to a stronger financial accelerator.”

Days of Slaughter by Susan Wharton Gates

Nominated by: Frank E. Nothaft (CoreLogic)

Why? “September 2018 marks the 10th anniversary of the federal government’s placement of Fannie Mae and Freddie Mac into conservatorship. Yet not that long before that, the U.S. secondary mortgage market was the envy of many countries, an example of how other nations should set up their own mortgage markets. For a generation prior to the federal takeover, Fannie Mae and Freddie Mac provided an inexpensive and stable flow of funds to America’s homeowners. Days of Slaughter provides an insider’s view as to what were some economic, political, and management issues that led to the collapse of Freddie Mac.”

Metropolitan land Values by David Albouy, Gabriel Ehrlich and Minchul Shin

Nominated by: Albert Saiz (Massachusetts Institute of Technology)

Why? “This is a really interesting paper for everyone who wants to understand housing affordability in the United States. The authors use a new database of market transactions to study the importance of land costs on the overall price of housing. The authors do not use residual estimates, but actual land transactions, which makes their estimates more reliable.”

The New Urban Crisis: How Our Cities Are Increasing Inequality, Deepening Segregation, and Failing the Middle Class and What We Can Do About It by Richard Florida

Nominated by: Robert J. Shiller (Yale University)

Why? “I would recommend Richard Florida’s 2017 book: The New Urban Crisis, which tells us about a relation between rising inequality and urban dynamics. Rising inequality may be the most important economic issue facing the world today. His detailing the urban dimension of this is striking. His “winner-take-all urbanism” is connected to the geographical polarization of America today, and no doubt applies to other countries as well. Florida lives in Canada, where there is a similar real estate boom in superstar cities going on today.”

Milestones in European Housing Finance by Jens Lunde and Christine Whitehead

Nominated by: Susan Wachter (University of Pennsylvania)

Why? “In their edited volume, Milestones in European Housing Finance, Jens Lunde and Christine Whitehead offer a perspective of the past 25 years in European housing finance – a period including the transition from socialism, moves towards development of a common economic framework across the continent and of course, the Global Financial Crisis (GFC). By including treatises – provided by the most prominent country experts – on the development of individual nations’ housing finance systems as well as thematically-focused chapters, Lunde and Whitehead develop a view of not only the past quarter century, but also of keys for envisioning the future. This volume underlines the significance of cross-country comparisons in developing a path forward for housing finance systems across the globe.”

Photo by Pj Accetturo

Global Housing Watch Newsletter: June 2018

Looking for something to read over the summer? We asked experts for suggestions on books and papers to read on housing markets. Below are their picks:

Modeling Spatial Housing Markets: Theory, Analysis and Policy by Geoffrey Meen

Nominated by: John V. Duca (Federal Reserve Bank of Dallas)

Why? “The book provides a well-organized,

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, June 18, 2018

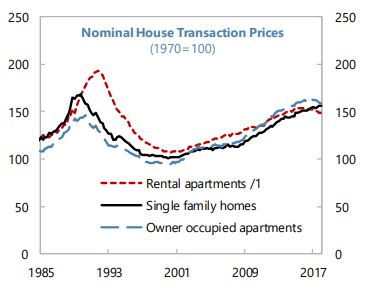

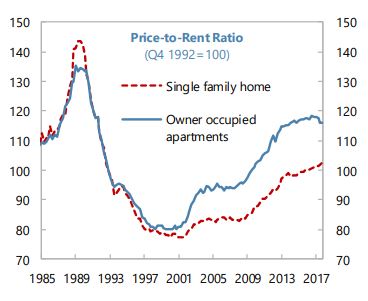

House Prices in Switzerland

The IMF’s latest report on Switzerland says that:

“Private sector leverage and real estate exposure is high. The growth rate of mortgage claims has slowed from a high base, but these claims increase by about 5 percentage points of GDP per year. Liquidity and capital of domestically-focused banks exceed regulatory minima, and profits have held up despite narrowing interest spreads. Following a series of macroprudential tightening measures during 2012–14, property prices subsequently stabilized, but have risen again recently alongside moderating mortgage interest rates. Reflecting their status as attractive global cities and internationally-traded assets, property prices in Geneva and Zurich have been among the fastest growing in the world. However, standard housing-price metrics do not indicate significant misalignment. Newer-vintage mortgages appear riskier, with nearly half exceeding indicative affordability thresholds and also carrying higher loan-to-value ratios, especially those for purchasing

investment properties.”

The IMF’s latest report on Switzerland says that:

“Private sector leverage and real estate exposure is high. The growth rate of mortgage claims has slowed from a high base, but these claims increase by about 5 percentage points of GDP per year. Liquidity and capital of domestically-focused banks exceed regulatory minima, and profits have held up despite narrowing interest spreads. Following a series of macroprudential tightening measures during 2012–14, property prices subsequently stabilized,

Posted by at 10:08 AM

Labels: Global Housing Watch

Subscribe to: Posts