Showing posts with label Global Housing Watch. Show all posts

Wednesday, February 6, 2019

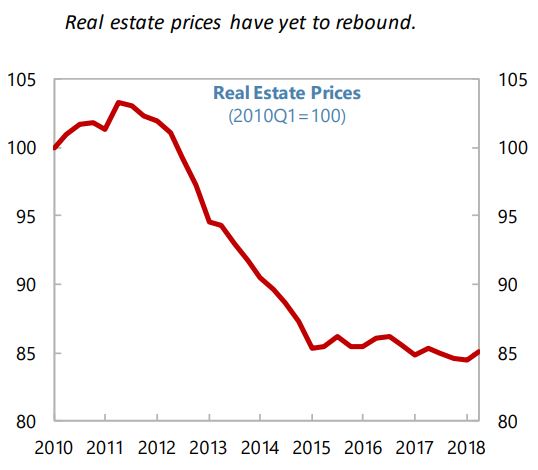

House Prices in Italy

From the IMF’s latest report on Italy:

Posted by at 11:29 AM

Labels: Global Housing Watch

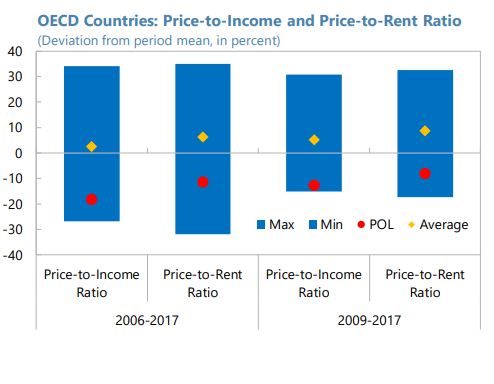

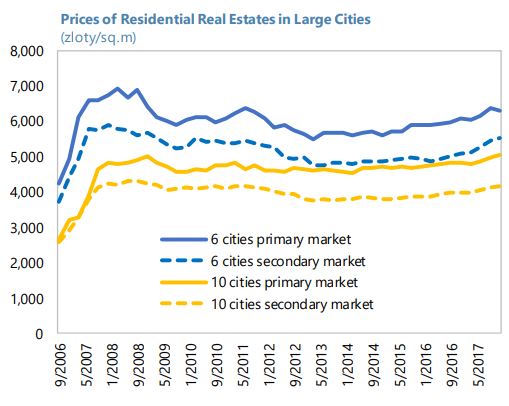

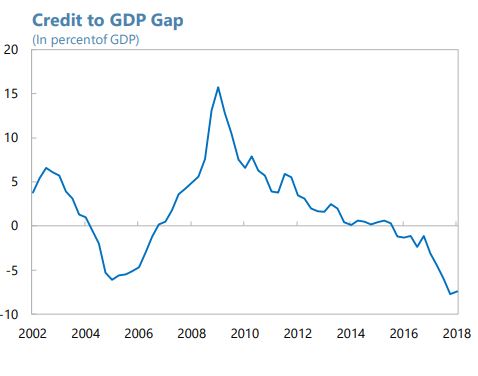

Housing Market in Poland

From the IMF’s latest report on Poland:

“Current strong housing demand is financed to a greater extent than before the GFC with buyers’ own resources. Rising construction costs have slowed the supply of new housing, and nominal house prices in some regions have risen to pre-GFC levels. Nonetheless, affordability remains comfortable owing to strong growth of household incomes.”

From the IMF’s latest report on Poland:

“Current strong housing demand is financed to a greater extent than before the GFC with buyers’ own resources. Rising construction costs have slowed the supply of new housing, and nominal house prices in some regions have risen to pre-GFC levels. Nonetheless, affordability remains comfortable owing to strong growth of household incomes.”

Posted by at 9:29 AM

Labels: Global Housing Watch

Sunday, February 3, 2019

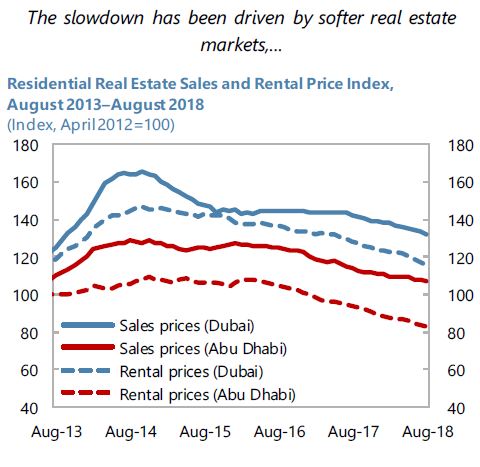

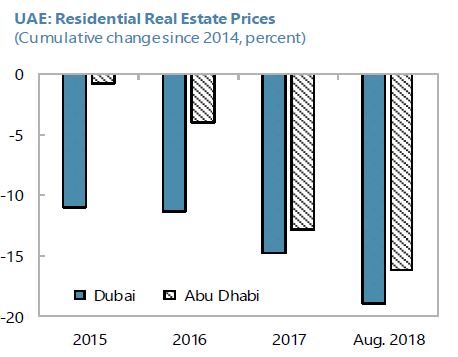

Housing Market in the United Arab Emirates

From the IMF’s latest report on UAE:

“A sharp deepening in the real estate downturn and weakening asset quality could constrain bank lending, which in turn could hold back the recovery.”

“Given the risk of spillovers from declining real estate prices, staff urged the CBU to resist calls for relaxing prudential limits on real estate lending. The authorities are preparing to develop a new bank resolution regime; in the meantime, staff encouraged the CBU to discuss contingency plans for banks in case of an abrupt tightening of financial conditions or other adverse shocks.”

From the IMF’s latest report on UAE:

“A sharp deepening in the real estate downturn and weakening asset quality could constrain bank lending, which in turn could hold back the recovery.”

“Given the risk of spillovers from declining real estate prices, staff urged the CBU to resist calls for relaxing prudential limits on real estate lending. The authorities are preparing to develop a new bank resolution regime; in the meantime,

Posted by at 8:09 AM

Labels: Global Housing Watch

Friday, February 1, 2019

Housing View – February 1, 2019

On cross-country:

- Global Home Price Growth under Pressure – Fitch Ratings

- House Prices to Fall in Several APAC Markets in 2019 – Fitch Ratings

On the US:

- The Dream Revisited – Columbia University Press

- Supply Skepticism: Housing Supply and Affordability – NYU Furman Center

- In Lieu of Gifts, Please Make a Down Payment on Our New Home – Citylab

- Could High-Speed Rail Ease California’s Housing Crisis? See Japan. – Citylab

- More Housing Would Mean Cheaper Housing – Wall Street Journal

- California housing crisis podcast: Where’s the home building for the middle class? – Los Angeles Times

- AEI Housing Market Indicators release on October 2018 data – American Enterprise Institute

- Mortgage Risk Premiums during the Housing Bubble – The Journal of Real Estate Finance and Economics

- Big drop in US homebuilders’ shares could spell trouble – Financial Times

- Americans stopped buying homes in 2018, mortgage lenders are getting crushed, and an economic storm could be brewing – Business Insider

- Two Lawsuits Show What a Hot Mess California Housing Politics Is Right Now – Reason

On other countries:

- [China] Chinese Exiting U.S. Real Estate as Beijing Directs Money Back to Shore Up Economy – Wall Street Journal

- [India] Too slow for the urban march: Litigations and real estate market in Mumbai, India – Brookings

- [Lebanon] Lebanese Central Bank to Reinstate Subsidized Housing Loans – Bloomberg

- [New Zealand] New Zealand Vowed 100,000 New Homes to Ease Crunch. So Far It Has Built 47. – New York Times

- [Singapore] Singapore Is Seeing an Unprecedented Mortgage Slowdown – Bloomberg

- [United Kingdom] What goes up must come down: modelling the mortgage cycle – Bank of England

- [United Kingdom] London property transactions drop to decade low – Financial Times

- [United Kingdom] Call for rethink on UK planning rules for housing – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Global Home Price Growth under Pressure – Fitch Ratings

- House Prices to Fall in Several APAC Markets in 2019 – Fitch Ratings

On the US:

- The Dream Revisited – Columbia University Press

- Supply Skepticism: Housing Supply and Affordability – NYU Furman Center

- In Lieu of Gifts, Please Make a Down Payment on Our New Home – Citylab

- Could High-Speed Rail Ease California’s Housing Crisis?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, January 25, 2019

Ukraine: Residential Property Price Index

The IMF’s latest report on Ukraine:

“A technical assistance (TA) mission was conducted during June 18–22, 2018 to support the State Statistics Service of Ukraine (SSSU) in improving the residential property price indexes (RPPI) for Ukraine. This was the second of a series of SECO2 RPPI-funded TA missions to take place until mid-2019 that will assist in building staff capacity for further development of the RPPI. RPPIs have been identified as critical ingredients for financial stability policy analysis. The indexes are used by policy makers as an input into design of macroprudential policies, that is, those policies aim to reduce systemic risks arising from “excessive” financial procyclicality (such as asset bubbles). RPPIs are also used by policy makers to inform monetary policy and inflation targeting.

In line with the recommendations from the previous mission, and ahead of schedule, an experimental overall national RPPI has been compiled. The authorities have used administrative data on the size of properties registered, combined with a survey covering the construction of new homes, to estimate the relative sizes of primary and secondary markets. The estimated weights remain susceptible to outliers, in particular, errors in the size registered. The SSSU should continue to work on addressing these errors.

It was agreed that a number of other improvements to the existing methodology can be implemented. Within the current methodology, the stratification design will be modified, with construction material to be dropped, significantly reducing the number of strata with zero or few returns each quarter. A standardized procedure for imputation where there are no returns in a stratum will be introduced. This is in addition to the existing procedures, where survey returns are reviewed to identify outliers that could affect results.

To further improve the RPPIs in the medium term, the underlying methodology will switch from stratification to hedonic methods. As a result of discussions during the mission, it was agreed that, given the constraints of the existing survey, hedonic methods represent the best option for reliable RPPIs, particularly, if data sources are improved in the future. The authorities remain enthusiastic about switching from the current stratification method to a hedonic regression method, and, therefore, building staff capacity in this area is a priority. Intensive training on the hedonic method and its relation to the existing methods was provided to the authorities during the mission. Additionally, three staff members will participate in the RPPI training seminar to be held at the Joint Vienna Institute (JVI) during August 2018. Work on developing an experimental hedonic model will be undertaken in 2019.

A switch to comprehensive administrative data will require cooperation of stakeholders elsewhere in the policy system. Existing survey data underpinning the RPPIs are limited, as responses are not legally mandatory. In line with best practice elsewhere, the use of survey data should be replaced by comprehensive administrative data. However, while the authorities can now access information in the registry of property transactions maintained by the State Enterprise Information Center (SEIC), entry of transaction price is not required in the registry, and often the recorded price is the assessed value, rather than the market price. If administrative data are to be used, this will require cooperation of other stakeholders, including the Ministry of Justice (the SEIC’s parent department), so that information recorded in the registry is suitable for use in the compilation of RPPIs.”

The IMF’s latest report on Ukraine:

“A technical assistance (TA) mission was conducted during June 18–22, 2018 to support the State Statistics Service of Ukraine (SSSU) in improving the residential property price indexes (RPPI) for Ukraine. This was the second of a series of SECO2 RPPI-funded TA missions to take place until mid-2019 that will assist in building staff capacity for further development of the RPPI. RPPIs have been identified as critical ingredients for financial stability policy analysis.

Posted by at 2:15 PM

Labels: Global Housing Watch

Subscribe to: Posts