Showing posts with label Global Housing Watch. Show all posts

Thursday, July 5, 2018

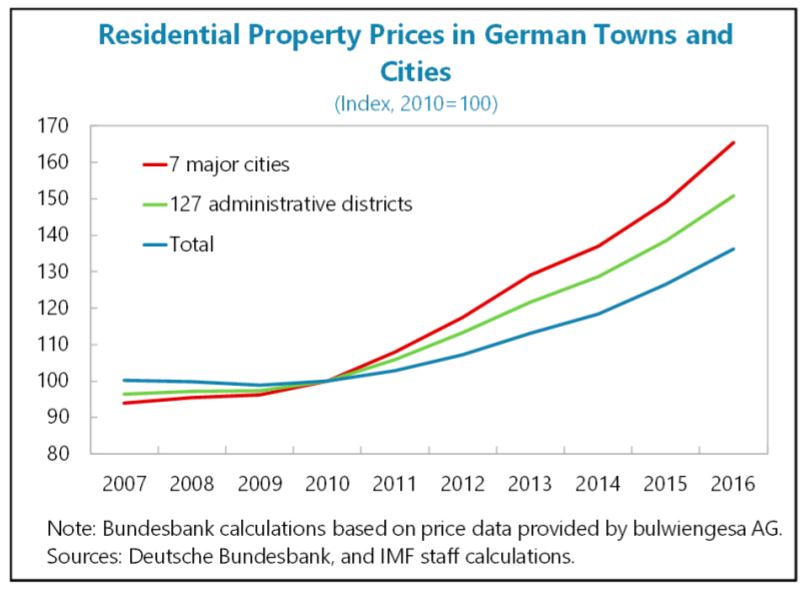

Germany’s Housing Market: Preventing Financial Excesses

The IMF’s latest report on Germany says that:

“Staff analysis suggests that house prices have risen faster than can be explained by demand and supply fundamentals in Germany’s major cities. House prices are rising moderately at the aggregate level, but have increased at double-digit rates in some hot spots where they

appear overvalued. Housing demand is driven by rising household income, large immigration flows in recent years, and low interest rates (…). On the supply side, stringent zoning restrictions (including for environmental protection) and high and rising capacity utilization (including labor shortages) in the construction sector prevent a more agile response of supply to price developments. House prices are most overvalued in Munich, Hamburg, Hannover, and Frankfurt, and are estimated to be more than 20 percent above their fundament level on average in major German cities (…). The Bundesbank obtains similar overvaluation estimates for some German cities in its latest assessment. As recommended in the past, lowering the effective burden of tax on new construction and reexamining zoning restrictions, in particular where demand is not likely to abate, would help mitigate price pressures.New housing policies, aimed at improving affordability, are not expected to have a

noticeable impact on prices. The government foresees spending €2 billion in renewed support for social housing in 2020–21, expanding the land available at a discount for social housing construction, and creating tax incentives to build on unused land. It also plans to allocate €2 billion to families with children acquiring a first home. Other measures are still being contemplated, including tax subsidies for rental housing, public loan guarantees and real estate tax exemptions to reduce equity requirements for owner-occupied houses, and strengthening rent controls. As these measures have counteracting effects on housing supply and demand, the overall impact on housing prices is likely to be small.Mortgage growth at the aggregate level has been moderate so far. Housing loans have

grown only marginally faster than GDP in recent years. German households are not highly leveraged (household debt stood at 53 percent of GDP at end-2017) and the overall debt-service-to-income ratio is low and declining (…). Mortgage lending spreads have compressed due to high competition among banks, but no widespread deterioration of lending conditions has been observed. Mortgage credit is recourse and based on fixed interest rates.However, data gaps prevent a full assessment of financial stability risks in the housing sector and should be urgently addressed. The absence of regional credit statistics and granular loan information prevents a full assessment of potential financial stability risks in specific market segments. The distribution of housing credit growth by type of bank, for instance, suggests that there could be important differences between major urban centers and the rest of the country. Given this, it is increasingly urgent that data gaps should be addressed.

The macroprudential toolkit should be strengthened. New tools—loan to value (LTV)

caps and amortization requirements—were legally created in 2017, a welcome development.

However, income-based instruments, such as the debt-to-income ratio and the debt-service-to income ratio, are not included in the legislation. These tools, which can help prevent an excessive build-up of debt by households when house prices are rising rapidly, should be added.Given rapidly rising house prices in some cities alongside data gaps that hinder a full

assessment of risks, early activation of macroprudential tools should be considered. As noted

in the 2016 Financial Sector Assessment Program (FSAP), international experience suggests that macroprudential tools should be deployed early to be most effective. It is therefore important that the macroprudential framework is sufficiently nimble such that instruments can be utilized preventatively to avoid the build-up of vulnerabilities. In Germany, early activation would help preserve financial stability by dampening risks of excessive leverage, especially in the context of insufficient data to assess whether pockets of vulnerability are arising. To the extent that vulnerabilities are not present, macroprudential measures—such as application of LTV caps and amortization requirements—would not likely be binding anyway. On this basis, consideration should be given to early activation of the existing macroprudential tools.Authorities’ Views

The Bundesbank monitors developments in the real estate markets closely, and authorities assess corresponding financial stability risks to be low. An early activation of borrower-based macroprudential tools is deemed unjustified at this stage and would face legal obstacles. They saw overvaluation concerns as localized and the lack of substantial credit growth or deterioration of credit standards, alongside households’ strong balance-sheets, as reassuring. They therefore saw no need for activation of LTV caps or amortization requirements at the present juncture. They fully shared staff’s concern over the information gaps which prevent a fuller assessment of risks. The authorities highlighted that microprudential tools are available and can be effectively used to address bank-specific concerns.”

The IMF’s latest report on Germany says that:

“Staff analysis suggests that house prices have risen faster than can be explained by demand and supply fundamentals in Germany’s major cities. House prices are rising moderately at the aggregate level, but have increased at double-digit rates in some hot spots where they

appear overvalued. Housing demand is driven by rising household income, large immigration flows in recent years, and low interest rates (…).

Posted by at 11:04 AM

Labels: Global Housing Watch

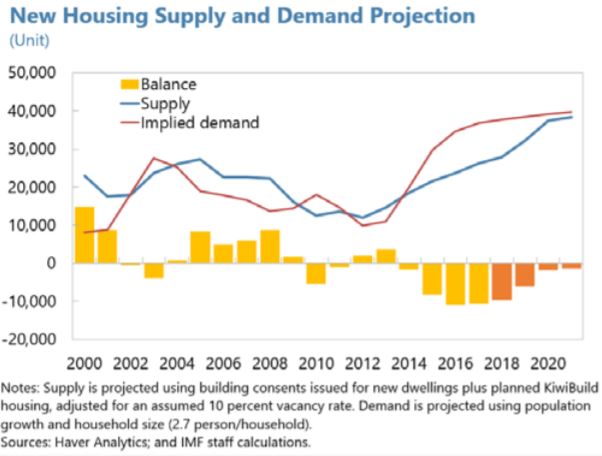

New Zealand: Managing Housing Market Imbalances

The IMF’s latest report on New Zealand says that:

“Context

The new government’s housing policy agenda focuses on direct supply initiatives, tax

policy changes, and restrictions on home ownership by nonresidents. Addressing declining

housing affordability has become a policy priority (…).

- Supply initiatives. Under the KiwiBuild program, the government plans to build 100,000 affordable houses over 10 years (about one third of average annual residential building authorizations) for first-time homebuyers. After initial financing of NZ$2 billion, the program would be sustained through the sales of completed houses.

- Addressing other supply constraints. Besides the KiwiBuild program, the Urban Growth

Agenda aims to increase the availability of developable land and the supply response to higher house prices by addressing regulatory, planning and other policy constraints, including the underfunding of locally-provided infrastructure.

- Tax policy changes. To dampen property speculation, more residential property sales will be subject to capital gains taxes, as the related bright-line test has been extended from a two-year to a five-year holding period. Residential properties other than main home acquired after March 29, 2018 will be subject to capital gain taxes if disposed of within five years of acquisition. The government also proposed to limit negative gearing from rental properties, such that the deductibility of net losses from property investment (and interest costs) from other taxable income would be eliminated. A Tax Working Group is considering possible additional reform, including a broader capital gains tax on real estate investment and land tax reform.

- Restrictions on nonresidents’ real estate purchases. A proposed ban in a draft amendment to the Overseas Investment Act is scheduled for a parliamentary vote as early as late June 2018. Under the amendment, all residential land would be re-classified as “sensitive land,” which would require approval for foreign buyers under tighter qualifying criteria.

Staff’s Views

The housing policy agenda appropriately focuses on closing key gaps on the supply

side and in the tax system. While demand-side drivers have stabilized, they remain robust, and improved housing affordability ultimately requires a stronger housing supply response. These measures are complementary, and the success of the housing policy agenda will depend on well coordinated progress on all fronts. While the large scale of the KiwiBuild program can provide the certainty needed to redirect builders’ incentives toward lower-price housing and adopt new, more cost-effective building technology, the direct market intervention by the government also comes with risks to the budget and risks of crowding out private housing supply and market distortions more broadly. The Tax Working Group should also consider raising land taxes, which are efficient and would increase the recurrent cost of holding land, thereby encouraging its (re)development.A ban of residential real estate purchases by nonresidents is unlikely to improve housing affordability significantly. The proposed draft amendment to the Overseas Investment Act would be a capital flow management measure (CFM) under the IMF’s Institutional View (IV) on capital flows, as it would introduce discrimination based on residency and thus limit capital flows by its design. Its use would not be in line with the IV. While macroeconomic and macroprudential policy settings are broadly appropriate, available data suggest that foreign buyers appear to have played a minor role in New Zealand’s residential real estate markets recently. And in its current design, the CFM is unlikely to be temporary or targeted. The broad housing policy agenda above, if fully implemented, would address most of the potential problems associated with foreign buyers on a non-discriminatory basis.

Authorities’ Views

The authorities concurred that restoring housing affordability required a focus on

strengthening supply and lowering tax distortions. They noted that measures to intensify

competition in land markets via the Urban Growth Agenda would not be sufficient. Direct

intervention, through the KiwiBuild program, was also required. On tax policy, while the extension of the bright-line test to five years for capital gains taxation on non-primary residences is now in place, a wider set of reforms are being considered to the tax treatment of residential real estate investment. This includes ring-fencing negative gearing on investment properties. The Tax Working Group has been directed to consider whether a system of taxing capital gains or land (not applying to the family home or the land under it), or other housing tax measures, would improve the tax system.The authorities disagreed with the assessment that a ban on residential real estate

purchases by nonresidents, if implemented, would be a CFM under the IV. They emphasized

that the ban must be assessed holistically, taking into account the broader social, economic and political context. Declining housing affordability and greater inequality have become a major concern, which has lowered approval of globalization and immigration in New Zealand. Given the central role that home ownership plays in New Zealanders’ sense of well being, the government has taken steps to ensure that housing prices will be shaped by domestic market forces. If the government had not committed to extend its domestic screening regime for sensitive New Zealand assets to residential land, it would not have been able to secure the public’s support for additional international trade agreements. The authorities noted that the proposed screening regime will allow nonresidents to obtain consent to acquire residential land where they are committed to reside and become tax residents, in New Zealand; where their investment will increase housing supply; or where they will develop the land for other purposes (such as commercial premises). They also think that the new regime will help ensure that foreign direct investment flows into the productive economy rather than unproductive speculation. Finally, the authorities do not consider this measure to be a CFM; it will only have a limited effect on aggregate capital flows or the balance of payments, and it will have no material impact on the broader direction of or the openness of New Zealand’s economy.”

The IMF’s latest report on New Zealand says that:

“Context

The new government’s housing policy agenda focuses on direct supply initiatives, tax

policy changes, and restrictions on home ownership by nonresidents. Addressing declining

housing affordability has become a policy priority (…).

- Supply initiatives. Under the KiwiBuild program, the government plans to build 100,000 affordable houses over 10 years (about one third of average annual residential building authorizations) for first-time homebuyers.

Posted by at 10:48 AM

Labels: Global Housing Watch

Wednesday, July 4, 2018

Housing in the United States

The IMF’s latest report on the United States says that:

“Housing finance and the U.S. housing market have not been reformed comprehensively. To date, no legislative or executive action has been taken to reduce substantially the footprint of Fannie Mae and Freddie Mac (“Enterprises”). However, as conservator, the Federal Housing Finance Agency (FHFA) has required market-based credit risk transfers from the Enterprises to the private sector at an increasing level since 2013. The Enterprises have also jointly developed a common securitization platform and have announced that they will issue a new uniform mortgage backed security starting June 2019. These Enterprise reforms have been accomplished administratively and have not reformed the entire housing finance system, which would require legislative action.

Since 2015, the FHFA has directed the Enterprises to fund the Housing Trust Fund and Capital Magnet Funds (as required by the 2008 Housing and Economic Recovery Act) by transferring a portion of total new acquisitions to these funds, which are administered by the Department of Housing and Urban Development and Treasury Department, respectively.

FHFA has the discretion to suspend the Enterprise allocations to the affordable housing funds, including the Housing Trust Fund, if the allocations are contributing to the Enterprise’s financial instability. Moreover, the Senior Preferred Stock Purchase Agreements (PSPA’s) are sources of strength for the Enterprises. Indeed, the PSPA’s between the Treasury and each Enterprise both ensure the ability of each Enterprise to meet its financial obligations and to ensure that they will have minimal net worth as all profits above the capital reserve amount are transferred to Treasury each quarter. The capital reserve amount had been declining by $600 million per year and was scheduled to decline to $0 on January 1, 2018. However, on December 21, 2017, FHFA and the Department of the Treasury agreed to reinstate a $3 billion capital reserve amount for each Enterprise to prevent draws on the PSPA due to fluctuations in the Enterprises’ income due to the normal course of business. Despite the new capital reserve, the December 2017 tax cuts caused the Enterprises to draw a combined total of $4 billion at the end of that quarter. Policymakers have been evaluating and developing a potential comprehensive overhaul of the mortgage finance system over ten years after the federal government took control of Fannie Mae and Freddie Mac that could shrink or eventually close the two entities and create a system with more private capital. The Congressional Budget Office (CBO) has provided analyses on these issues. One such analysis prepared at the request of the Chairman of the House Committee on Financial Services, analyzed alternatives for attracting more private capital to the secondary mortgage market and alternative structures for that market, including a fully federal agency, a hybrid, public-private market, a market with a government guarantor of last resort, and a largely private secondary market.In 2018, the U.S. Senate passed The Economic Grown, Regulatory Relief and Consumer Protection Act (S. 2155), which has emphasized providing regulatory relief for small banks and credit unions and amending the Dodd-Frank Act. Moreover, on June 12, 2017, the Department of the Treasury published a comprehensive report containing recommendations for the financial regulation of banks and credit unions (“A Financial System that Creates Economic Opportunities: Banks and Credit Unions”).”

The IMF’s latest report on the United States says that:

“Housing finance and the U.S. housing market have not been reformed comprehensively. To date, no legislative or executive action has been taken to reduce substantially the footprint of Fannie Mae and Freddie Mac (“Enterprises”). However, as conservator, the Federal Housing Finance Agency (FHFA) has required market-based credit risk transfers from the Enterprises to the private sector at an increasing level since 2013.

Posted by at 2:11 PM

Labels: Global Housing Watch

Housing Affordability in New Zealand and Policy Response

The IMF’s latest report on New Zealand says that:

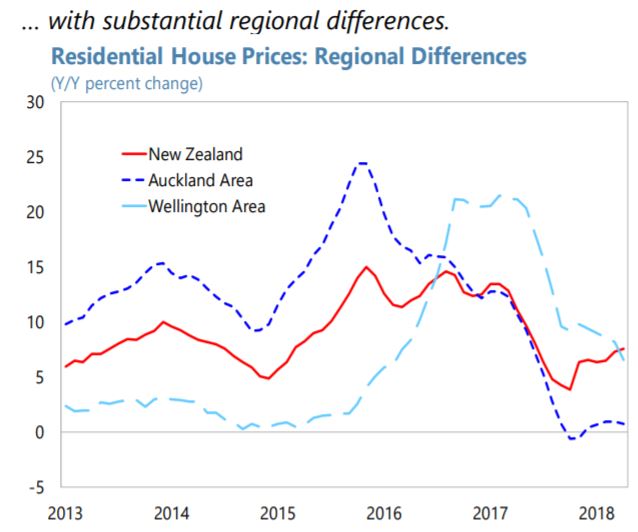

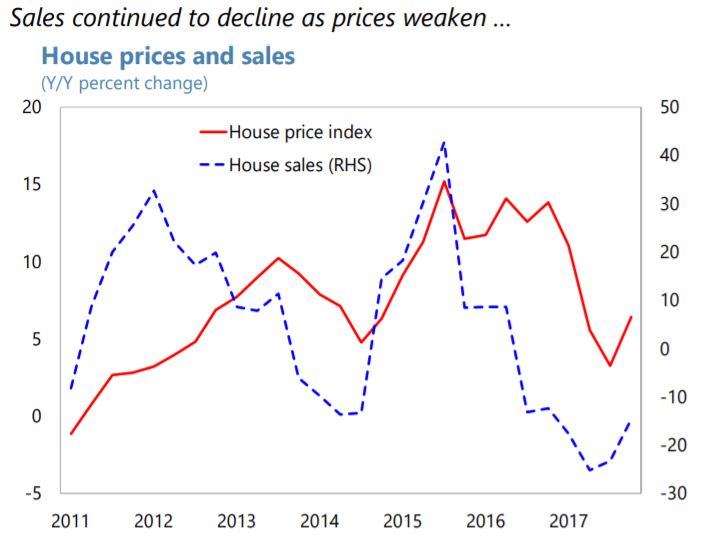

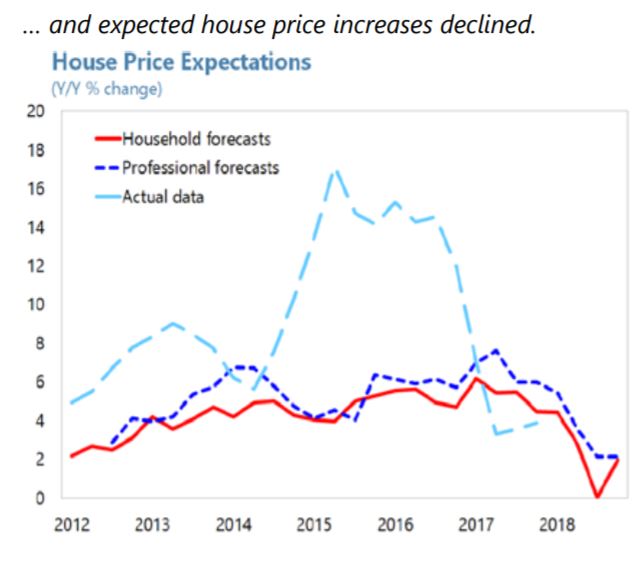

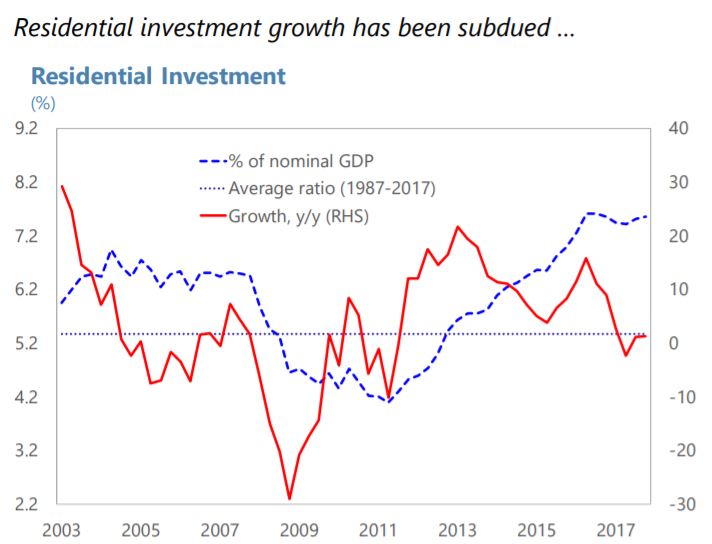

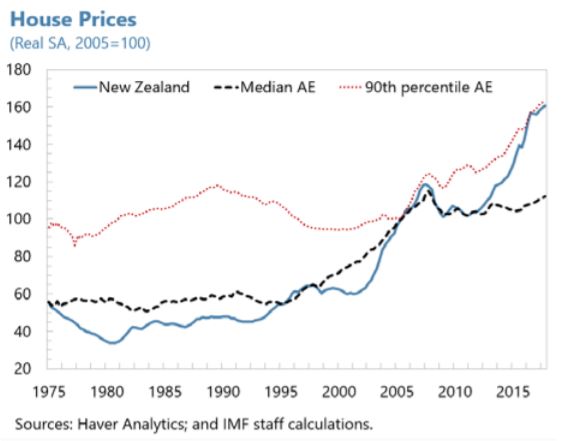

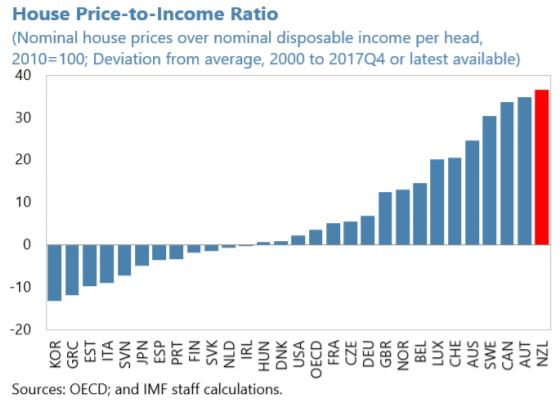

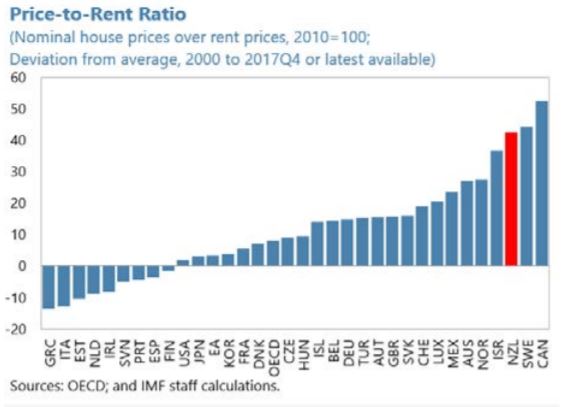

“The housing market is cooling but managing housing-related risks remain challenging.

Rising house prices were associated with rapid household credit growth through 2016. Given the slower rise in income, house price-to-income ratios reached unprecedented levels, especially in Auckland where the surge in house prices has been stronger. Household credit growth has moderated in 2017 while household debt continued to rise from already high levels. Given the underlying shortages in housing supply, the moderation in house prices is expected to be slow.Affordability concerns have also become more pressing, especially for first-time home

buyers. The deterioration in housing affordability because of high house prices as measured by housing cost to income has been partially offset by lower interest rates. Lower income groups remain more adversely affected by declining housing affordability. Rising house prices pose increasing difficulties for first-time home buyers entering the home market as it increases the length of time needed to save for a mortgage down payment regardless of the level of interest rates, and lead to higher debt servicing requirements as they need to have a larger mortgage than in the past.The housing policy agenda is ambitious and appropriately focuses on closing key gaps

on the supply side and in the tax system. Housing supply shortfalls have contributed to the runup in house prices, reflecting supply constraints amid strong demand fundamentals, including rising net migration, lower interest rates, and stronger income growth. While demand-side drivers have stabilized, they remain robust, and improved housing affordability requires eliminating supply bottlenecks. Supply and demand sides reforms are complementary, and the success of the housing policy agenda will depend on well-coordinated progress on all fronts.Lastly, improving the availability of housing affordability and other related statistical data is important. Further effort to compile and regularly release key housing related indicators such as house prices, housing costs, housing ownership and affordability measures would help to

enhance analysis and inform policy decisions.”

The IMF’s latest report on New Zealand says that:

“The housing market is cooling but managing housing-related risks remain challenging.

Rising house prices were associated with rapid household credit growth through 2016. Given the slower rise in income, house price-to-income ratios reached unprecedented levels, especially in Auckland where the surge in house prices has been stronger. Household credit growth has moderated in 2017 while household debt continued to rise from already high levels.

Posted by at 1:33 PM

Labels: Global Housing Watch

Saturday, June 30, 2018

Housing: Is This Time Different?

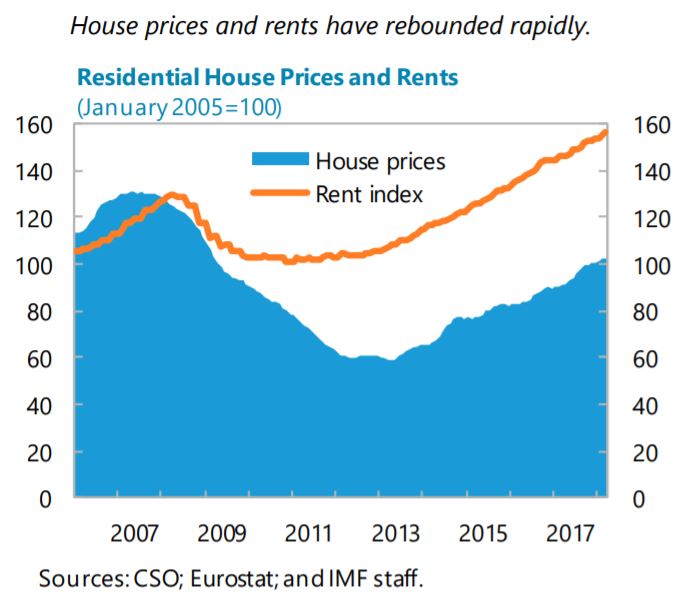

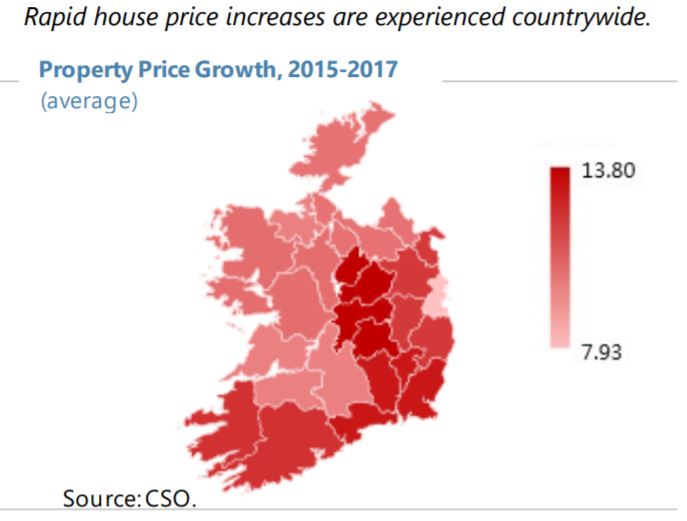

The IMF’s latest report on Ireland says that:

“As in the run-up to the crisis, the ongoing strong economic momentum is accompanied by a surge in house prices and rents. While house prices remain well below the pre-crisis peak, they have rebounded rapidly in Dublin and other regions, posting an average annual increase of 13 percent in March 2018. Rents have also increased at a strong pace (6 percent as of

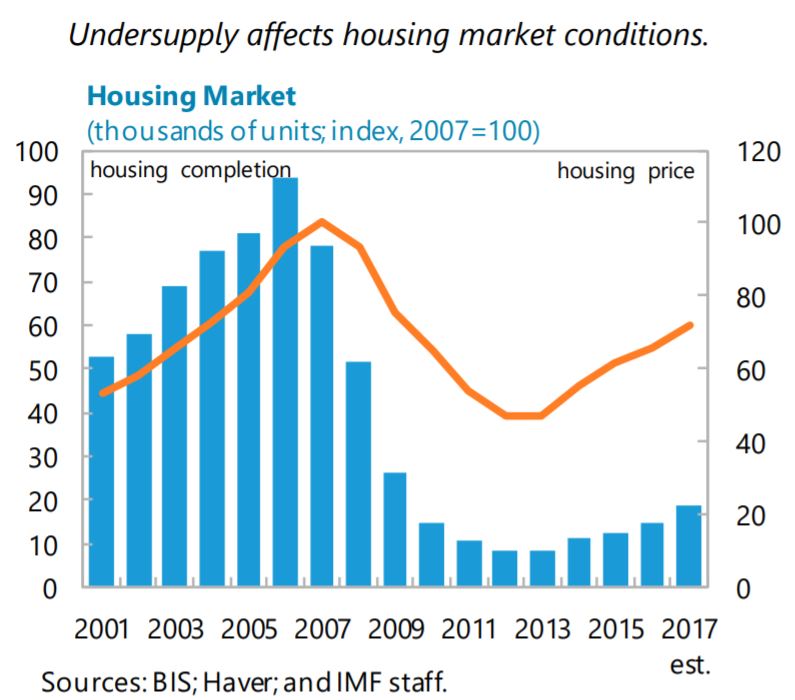

end-2017) and surpassed their pre-crisis level.Unlike in the pre-crisis period, house prices are fueled by a persistent supply shortfall

rather than by bank credit. Housing demand has recovered strongly, reflecting improved labor market conditions, rising incomes, and low interest rates. While mortgage drawdowns and approvals have rapidly increased, albeit from a low base, cash transactions remain relevant. In contrast, the recovery of the housing supply has been modest so far, with house completions falling well below the estimated underlying demand of about 35,000 units per year. The government has taken several measures to help boost supply (…) but these will need time to have an impact. High building costs, impaired balance sheets of construction firms and related funding difficulties, skill shortages, and land hoarding are the main factors holding back supply. In CRE properties, high yield attracted strong investment, largely from abroad, alleviating financing constraints and resulting in a fast supply response. Returns have moderated to levels seen in peers, after years of strong gains.While house prices are not significantly misaligned, upward pressure is likely to persist. Price-to-income and priceto-rent ratios have steadily increased in recent years and at present modestly exceed their historical average. However, model-based measures of house price misalignment are inconclusive with results ranging from some undervaluation (ESRI) to a small overvaluation. While there are no immediate financial stability risks, house price pressures are likely to persist over the medium term, as demand growth is

likely to continue outpacing supply.Against this backdrop, priority should be given to encourage greater housing supply…

- Further rationalization of building regulations and streamlining of planning processes are warranted. Reducing skills gaps in the construction sector, advancing debt restructuring of distressed but viable construction firms, and improving their access to financing are important.

- The establishment of the HBFI could provide funding to financially-constrained developers in the residential market. However, its operations should remain limited in scope and subject to prudent risk assessment and a robust governance structure to minimize risks for public finances.

- With a view to reducing land hoarding, a vacant site levy will be introduced starting

in 2019. However, its rates (3 percent for the first year and 7 percent for the second

and subsequent years) should be reviewed periodically to ensure effectiveness.

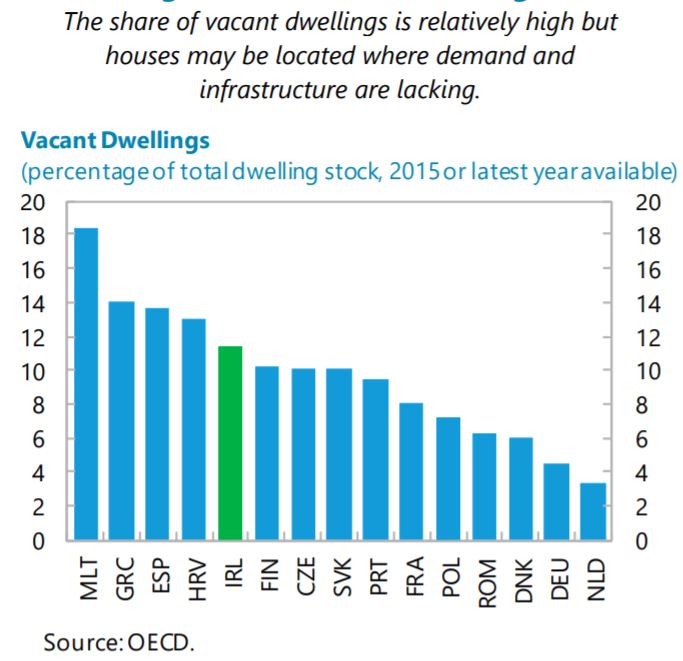

- Ireland has a high level of vacant dwellings, though some of these are located in areas

where demand and infrastructure are lacking. To ensure greater utilization of these properties, consideration should be given to adopting a surcharge on properties that are left vacant in urban areas.…while enacted measures to improve housing affordability need to be well-targeted…

- There is scope to re-calibrate the Help-to-Buy scheme, which provides a tax rebate of up to 5 percent of the dwelling purchase price for FTBs, towards low-income households.

- Measures to stabilize rents should be reconsidered as they may deter new construction. Support for disadvantaged groups should be delivered through well-targeted housing assistance payments.

- The RIHL, which provides loans to risky borrowers outside the banking system, should remain of limited scope and subject to stringent risk assessment to safeguard financial stability, particularly because the use of the RIHL might breach the central bank’s loan-to-income (LTI) limits.

…and macroprudential policy should continue to be deployed proactively. Following

last November’s review of mortgage measures, the central bank has kept the core parameters of the macroprudential framework intact, while halving the proportion of new non-FTB loans allowed to exceed the 3.5 LTI limit to 10 percent. Although currently appropriate, it is crucial that the macroprudential limits are adjusted pre-emptively to ensure that bank and household balance sheets remain resilient to shocks. In addition, as the Central Credit Registry becomes operational in 2018, staff encourages the authorities to shift from a LTI to a debt-to-income limit, which better captures household repayment capacity, once comprehensive data on household debt are available.”

The IMF’s latest report on Ireland says that:

“As in the run-up to the crisis, the ongoing strong economic momentum is accompanied by a surge in house prices and rents. While house prices remain well below the pre-crisis peak, they have rebounded rapidly in Dublin and other regions, posting an average annual increase of 13 percent in March 2018. Rents have also increased at a strong pace (6 percent as of

end-2017) and surpassed their pre-crisis level.

Posted by at 6:48 AM

Labels: Global Housing Watch

Subscribe to: Posts