Showing posts with label Global Housing Watch. Show all posts

Thursday, October 18, 2018

Assessing Housing Risk

From Money and Banking:

“Housing debt typically is on the short list of key sources of risk in modern financial systems and economies. The reasons are simple: there is plenty of it; it often sits on the balance sheets of leveraged intermediaries, creating a large common exposure; as collateralized debt, its value is sensitive to the fluctuations of housing prices (which are volatile and correlated with the business cycle), resulting in a large undiversifiable risk; and, changes in housing leverage (based on market value) influence the economy through their impact on both household spending and the financial system (see, for example, Mian and Sufi).

In this post, we discuss ways to assess housing risk—that is, the risk that house price declines could result (as they did in the financial crisis) in negative equity for many homeowners. Absent an income shock—say, from illness or job loss—negative equity need not lead to delinquency (let alone default), but it sharply raises that likelihood at the same time that it can depress spending. As it turns out, housing leverage by itself is not a terribly useful leading indicator: it can appear low merely because housing prices are unsustainably high, or high because housing prices are temporarily low. That alone provides a powerful argument for regular stress-testing of housing leverage. And, because housing markets tend to be highly localized—with substantial geographic differences in both the level and the volatility of prices—it is essential that testing be at the local level.”

Continue reading here.

From Money and Banking:

“Housing debt typically is on the short list of key sources of risk in modern financial systems and economies. The reasons are simple: there is plenty of it; it often sits on the balance sheets of leveraged intermediaries, creating a large common exposure; as collateralized debt, its value is sensitive to the fluctuations of housing prices (which are volatile and correlated with the business cycle),

Posted by at 8:19 AM

Labels: Global Housing Watch

Tuesday, October 16, 2018

Housing and Macroeconomics

Global Housing Watch Newsletter: October 2018

*Below is a summary of a workshop prepared by Benjamin Larin (Leipzig University), Hans Torben Löfflad (Leipzig University), Konstantin Gantert (Leipzig University).

What drives house price fluctuations? How do fluctuations in house prices and credit affect the real economy? What explains the long-run dynamics of house prices? How do house prices and rents affect wealth inequality and individual welfare? These are some of the questions that were discussed at a recent event.

The European Association of Young Economists (EAYE), in collaboration with Leipzig University, organized the first EAYE Workshop on Housing and Macroeconomics. This newly established workshop will take place annually and will focus on a specific topic. The workshop is organized by young economists, and it is meant for young economists. This year’s keynote lectures were Moritz Kuhn (University of Bonn, CEPR, IZA) and Alberto Martín (ECB, CREI, Barcelona GSE). What follows is a summary of this year’s workshop.

Credit cycles, housing, and short-term fluctuations

How credit and the real side of the economy are linked, and how financial shocks translate to changes in GDP—this is one of the questions that was asked frequently at the workshop. One paper analyzed the effects of credit expansion on aggregate demand in Denmark. The authors find that additional demand due to credit expansion is mostly spend in the non-tradable sector. Employment increases, mostly at small firms, yet the average labor separation rate is found to be higher for those jobs. Another paper analyzed the supply side effects of housing on the macroeconomy. The authors found that housing supply elasticities have decreased over the course of the last two US housing boom-bust episodes, implying more volatile house prices.

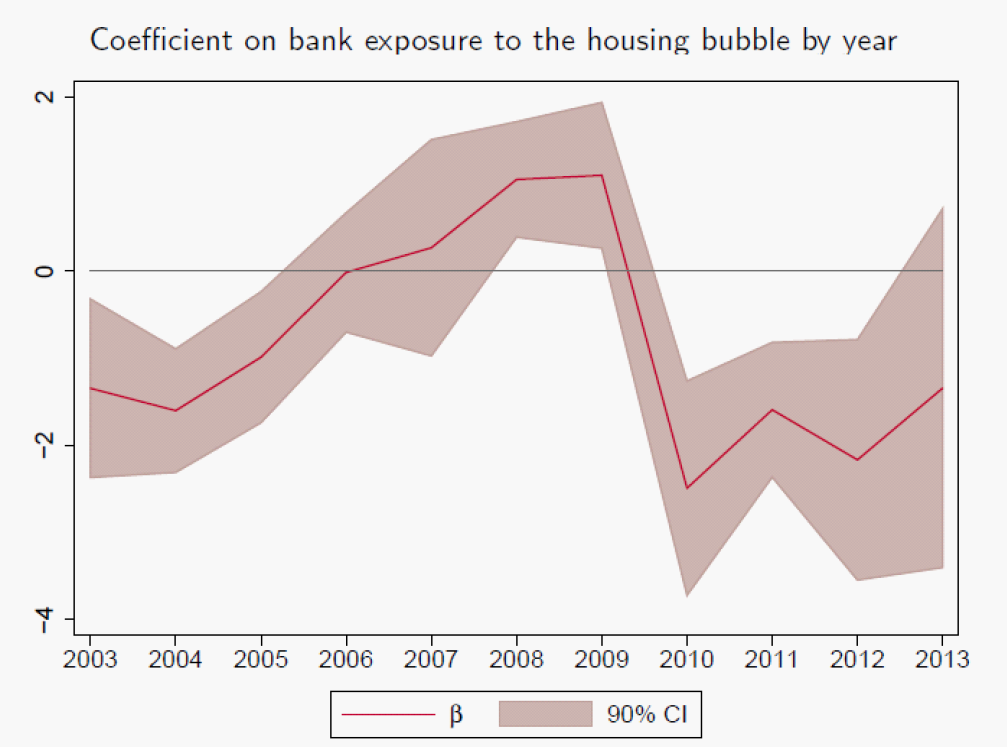

In the first keynote lecture, Alberto Martin presented a theory of macroeconomics of rational bubbles with an application to housing bubbles. He showed that a housing bubble leads to investment into the housing sector, first crowding out investment in non-housing firms (see figure 1). As bank capital increases over time, credit to non-housing firms increases as well. As the housing bubble bursts, this development reverses as credit lines freeze.

Figure 1.

Note: Coefficient of housing credit exposure of banks on credit growth to non-financial firms in the U.S. from 2003 to 2013. A value below 0 indicates a fall in credit to non-housing firms as the exposure to housing credit of a bank increases.

The real effects of housing credit on the macroeconomy are driven by changes in the credit side of the economy. A paper presented preliminary evidence that there is again a housing bubble in the U.S. and in other OECD economies. The housing bubbles in the U.S. seem to be geographically clustered, yet county specific factors cannot explain this. Bubbles do in general induce investment and growth through collateral feedback loops, yet they also create significant costs when they burst. When a bubble bursts feedback loops amplify the effects on the real economy. One channel is the excessively volatile risk premium that has to be paid. Another channel is the fluctuation in housing liquidity due to a change in the average time-to-sell margin. When everybody wants to sell their house, there is a supply side overhang and the liquidity of houses decreases strongly. This leads to a decrease in the value of houses.

Policy applications

As volatility of risk and house prices is high and its economic costs are large, the question arises whether policy can smooth this cycle and increase welfare. Two papers discussed different policy measures.

First, is macroprudential policy useful as an aggregate policy tool or should it take regional heterogeneity into account? A model-based analysis shows that taking the regional heterogeneity of house prices into account has potential benefits over classical monetary policy targeting inflation and one-size-fits-it-all macroprudential policy.

The second paper asked whether monetary policy effectiveness changes depending on the leverage cycle. The authors show that monetary policy is very effective when households deleverage, and credit constraints are binding, while it has only small effects when household leverage is increasing.

A third paper took a completely different angle on housing and studied the effect of the recent refugee inflow on rents in Germany. The authors find, very surprisingly, that local rents decrease as refugees move in. A possible explanation is the crowding out of the original population to different places in response to the inflow of refugees in their neighborhood.

Growth and wealth distribution

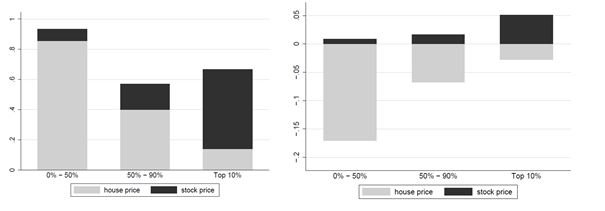

Some presentations at the workshop studied the relevance of the portfolio composition and house prices on the dynamics of wealth inequality. As the bottom 90 percent of the U.S. wealth distribution have a very large housing portfolio share, and hold only a small fraction of equity, it is paramount to wealth distribution how the two assets develop relatively to each other. Moritz Kuhn emphasized that the evolution of wealth inequality is the result of a race between housing and equity performance (see figure 2). When housing does relatively better, wealth inequality decreases. When equity does relatively better, wealth inequality increases.

Figure 2.

Note: The left figure indicates the wealth growth of different groups of the wealth distribution in the U.S. separated for housing and equity between 1998 and 2007. The right figure shows the impact on wealth growth from 2008 to 2016.

The significance of this statement has further been shown by a presentation on wealth inequality in Spain. There, wealth inequality did not increased significantly as rich households held a relatively high share of housing in their portfolio. Moritz Kuhn further emphasized the importance of data on the joint distribution of income and wealth for better understanding the dynamics of income and wealth inequality.

Takeaways from the workshop

Housing and Macroeconomics is an increasingly important topic. And as the many high-quality presentations have showed, young economists are aware of the importance of this topic. Housing has both short and long-run effects on the macroeconomy and the two dimensions might be connected. The financialization of housing drives both the business cycle and long-run wealth inequality. Therefore, housing is an important determinant for welfare and the economy in general.

Note: Photo on the left: Alberto Martin, center photo: participants at the workshop, right photo: Moritz Kuhn.

Global Housing Watch Newsletter: October 2018

*Below is a summary of a workshop prepared by Benjamin Larin (Leipzig University), Hans Torben Löfflad (Leipzig University), Konstantin Gantert (Leipzig University).

What drives house price fluctuations? How do fluctuations in house prices and credit affect the real economy?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, October 12, 2018

Housing View – October 12, 2018

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap. Here’s How. – Zillow

- Homeless in US: A deepening crisis on the streets of America – BBC

- Low mortgage rates and securitization: A distinct perspective on the U.S. housing boom – Brunel University of London

- Housing Sentiment Dips Slightly on Interest Rate Concerns – Fannie Mae

- 2018 Cost Burden Report: Despite improvements, affordability issues are immense – Apartment List

On other countries:

- [China] Angry Mobs Show All’s Not Well in China’s Property Sector – Bloomberg

- [Hong Kong] An Early Warning Sign for the World’s Priciest Homes Is Flashing Sell – Bloomberg

- [United Kingdom] What determines UK housing equity withdrawal in later life? – Regional Science and Urban Economics

Photo by Aliis Sinisalu

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, October 9, 2018

Georgia: Residential Property Price Index

From the IMF’s latest report on Georgia:

“The compilation of an RPPI will facilitate the assessment of developments and risks in property markets. It will therefore be useful for monetary policy as it will improve the understanding of the linkages between property asset prices and financial assets. The National Bank of Georgia compiles a rudimentary index that tracks residential and commercial property prices in two districts of Tbilisi—one is known for expensive properties and the other for modestly priced properties. The index is therefore quite limited and is not disseminated.

On the RPPI, the mission proposed that, as a start, the index be restricted to the capital city and cover all transactions in new apartments and houses. Initially, the index will not include transactions in existing dwellings because of the complexity in covering these dwellings. Existing dwellings may be covered at a later stage when the RPPI methodology is stabilized and the staff gain the experience and skills in compiling the index.

Geostat should be able to compile the RPPI on a quarterly basis and disseminate the first index for the first quarter of 2021, in mid-May 2021. The RPPI will be developed by the same staff compiling the CPI; however, the production schedule for the RPPI can be arranged around the production and release schedule for the CPI to accommodate the available staff

resources. Based on the current CPI production schedule and the proposed RPPI development plan, additional staff would not be required.The most suitable data source for the RPPI may be the National Agency of Public Registry of Ministry of Justice (NAPR). Geostat informed the mission that it is compulsory to

register all transactions in dwellings with the NAPR. Therefore, the NAPR may collect information on transaction value, transactors, dwelling specifications, and location. An alternative source would be the two main websites for real estate transactions.”

From the IMF’s latest report on Georgia:

“The compilation of an RPPI will facilitate the assessment of developments and risks in property markets. It will therefore be useful for monetary policy as it will improve the understanding of the linkages between property asset prices and financial assets. The National Bank of Georgia compiles a rudimentary index that tracks residential and commercial property prices in two districts of Tbilisi—one is known for expensive properties and the other for modestly priced properties.

Posted by at 1:37 PM

Labels: Global Housing Watch

Friday, October 5, 2018

Housing View – October 5, 2018

On cross-country:

- World’s top 10 most at-risk housing markets – Global Property Guide

- The Cities Around the World Most at Risk of Property Bubbles – Bloomberg

- Housing Crises – Federal Reserve Bank of St. Louis

- Global Residential Cities Index – Q2 2018 – Knight Frank

On the US:

- Brief Thoughts on Housing Supply and Policy – MIT Center for Real Estate

- ‘The Renters Strike Back’ – Brookings

- Unlocking Amenities: Estimating Public-Good Complementarity – NBER

- An Examination of the Link between Urban Planning Policies and the High Cost of Housing and Labor – Institute for International Economic Policy

- Housing Stability and Family Health: Five Things to Know – Federal Reserve Bank of San Francisco

- Housing Market Slows, as Rising Prices Outpace Wages – New York Times

- The Hot Property That’s Next on Tech’s Agenda: Real Estate – New York Times

- Dallas strikes it rich with rising property prices – Financial Times

- Mortgage Market Design: Lessons from the Great Recession – Brookings

- How vacation homes went from private escape to investment opportunities – Curbed

- America’s Affordable Housing Crisis Isn’t Just Hitting Cities – Huffington Post

- How Will Artificial Intelligence Shape Mortgage Lending? – Fannie Mae

On other countries:

- [Canada] British Columbia Cracks Down on Dirty Money in Real Estate – Bloomberg

- [Denmark] Housing Summit: Future Housing Market and Urban Development in the Capital Region of Denmark – Copenhagen Economics

- [Germany] A look into German housing markets: A bubble call? – Sage Journal

- [Ireland] Thousands march on Irish parliament in growing housing shortage protest – Reuters

- [Italy] House prices in local markets in Italy: dynamics, levels and the role of urban agglomerations – Bank of Italy

- [Mexico] Empty houses across North America: Housing finance and Mexico’s vacancy crisis – Urban Studies

- [Spain] Organisations and political groups reach an agreement to allocate 30% of all new homes as protected housing – Info Barcelona

- [Thailand] Thailand to Impose Mortgage Curbs to Tackle Speculation – Bloomberg

- [United Kingdom] What a no-deal Brexit could mean for London property prices – Global Property Guide

- [United Kingdom] London stamp duty take hits record £4.9bn even as sales fall – Financial Times

- [United Kingdom] May Plans to Hike U.K. Property Tax for Foreign Buyers – Bloomberg

- [United Kingdom] New tax on foreign home buyers to help rough sleepers, PM says – BBC

- [United Kingdom] Social Housing: Evidence Review – University of York

Photo by Aliis Sinisalu

On cross-country:

- World’s top 10 most at-risk housing markets – Global Property Guide

- The Cities Around the World Most at Risk of Property Bubbles – Bloomberg

- Housing Crises – Federal Reserve Bank of St. Louis

- Global Residential Cities Index – Q2 2018 – Knight Frank

On the US:

- Brief Thoughts on Housing Supply and Policy – MIT Center for Real Estate

- ‘The Renters Strike Back’ – Brookings

- Unlocking Amenities: Estimating Public-Good Complementarity – NBER

- An Examination of the Link between Urban Planning Policies and the High Cost of Housing and Labor – Institute for International Economic Policy

- Housing Stability and Family Health: Five Things to Know – Federal Reserve Bank of San Francisco

- Housing Market Slows,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts