Showing posts with label Global Housing Watch. Show all posts

Saturday, June 30, 2018

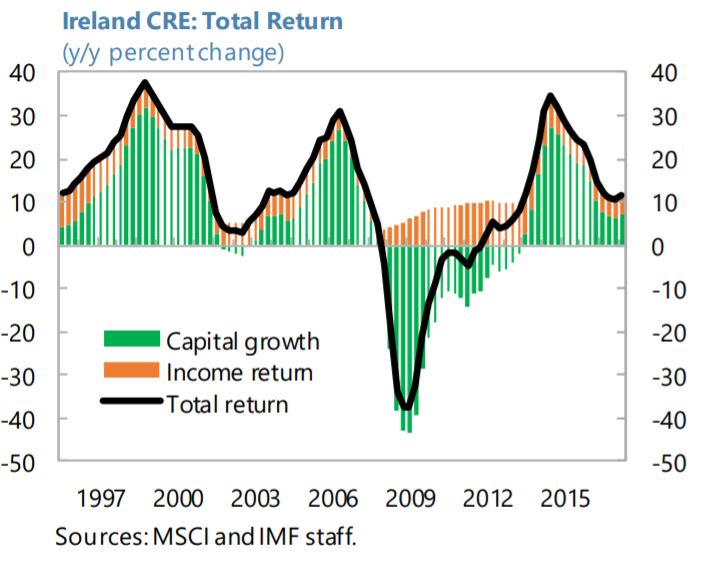

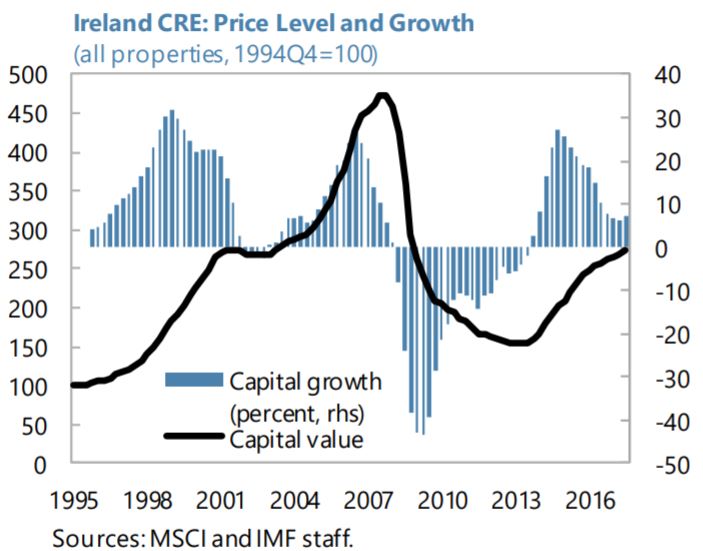

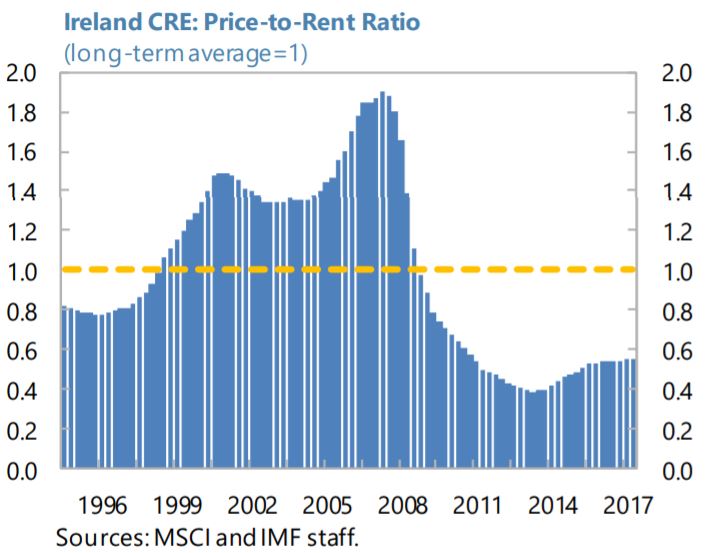

The Irish Commercial Real Estate Market: Synchronization and the Role of External Factors

The IMF’s latest report on Ireland says that:

“This chapter examines the synchronization of the Irish returns on commercial real estate (CRE) properties with those in peers to better understand the importance of external factors in explaining the high volatility of CRE returns in recent years. The analysis finds that the cyclical pattern of Irish CRE returns is highly corelated with that in other advanced economies, yet with much higher volatility. Moreover, a vector auto-regression (VAR) analysis points to a high impact of international CRE prices on Irish CRE prices, and to strong feedback effects between the latter and domestic economic activity. These findings underline the importance of continued close monitoring of this market to ensure that the financial system is resilient to possible drops in collateral values and investment flows.”

