Showing posts with label Global Housing Watch. Show all posts

Friday, January 25, 2019

Housing Market in Hong Kong

The IMF’s latest report on Hong Kong says:

“The three-pronged strategy, comprised of macroprudential measures, stamp duties, and measures to boost housing supply, remains appropriate and should continue in place, and be adjusted as financial stability risks evolve. However, ultimately resolving the imbalances in the housing market requires expanding supply and further efforts are needed in this area.”

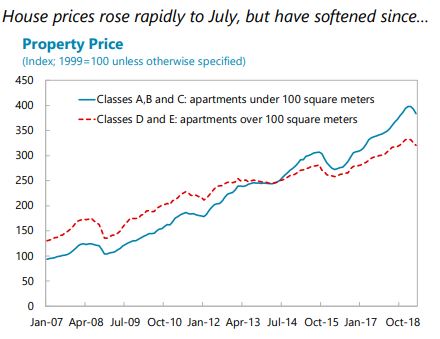

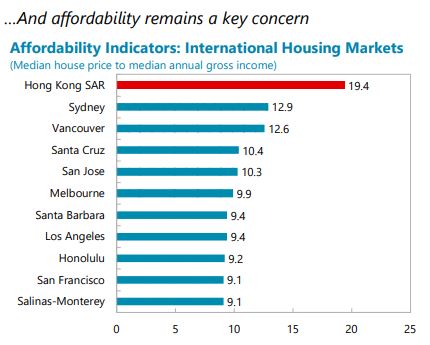

“The authorities’ strategy to contain the housing boom using tight macroprudential measures and stamp duties remains appropriate, but more needs to be done to raise housing supply. The authorities’ three-pronged approach relies on a mix of macroprudential policies, stamp duties to contain excessive demand, and measures to increase housing supply. While macroprudential measures have allowed for building buffers in the financial system against a correction, housing prices rose until recently, and affordability deteriorated. A significant increase in housing supply remains the most needed course of action. Given affordability concerns, the authorities could also consider increasing spending on public housing and allocating a larger share of new housing stock for public housing.

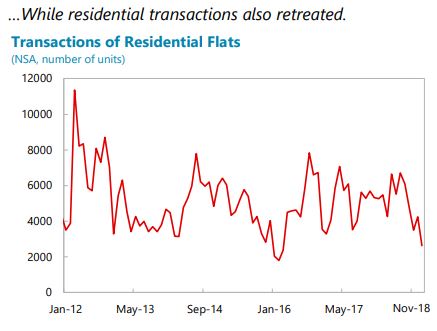

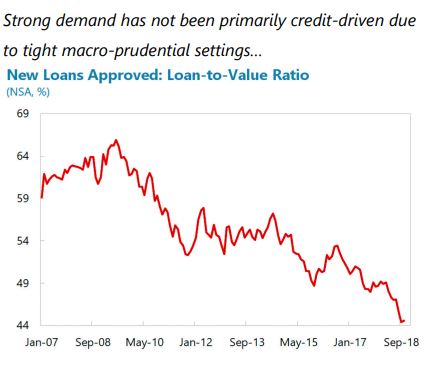

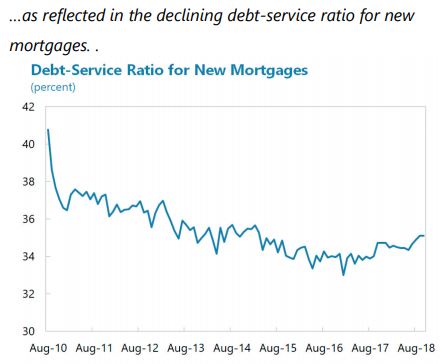

Tight macroprudential regulations have helped contain systemic risks and should remain in place. These include: LTV and debt service-toincome (DSR) ratios that vary with the residence type (primary vs. other) and the source of borrower’s income (originating in vs. outside of Hong Kong SAR); stress tests on the DSR to ensure affordability if interest rates increase; and floors on risk weights on property loans.6 These measures, together with stringent regulation and supervision, allowed banks to build significant buffers that should help cushion the impact of house price declines. While the mix should be reassessed on a regular basis, the authorities should cautiously await more signs of a sustained decline before considering loosening macroprudential and demand-side measures. At the same time, if prices rebound, further tightening of macroprudential measures would likely result in leakages to unregulated non-bank financial institutions as borrowers secure mortgage financing outside regular bank channels (e.g., property developers offering financing to potential buyers).

Stamp duties on real estate have helped contain systemic risks and should be retained for now but phased out when these risks dissipate.

- The government maintains three types of stamp duties on purchase of residential properties: Ad Valorem Stamp Duty on all purchases except of primary residences of permanent residents who do not have any other local residential property at the time of purchase (called previously Doubled Ad Valorem Stamp Duty/currently New Residential Stamp Duty), Special Stamp Duty (SSD) on resale of residential properties within 36 months, and Buyer’s Stamp Duty (BSD) on purchases by non-residents.7 Staff analysis indicates that stamp duties have been effective in curbing house price increases by as much as 9 percent, and, consequently, helped limit household indebtedness and the buildup of systemic risks in the banking sector.

- The DSD/NRSD is levied at a higher rate on non-residents and is assessed to be a capital flow management measure and macroprudential measure under the IMF’s Institutional View of Capital Flows. It continues to be assessed as appropriate given that it: i) was imposed to stem the inflow of capital into the property market; ii) was not used to substitute for the appropriate macroeconomic adjustment; and iii) was imposed because macroprudential measures did not apply to cash buyers, and their further tightening could have resulted in leakages to less regulated non-bank financial institutions. Moreover, the systemic financial risk remains elevated. Stamp duties should be phased out once systemic risks dissipate.

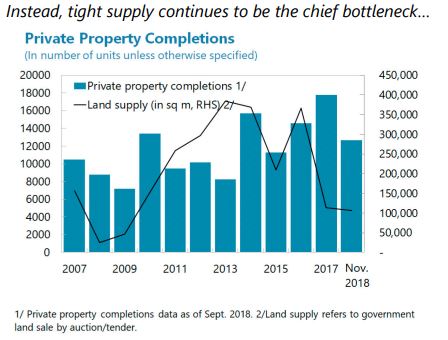

Efforts to further increase supply will be key to resolving the demand-supply imbalance and moderating further price increases.

- After a significant increase in the number of housing units in the early 2000s, the average annual housing production between 2006-2013 fell below 25,000 units. In 2014 the authorities adopted the Long-Term Housing Strategy, which aimed to provide 460,000 housing units over ten years. This was complemented by the Hong Kong 2030+ Strategy—a guide to long-term planning and development of land and infrastructure. While housing production has increased to around 30,000 units on average over 2015-17, it has been falling short of target by around 40 percent on average.

- The authorities are implementing new measures to boost housing supply. In April 2018, the Task Force on Land Supply presented options to increase the availability of land for residential housing, including reclaiming land in Victoria Harbor, and potential development of two strategic areas in East Lantau Metropolis and New Territories North. The “Lantau Tomorrow” reclamation project, as well as further development of brownfield sites, land sharing, and revitalization of existing buildings have been proposed in the 2018 Policy Address. Furthermore, the authorities announced plans to reform the pricing of subsidized housing, initiate a starter homes project, and set up a task force to assist with provision of transitional housing. In addition, a vacant property tax (“Special Rates” tax) of 200 percent of a flat’s “ratable” value (rental value estimated by the Rating and Valuation Revenue Department, roughly 5 percent of the property value) was proposed for unsold new residential units, and a requirement on developers to offer no less than 20 percent of flats during each sale to prevent the accumulation of unsold flats.

- The authorities should also review and—where possible—expedite the procedures guiding the process of identifying land and building sites, zoning, and conducting the necessary environmental, design, transportation, and other assessments to streamline the process.

Frequent reviews of eligibility for social housing could potentially help alleviate social pressures. Around 30 percent of households currently live in public rental housing, with eligibility based on income and wealth, and additional 15 percent of households live in subsidized sale flats. Wait time for public rental housing have increased significantly, from 1.8 years for general applicants and 1.1 years for the elderly in 2008, to 5.1 years and 2.8 years, respectively, in 2017 to ensure proper allocation of benefits, frequent reviews of eligibility should be conducted: in 2016, around 5½ percent of households in the highest income quantile lived in public rental housing.

The authorities agreed that increasing land and housing supply was fundamental to resolving the housing problem facing the community. Challenges in achieving the ten-year housing supply targets under the Long-Term Housing Strategy remain, tied to insufficient land for development and the necessary time to carry out due procedures. The authorities re-iterated that no efforts are being spared, as evidenced by the Government’s vision for the development of Lantau as outlined in the 2018 Policy Address, which should greatly increase land supply in the long-term. Macro-prudential and demand-side measures in the form of stamp duties have been conducive to a healthy development of the property market and will be maintained at this juncture. The authorities added that they could revisit measures as needed if warranted by changes in conditions. They underscored that the current state of the housing market is very different from that pre-Asian Financial Crisis: LTVs are much lower as are debt service burdens, supply is tighter, and banks, developers and households are much less leveraged now.”

The IMF’s latest report on Hong Kong says:

“The three-pronged strategy, comprised of macroprudential measures, stamp duties, and measures to boost housing supply, remains appropriate and should continue in place, and be adjusted as financial stability risks evolve. However, ultimately resolving the imbalances in the housing market requires expanding supply and further efforts are needed in this area.”

“The authorities’ strategy to contain the housing boom using tight macroprudential measures and stamp duties remains appropriate,

Posted by at 2:11 PM

Labels: Global Housing Watch

Housing View – January 25, 2019

On cross-country:

- 15th Annual Demographia International Housing Affordability Survey – Demographia

- Informal settlements and housing markets – International Growth Centre

- Eurozone house price growth squeezed by weaker Italian market – Financial Times

On the US:

- Microsoft’s Leap Into Housing Illuminates Government’s Retreat – New York Times

- Microsoft’s $500 million plan to fix Seattle’s housing problem, explained – VOX

- Dynamism Diminished: The Role of Housing Markets and Credit Conditions – NBER

- Fears of housing downturn may have been overblown – CNN

- US housing: Hopes for a turnaround? – ING

- The Housing Blues Won’t Be Over Soon – Wall Street Journal

- BofA Says Don’t Believe the Hype on a Housing Collapse – Bloomberg

- Housing Inventory Tracking – Calculated Risk

- Shiller: Trump is a ‘psychological boost’ to the housing market – Yahoo Finance

On other countries:

- [Czech Republic] Czech: Property price growth still outstrips EU average – ING

- [Egypt] Egypt’s house prices falling sharply again – Global Property Guide

- [Netherlands] Record House Prices, Jobs Growth Not Enough to Keep Dutch Happy – Bloomberg

- [Singapore] Singapore’s house price rises accelerating – Global Property Guide

- [Spain] Spanish Existing-Home Prices Jump 7.8% in 2018, Most in a Decade – Bloomberg

- [Switzerland] Slowdown inevitable for house prices in Switzerland – Global Property Guide

- [United Arab Emirates] UAE’s property prices fall further – Global Property Guide

- [United Kingdom] Are UK house prices heading for a post-Brexit meltdown? – Financial Times

- [United Kingdom] Whatever happens, Brexit is bad news for young house buyers – Financial Times

- [United Kingdom] Housing market outlook worst ‘for 20 years’ – BBC

- [United Kingdom] Smaller companies deliver better returns than property – Financial Times

- [United Kingdom] Tata Steel announces vision to combat growing housing crisis – Tata Steel

- [United Kingdom] ‘Brexit discount’ on London property fails to tempt US buyers – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- 15th Annual Demographia International Housing Affordability Survey – Demographia

- Informal settlements and housing markets – International Growth Centre

- Eurozone house price growth squeezed by weaker Italian market – Financial Times

On the US:

- Microsoft’s Leap Into Housing Illuminates Government’s Retreat – New York Times

- Microsoft’s $500 million plan to fix Seattle’s housing problem,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, January 18, 2019

Housing View – January 18, 2019

On cross-country:

- London, New York and Hong Kong Are No Longer Immune to Global Housing Downturn – Bloomberg

- Global Housing and Mortgage: Outlook 2019 – Fitch Ratings

On the US:

- What if Cities Are No Longer the Land of Opportunity for Low-Skilled Workers? – New York Times

- Recession Signals: Four Housing Indicators to Watch in 2019 – Federal Reserve Bank of St. Louis

- Thousands Face Threat Of Eviction After HUD Contracts Expire Due To Shutdown – NPR

- Your Taxes (Once Again) Are Underwriting Bad Mortgage Loans – Foundation for Economic Education

- Using Data Visualizations to Explain Housing and Mortgages – Barry L. Ritholtz

- Examining Both Sides of the Transaction: Bargaining in the Housing Market – Real Estate Economics

- Real Estate Investors See Riches in a Tax Break Meant to Help the Poor – Bloomberg

- Home Personal Finance Real Estate Buyers are finally finding more discounts on new homes – MarketWatch

- Microsoft Pledges $500 Million for Affordable Housing in Seattle Area – New York Times

- This Year Could Reverse the Slide for Housing and Auto Industries – Bloomberg

- Explaining the U.S. Urban Housing Shortages – Wall Street Journal

- Fed Says Student Debt Has Hurt the U.S. Housing Market – Wall Street Journal

- The Housing Affordability Crisis: The Role of Anti-Sprawl Policy – Cascade Policy Institute

- US real estate: changing the way New York is built – Financial Times

- Expected Gains in Remodeling Spending to Slide Lower in 2019 – Harvard Joint Center for Housing Studies

On other countries:

- [Australia] The Australian Dream Died Alone in an Apartment – Bloomberg

- [Latvia] Latvia’s house price rises decelerating – Global Property Guide

- [Netherlands] Amsterdam Houses Head for Record Prices – Bloomberg

- [Romania] Romania’s housing market is losing steam again – Global Property Guide

- [Spain] Spain’s house prices continue to rise modestly – Global Property Guide

- [Taiwan] Taiwan’s house prices almost steady – Global Property Guide

- [United Kingdom] Why the housing ladder doesn’t exist anymore – Financial Times

On cross-country:

- London, New York and Hong Kong Are No Longer Immune to Global Housing Downturn – Bloomberg

- Global Housing and Mortgage: Outlook 2019 – Fitch Ratings

On the US:

- What if Cities Are No Longer the Land of Opportunity for Low-Skilled Workers? – New York Times

- Recession Signals: Four Housing Indicators to Watch in 2019 – Federal Reserve Bank of St.

Posted by at 6:35 AM

Labels: Global Housing Watch

Wednesday, January 16, 2019

Special Issue: The Appropriate Role of Government in U.S. Mortgage Markets

From the Federal Reserve Bank of New York:

“A decade after the financial crisis, the U.S. mortgage finance system remains largely untouched by legislative reforms. Policy deliberations have focused on Fannie Mae and

Freddie Mac—the two enormous government-sponsored enterprises (GSEs) that were placed into federal conservatorship in September 2008. The conservatorships were initially thought of as a temporary arrangement during which U.S. mortgage markets could be stabilized and function as intended, while providing time for Congress to consider the appropriate long-term federal role in the secondary mortgage market. To date, however, legislators have yet to resolve some basic issues: Should government guarantees continue to be available for a large swath of loans? If so, what types of institutions should have direct access to guarantees and how would their access be facilitated and regulated?This special issue of the Federal Reserve Bank of New York’s Economic Policy Review presents a set of articles that developed from presentations given at “The Workshop on the Appropriate Government Role in U.S. Mortgage Markets,” held at the Bank on April 27-28, 2017. The workshop was organized in association with the Board of Governors, the Federal Reserve Bank of Atlanta, the Anderson School of Management at the University of California–Los Angeles, and the Wharton School of the University of Pennsylvania. We emphasize at the outset that the opinions expressed in the articles are those of the authors and do not necessarily reflect the views of any of the organizing institutions. In this introduction, we provide some context for the workshop and highlight the articles’ key findings.”

Introduction

W. Scott Frame and Joseph TracyGSE Guarantees, Financial Stability, and Home Equity Accumulation

Wayne Passmore and Alexander H. von HafftenThe FHA and the GSEs as Countercyclical Tools in the Mortgage Markets

Wayne Passmore and Shane M. SherlundPricing Government Credit: A New Method for Determining Government Credit Risk Exposure

Brent W. Ambrose and Zhongyi YuanPeas in a Pod? Comparing the U.S. and Danish Mortgage Finance Systems

Jesper Berg, Morten Bækmand Nielsen, and James VickeryCredit Risk Transfer and De Facto GSE Reform

David Finkelstein, Andreas Strzodka, and James VickeryCredit Risk Transfer, Informed Markets, and Securitization

Susan M. WachterHousing Affordability: Recommendations for New Research to Guide Policy

Jane DokkoLong-Term Outcomes of FHA First-Time Homebuyers

Donghoon Lee and Joseph Tracy

From the Federal Reserve Bank of New York:

“A decade after the financial crisis, the U.S. mortgage finance system remains largely untouched by legislative reforms. Policy deliberations have focused on Fannie Mae and

Freddie Mac—the two enormous government-sponsored enterprises (GSEs) that were placed into federal conservatorship in September 2008. The conservatorships were initially thought of as a temporary arrangement during which U.S. mortgage markets could be stabilized and function as intended, while providing time for Congress to consider the appropriate long-term federal role in the secondary mortgage market.

Posted by at 11:21 AM

Labels: Global Housing Watch

Housing Market in Finland

The IMF’s latest report on Finland says:

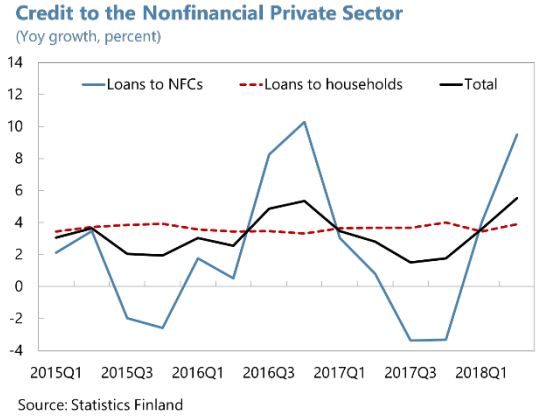

“Credit has expanded moderately overall, but housing corporation loans and consumer credit have been rising more rapidly. Total loan growth to the private nonfinancial sector has remained broadly constant at around 3½ percent for the past five years. Most lending to households has been in the form of secured lending for housing, which has grown around 4 percent. Corporate loan growth has rebounded strongly in the second quarter of the year after a sharp contraction in the second half of 2017. Two lending categories stand out:

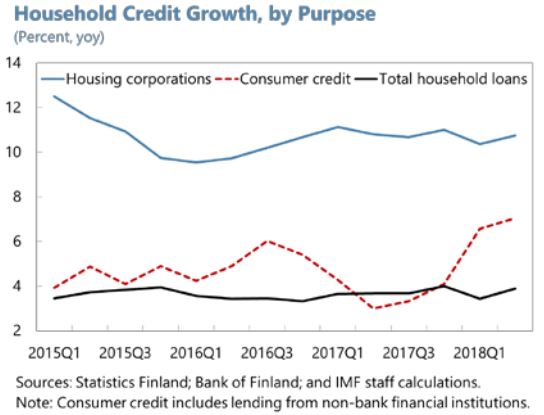

Loans to housing corporations have been expanding rapidly—above 10 percent—for many years. The drivers—expansion of the housing stock and renovation of rental properties—are

healthy. But the shareholders of housing corporations include homeowners, making these de facto indirect loans to households, and households might thereby be tempted to take on more debt than can easily be repaid.Consumer credit has been increasing steadily—above 7 percent y/y in the second quarter of 2018—and now accounts for 12 percent of aggregate household debt, driven by credit

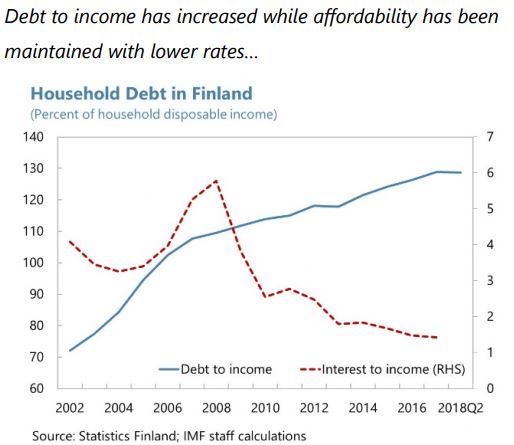

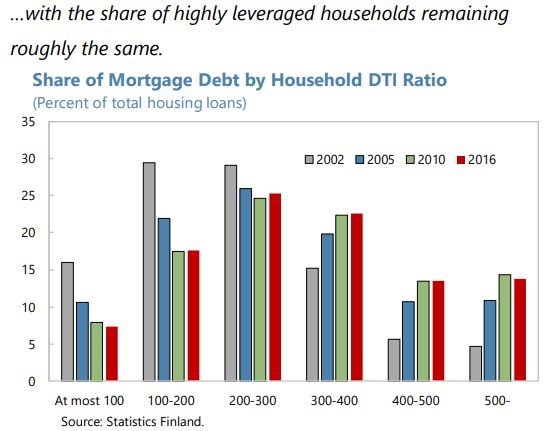

institutions easing lending standards and a rapid increase in non-bank lending. The expansion has been associated with an increase in payment defaults.Household debt has been increasing steadily, despite the increase in real disposable incomes. Saving rates are lower than peers, although some of the difference is attributable to Finland’s public pension system. Household debt remains lower than Nordic peers, but is expected to increase further. Highly-indebted households (i.e. those with debt greater than four times their income) accounted for over a quarter of borrowing in 2016; preliminary survey data for 2017 indicate that the typical new borrower for housing purchases is taking on leverage of 4½ times income. The share of floating rate loans in household lending is high, exacerbating households’ vulnerabilities to interest rate and/or income shocks, although this is mitigated by the prevalence of mortgages with annuity repayments.

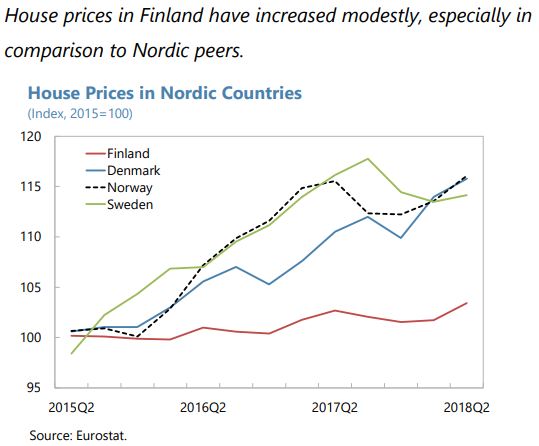

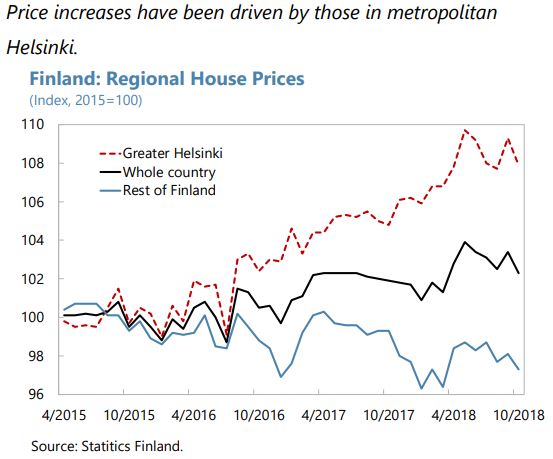

Residential real estate markets do not seem overheated overall, but demand still exceeds supply in major metropolitan areas, and commercial real estate may expose the economy to shocks. Housing starts and completions have been elevated, but price increases in greater Helsinki suggest demand still outstrips supply. Across the whole country, house price increases have been modest, especially in comparison to Nordic peers, with house price deflation in regions outside greater Helsinki. Price-to-income and price-to-rent ratios have not risen much during the recent economic recovery. Low and declining yields in commercial real estate suggest relatively high valuations.

The authorities have tightened credit policies. A floor of 15 percent on the average risk weight for housing loans took effect in January for institutions using internal risk-based (IRB) models. Effective July, the maximum loan-to-collateral (LTC) ratio for housing loans (excluding loans on first homes) was cut from 90 to 85 percent.

The recent tightening is appropriate, but policy could be more effective if the toolkit were modified. Although overall household debt and leverage are not high in comparison with other Nordic countries, there are some cohorts that are increasingly vulnerable to income and/or interest rate shocks—which, in view of the concentration of total lending in real estate, opens the financial system to risks.

The current cap on mortgage loans relative to collateral could usefully be replaced with a cap relative to the value of the property, as is common in other countries. And because the

underlying problem is more the level of debt than housing valuations, it would be useful for the authorities to have debt-based macroprudential tools (such as debt-to-income or debt-service to-income caps) at their disposal should leverage become more stretched. Applying such tools well depends on accurate information. Staff supports the recent Justice Ministry recommendation for the establishment of a “positive credit register”—i.e. a database that credit firms and the FINFSA could use to obtain real-time information about customers’ debt and income levels. A new challenge arises from non-bank lending, including online platforms such as peer-to-peer lending, which is not being recorded in credit statistics and registers.The growing reliance on consumer credit, especially that provided by non-banks and via digital platforms, raises additional concerns. Some of these outlets are not regulated and provide cross border financing. Attempts were made to circumvent legally-binding interest rate caps, raising the question of whether borrowers—especially those dealing with non-bank lenders—are sufficiently informed about the conditions of their loans. The authorities are amending the legislation on interest rate caps to close loopholes. Additional consumer protection measures are needed and require more data collection, especially on consumer lending provided through digital platforms. Tighter prudential requirements to demonstrate creditworthiness could also be considered.

Macroprudential authority tools should not be expected to solve underlying supply problems. The authorities have already implemented measures to expand housing supply in urban areas, including Helsinki. The government provides considerable support for social housing, which should make it easier to move across regions. But property taxation could be deterring mobility: recurrent property taxes collected by municipalities tend to be low, with some exceptions, while transaction tax rates are steeper at 4 percent.”

The IMF’s latest report on Finland says:

“Credit has expanded moderately overall, but housing corporation loans and consumer credit have been rising more rapidly. Total loan growth to the private nonfinancial sector has remained broadly constant at around 3½ percent for the past five years. Most lending to households has been in the form of secured lending for housing, which has grown around 4 percent. Corporate loan growth has rebounded strongly in the second quarter of the year after a sharp contraction in the second half of 2017.

Posted by at 10:56 AM

Labels: Global Housing Watch

Subscribe to: Posts