The IMF’s latest report on Ireland says that:

“This chapter examines the synchronization of the Irish returns on commercial real estate (CRE) properties with those in peers to better understand the importance of external factors in explaining the high volatility of CRE returns in recent years. The analysis finds that the cyclical pattern of Irish CRE returns is highly corelated with that in other advanced economies, yet with much higher volatility.

Posted by at 6:23 AM

Labels: Global Housing Watch

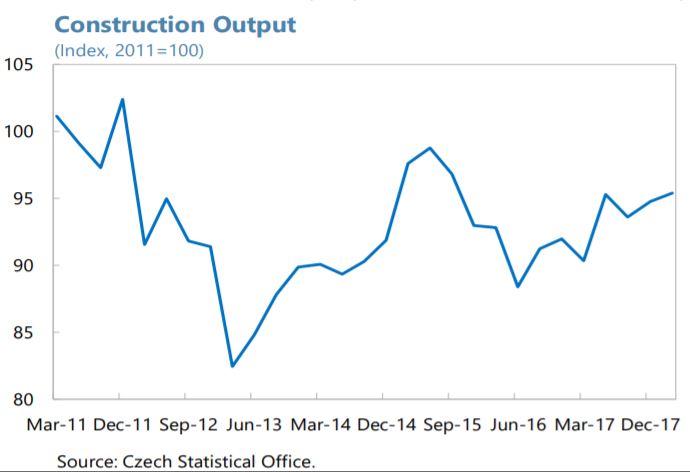

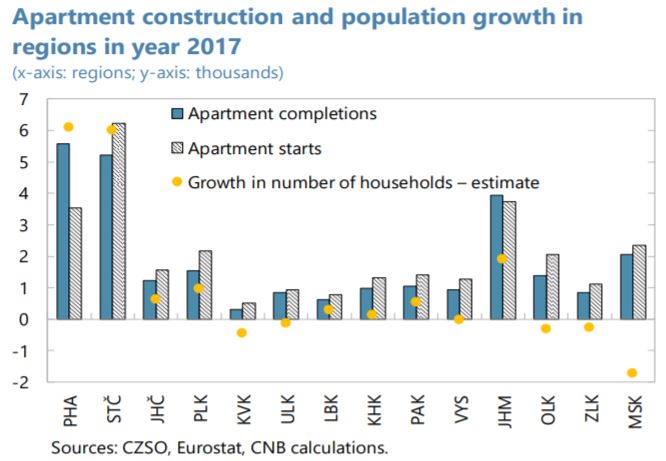

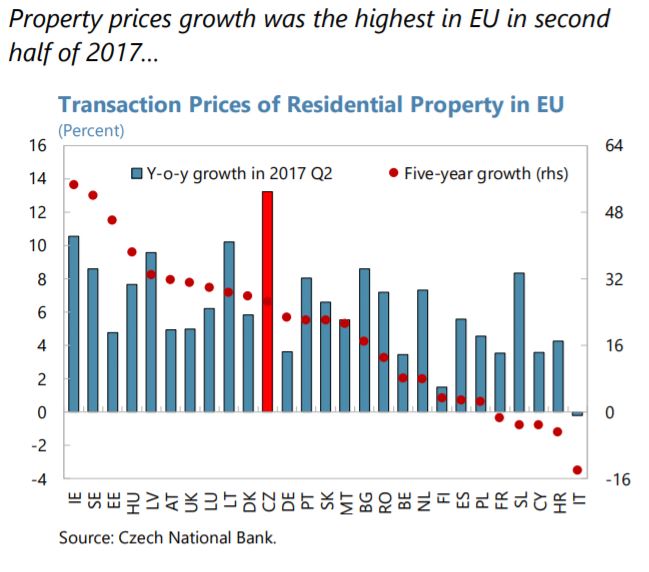

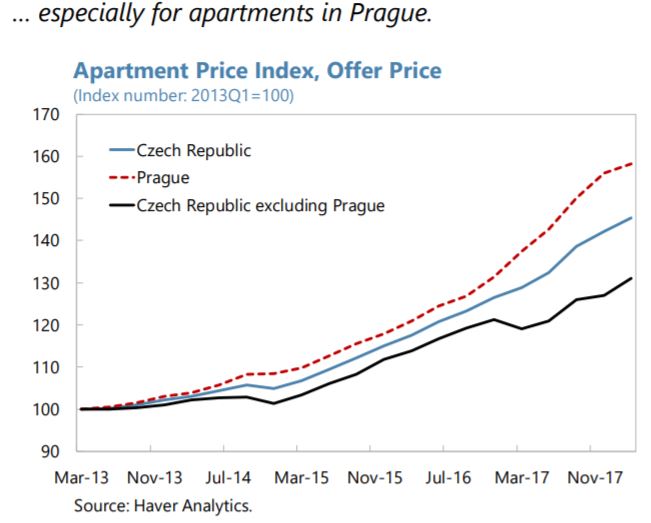

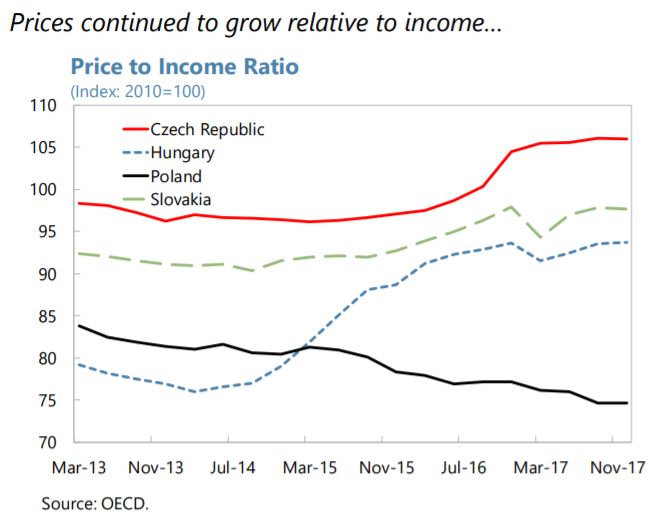

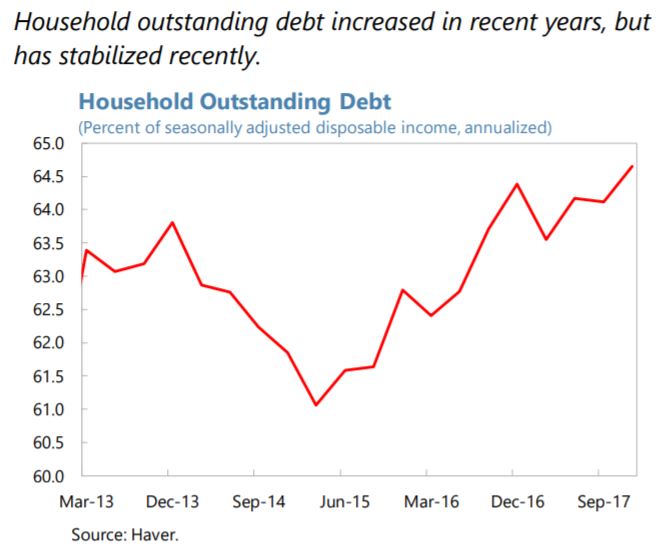

Housing Market in Czech Republic

The IMF’s latest report on Czech Republic says that:

“Construction activity declined after the financial crisis and has yet to recover to levels seen in 2009. The effect is particularly noticeable in Prague, for which housing completions have not kept pace with housing demand. Low numbers of housing starts imply that the problem will continue for some time. Demand has been driven mainly by migration within the country and strong demand for prime properties by foreigners; demand for investment properties is also believed to play a significant role.”

The report also says that:

“Private credit growth is in line with nominal GDP growth, but household lending is growing more quickly. Bank lending to residents eased to 4 percent (y/y) in April, of which loans to

resident non-financial corporations grew by only 1½ percent. However, loans to households

increased by 7½ percent; mortgage loans to households increased by 9½ percent, off the recent peak in mid-2017 of 10½ percent, but nonetheless outpacing nominal income growth. Consumer credit also grew relatively strongly.Some households are highly leveraged. The aggregate household debt-to-income (DTI)

ratio has not increased further over the year, given the strong growth of disposable income. But many households continue to borrow at high loan-to-income multiples (…), associated with escalating price-to-income and price-to-rent ratios (…).The CNB has tightened macroprudential recommendations (…). New, non-binding

recommendations implemented in 2017: Q2 included a 90 percent LTV cap on individual loans and a 15 percent cap on the share of new loans originated with LTV ratios between 80 and 90 percent. In June 2017, the CNB recommended that banks pay extra attention to debt-to-income and debt service-to-income ratios. Reported lending standards have subsequently tightened, and the share of new household mortgage loans with LTVs above 90 percent has declined, with many loans at around 80 percent LTV. However, concerns were expressed that this improvement may have been flattered by inflated valuations.Additional measures are needed to insure against household financial vulnerabilities. DTI ratios on new mortgages are only indirectly addressed by LTV restrictions—to safeguard

household finances, the financial authority needs more comprehensive tools and access to data sufficient for a comprehensive picture of households’ finances.

- The CNB should be given binding powers over maximum LTV, DTI, and Debt-Service-To-Income (DSTI) ratios as soon as possible. Debt-based measures would provide a more comprehensive assessment of financial risks than loan-based measures, and are increasingly standard in advanced economies. In the absence of legislation granting binding powers, the CNB should immediately issue recommendations over DTI and DSTI ratios, to reinforce those over LTVs and better target high leverage.

- If such “demand side” (i.e. borrower-based) tools are not implemented, additional “supply side” measures could be considered, but these would only indirectly address the underlying problem of high household leverage. Risk weight add-ons or minimum risk weights for property exposures could provide insurance against growing real estate exposures, but a substantial increase would likely be required to make a meaningful difference to lending conditions, given that capital ratios are above regulatory requirements. The CNB has discretion over capital requirements under Pillar II, but it is not guaranteed that the effects would “pass through” to mortgage borrowers.

Better data are needed for monitoring risks. The use of DTI and DSTI measures puts great

demands on data—to accurately assess risks and to be fully sure of compliance, the CNB needs access to comprehensive household loan data. Better data on commercial real estate transactions would also be helpful.Macroprudential measures should be supported by addressing fiscal and structural

policies. Increasing house prices in major metropolitan areas reflects equilibrium adjustment, and demand has consistently outstripped supply, especially in Prague. Planning and zoning laws contribute to housing supply constraints that add to pressures on prices. Some progress has been made in streamlining procedures for building permits, but construction levels remain below pre-crisis highs (…). In addition, the tax environment adds to housing demand (…). Without attention to such problems, the housing market is likely to remain tight.”

The IMF’s latest report on Czech Republic says that:

“Construction activity declined after the financial crisis and has yet to recover to levels seen in 2009. The effect is particularly noticeable in Prague, for which housing completions have not kept pace with housing demand. Low numbers of housing starts imply that the problem will continue for some time. Demand has been driven mainly by migration within the country and strong demand for prime properties by foreigners;

Posted by at 6:15 AM

Labels: Global Housing Watch

Friday, June 29, 2018

Housing View – June 29, 2018

On cross-country:

- Vivienda en Centroamérica – Instituto Centroamericano de Administración de Empresas (INCAE), CNN

- ‘Livability & Affordability in the Digitized City’ – Housing Europe

- Using evidence to make affordable housing a more attractive investment – Housing Europe

- The digitalisation of cities and housing: what will the future bring? – Sociology Lens

On the US:

- The State of the Nation’s Housing 2018 – Joint Center for Housing Studies

- Housing in the U.S. is too expensive, too cheap, and just right. It depends on where you live. – Brookings

- The big business of housing immigrant children – CNN

- Housing Inventory Tracking – Calculating Risk

- How Is Technology Changing the Mortgage Market? – Federal Reserve Bank of New York

- S. Housing Will Get Even Less Affordable – Bloomberg

- Fed’s Bostic to Hear Case for Excluding Housing From Inflation – Bloomberg

- BankThink FHFA needs to curb Fannie and Freddie’s insatiable appetites – American Banker

On other countries:

- [Canada] Nothing ‘nefarious’ about foreign-buyer tax: B.C. gov’t lawyer – Vancouver Sun

- [China] Why China Can’t Fix Its Housing Bubble – Bloomberg

- [France] Macron pone en jaque el modelo de vivienda social en Francia – El Salto

- [New Zealand] As Housing Prices Soar, New Zealand Tackles a Surge in Homelessness – New York Times

- [Nigeria] Nigerian Low-Cost Mortgage Lender Set for $1.4 Billion Boost – Bloomberg

- [Portugal] Portugal property boom accelerates in first quarter – Reuters

- [Singapore] Singapore Millennials Prefer Property – Bloomberg

- [Sweden] Giddy property prices are a test for Swedish policymakers – The Economist

- [United Arab Emirates] Dubai: To Build or not to Build? – REIDIN

- [United Kingdom] House prices tumble in seaside hot spots – BBC

- [United Kingdom] Buy-to-let landlords cool on property purchases – Financial Times

- [United Kingdom] Not in my back yard — conflicting views on the housing shortage – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Vivienda en Centroamérica – Instituto Centroamericano de Administración de Empresas (INCAE), CNN

- ‘Livability & Affordability in the Digitized City’ – Housing Europe

- Using evidence to make affordable housing a more attractive investment – Housing Europe

- The digitalisation of cities and housing: what will the future bring? – Sociology Lens

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, June 27, 2018

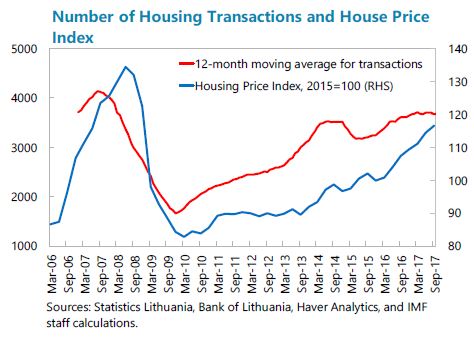

House Prices in Lithuania

The IMF’s latest report on Lithuania says that:

“Household credit remained strong, rising by 7 percent thanks to solid wage growth, and coincided with a surge in housing activity. The number of transactions in the real estate market rose sharply and neared the pre-crisis peak. Moreover, housing prices, especially in major urban centers, rose sharply, prompting the Bank of Lithuania (BoL) to raise the countercyclical capital buffer by 0.5 percentage points in December 2017. Nonetheless, the stock of credit is still modest at 41 percent of GDP, well below the pre-crisis peak of 68 percent of GDP. Similarly, housing prices remain significantly below their 2007 peak, especially when adjusted for inflation. Financial soundness indicators remain strong. Lithuania’s banking system is well capitalized, liquid, and profitable despite the low interest rate environment. Nevertheless, spillovers from real-estate related vulnerabilities in Nordic parent banks, which control most of Lithuania’s financial sector, remain a risk.”

The report also says:

“An analysis of Lithuania’s credit, housing price, and output cycles during 1995–2017Q3, reveals that housing price cycles are more frequent, but shorter-lived than the other two with credit cycles being the most volatile. The analysis finds strong synchronization among them in Lithuania, particularly between the credit and housing price cycles.

Lithuania’s cycles are highly synchronized with those of other Baltic and Nordic countries. This is particularly true for credit due to the close links of Lithuania’s financial system to parent bank developments. Housing price cycles are the least synchronized possibly because real estate markets are mostly affected by local conditions.

An econometric exercise shows that housing price booms are the key determinant of credit upturns. Other factors causing a credit upturn include the negative impact of the global financial crisis, bank profitability, deposit growth, interest rates, and private sector indebtedness. The presence of an economic boom does not seem to be a significant determinant of a credit upturn, suggesting that other, potentially external, factors play a more significant role.

A panel VAR that includes other variables potentially influencing credit demand and supply shows that Lithuania is more vulnerable to shocks than the region as a whole, and that credit and real GDP shocks in Lithuania have a particularly strong impact on Lithuania’s credit. Credit, housing price, and output shocks in other Baltic and Nordic countries on average also have a strong impact on Lithuania’s credit.”

The IMF’s latest report on Lithuania says that:

“Household credit remained strong, rising by 7 percent thanks to solid wage growth, and coincided with a surge in housing activity. The number of transactions in the real estate market rose sharply and neared the pre-crisis peak. Moreover, housing prices, especially in major urban centers, rose sharply, prompting the Bank of Lithuania (BoL) to raise the countercyclical capital buffer by 0.5 percentage points in December 2017.

Posted by at 6:56 AM

Labels: Global Housing Watch

Friday, June 22, 2018

Housing View – June 22, 2018

Journal of Housing Economics (June 2018 Volume)

- Race and the City by Ingrid Gould Ellen, Stephen L. Ross

- Are inclusionary housing programs color-blind? The case of Montgomery County MPDU program by Adji Fatou Diagne, Haydar Kurban, Benoit Schmutz

- The Visible Host: Does race guide Airbnb rental rates in San Francisco? by Venoo Kakar, Joel Voelz, Julia Wu, Julisa Franco

- Racial climate and homeownership by Timothy F. Harris, Aaron Yelowitz

- The non-financial costs of violent public disturbances: Emotional responses to the 2011 riots in England by Panka Bencsik

- Are central cities poor and non-white? by Jenny Schuetz, Jeff Larrimore, Ellen A. Merry, Barbara J. Robles, Arturo Gonzalez

- Racial segregation in the United States since the Great Depression: A dynamic segregation approach by Trevor Kollmann, Simone Marsiglio, Sandy Suardi

- The paradox of expanding ghettos and declining racial segregation in large U.S. metropolitan areas, 1970–2010 by Janice Fanning Madden, Matt Ruther

- Does segregation matter for Latinos? by Jorge De la Roca, Ingrid Gould Ellen, Justin Steil

- There’s no place like home: Racial disparities in household formation in the 2000s by Sandra Newman, Scott Holupka, Stephen L. Ross

On cross-country:

- The unaffordable city: Housing and transit in North American cities – Cities

- Rethinking Urban Sprawl: Moving Towards Sustainable Cities – OECD

- Innovando la política de vivienda a través del alquiler: de la ‘casa propia’ a una vivienda que sirva – Inter-American Development Bank

- How cities can lead the way in bridging the global housing gap – World Economic Forum

- Real Estate & Aging – UBS

On the US:

- Housing Wealth Effects: The Long View – NBER

- Don’t Blame Expensive Housing for Falling Fertility – Citylab

- The 0.25% Fed Rate Increase Doesn’t Mean Mortgage Rates Will Increase 0.25% – Forbes

- Climate Change May Already Be Hitting the Housing Market – Bloomberg

- Zillow Data Used To Project Impact Of Sea Level Rise On Real Estate – NPR

- The High Cost of Low Credit – Zillow

- Negative Equity Dips Below 10 Percent for First Time Since the Bottom of the Market – Zillow

- Birth Rates are Falling Most where Homes are Appreciating Fastest – Zillow

- Californians Are Leaving, Where Are They Looking to Go? – Trulia

- Housing: The Case for YIMBY (Yes, In My Back Yard!) – Foundation for Economic Education

- Threading the Needle of Fair Housing Law in a Gentrifying City with a Legacy of Discrimination – University of San Francisco

- S. Home Prices at Least Affordable Level Since Q3 2008 – ATTOM

On other countries:

- [China] China’s Home Prices Rise at Faster Pace Despite Curbs – Bloomberg

- [Ireland] Surging Irish Home Prices to Cool Off, Central Bank Chief Says – Bloomberg

- [Netherlands] Sizzling Amsterdam Housing Market Pushes People to Other Cities – Bloomberg

- [Spain] New Build Residential Snapshot – Q1 2018 – Knight Frank

- [United Arab Emirates] Dubai / Abu Dhabi Residential Property Price Indices: May 2018 Results – REIDIN

Photo by Aliis Sinisalu

Journal of Housing Economics (June 2018 Volume)

- Race and the City by Ingrid Gould Ellen, Stephen L. Ross

- Are inclusionary housing programs color-blind? The case of Montgomery County MPDU program by Adji Fatou Diagne, Haydar Kurban, Benoit Schmutz

- The Visible Host: Does race guide Airbnb rental rates in San Francisco? by Venoo Kakar, Joel Voelz, Julia Wu, Julisa Franco

- Racial climate and homeownership by Timothy F.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts