Showing posts with label Global Housing Watch. Show all posts

Tuesday, March 12, 2019

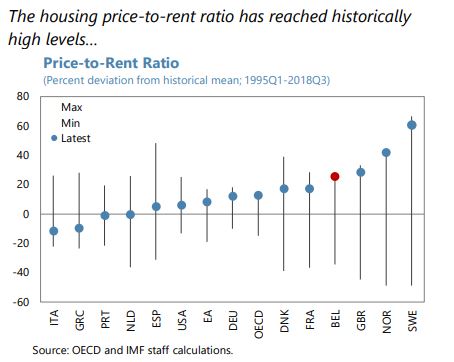

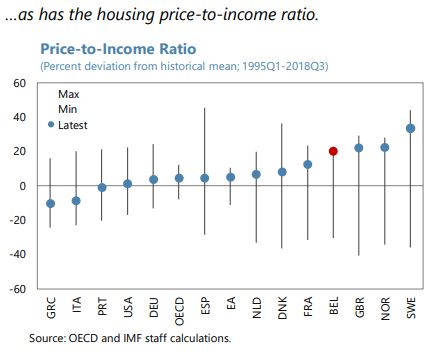

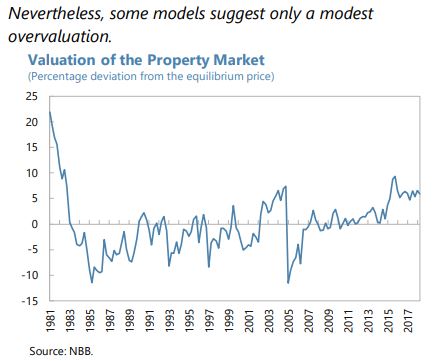

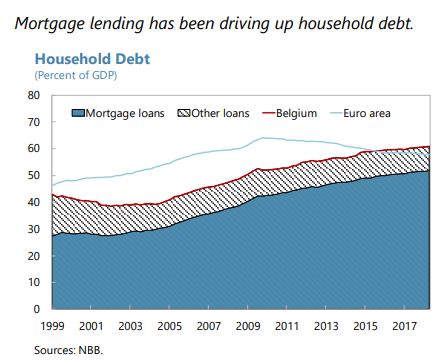

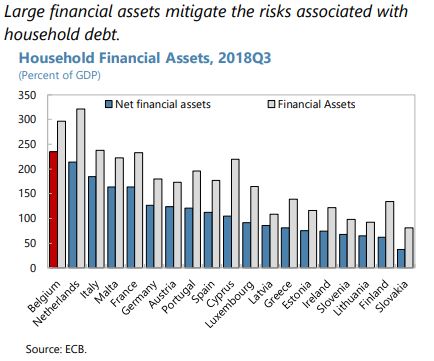

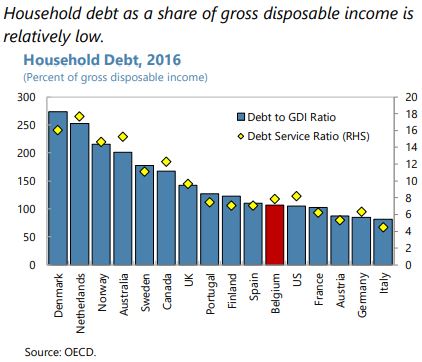

Housing Market in Belgium

From the IMF’s latest report on Belgium:

“Private sector indebtedness, primarily associated with household debt, and sustained increases in housing prices pose additional challenges. Strong growth in mortgage lending (9 percent in 2018) has contributed to a sizeable increase in household debt and housing prices. Models, however, point to only a modest house price overvaluation, depending on location. Meanwhile, the share of loans with a loan-to-value (LTV) ratio below 80 percent has declined by about 10 percentage points during 2014–2017. Although default rates are currently low, households have substantial assets in the aggregate, and household debt-to income is in line with peers, a sharp housing (and asset) price correction could result in rising defaults for some groups of the population and affect banks’ solvency, with second round effects on investment, consumption, and growth. 12 Belgian unconsolidated corporate debt has also increased over the last few years to a relatively high level, although, the level is more in line with peers after accounting for intragroup loans. Nonetheless, its dynamics warrant close monitoring, given recent strong bank credit growth to the corporate sector (…).

Staff welcomed the authorities’ recent macroprudential measures to address risks in the housing market and encouraged the authorities to remain proactive. To guard against a correction in housing prices and discourage banks from taking excessive credit risk, the National Bank of Belgium (NBB) introduced in May 2018 an add-on to risk weights on bank mortgage exposures as a new macroprudential measure. In view of the robust overall level of credit growth (5.9 percent in 2018) and credit gap (the NBB estimates this at 2 percent at end Q3-2018), staff recommended that the NBB continue to closely monitor the build-up of cyclical risks in both the household and corporate sectors and stand ready to tighten macroprudential policy further, including through the use of a countercyclical capital buffer. The authorities could also consider revising the framework for macroprudential decision-making to ensure the ability to deploy a broader range of macroprudential policies in a timely manner, as recommended by the 2017 Financial Sector Assessment Program (FSAP) mission.”

From the IMF’s latest report on Belgium:

“Private sector indebtedness, primarily associated with household debt, and sustained increases in housing prices pose additional challenges. Strong growth in mortgage lending (9 percent in 2018) has contributed to a sizeable increase in household debt and housing prices. Models, however, point to only a modest house price overvaluation, depending on location. Meanwhile, the share of loans with a loan-to-value (LTV) ratio below 80 percent has declined by about 10 percentage points during 2014–2017.

Posted by at 9:26 AM

Labels: Global Housing Watch

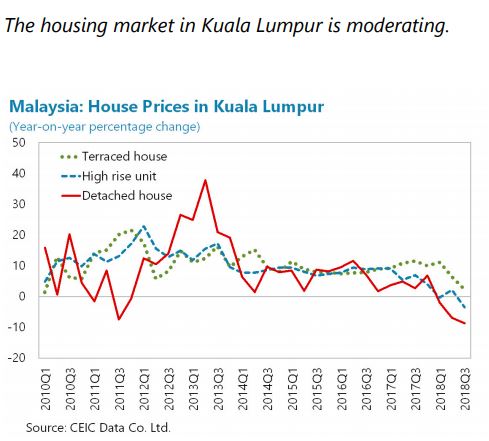

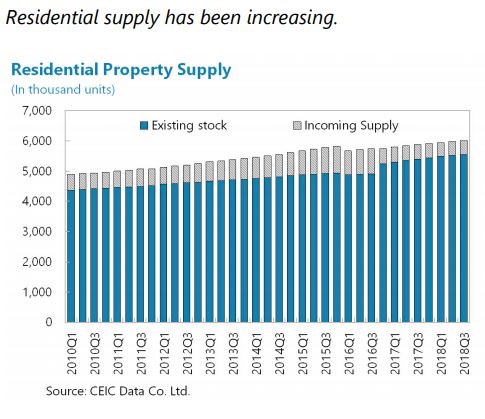

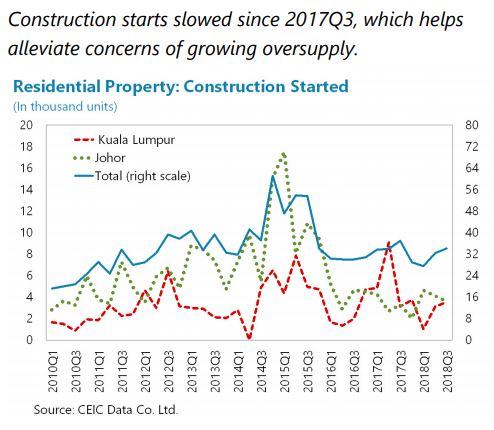

Housing Market in Malaysia

From the IMF’s latest report on Malaysia:

“The authorities continue to closely monitor risks emanating from the housing market, although the risks are deemed manageable (…). House price growth has declined from 6.5 percent in 2017 to 3 percent in 2018H1, and the volume of transactions has also declined. The number of unsold housing units that have been completed or are currently under construction is increasing and is mostly concentrated in high-rise buildings. Banks’ direct exposure to developers remain small and is closely monitored by the BNM. According to BNM stress tests, potential bank losses originating from a possible sharp real estate price adjustment and shocks to income and interest rates are small relative to the banks’ capital buffers. The BNM, MOF, and Ministry of Housing and Local Government have introduced new measures that help reduce the cost of property or of contracting a mortgage loan, with the objective to strengthen the demand for housing and facilitate leasing, and therefore gradually reduce the supply overhang. The impact of these measures should be evaluated on an ongoing basis to ensure effectiveness and correct potential distortions.

As systemic risks from the housing market dissipate, the residency-based differentiation in the real estate measures introduced in 2014 should be gradually phased out. Given banks’ sizable exposure to mortgage lending and to the construction industry, a real estate market price correction, through a reduction in household and corporate wealth, and these agents’ debt servicing capacity, could have a significant impact on growth and financial stability as NPLs rise. During 2012–13, the Malaysian House Price Index (MHPI) grew by a cumulative 24 percent, well-above its long-run annual average of 6 percent and, in 2014, amid further significant price increases, the number of transactions by non-citizens surged by 30 percent (…). The measures introduced in 2014 helped cool down the market (cutting growth in property purchases by non-citizens by over 50 percent in 2015 and by another 38.9 percent in 2016, and slowing the growth rate of MHPI to 9.4 and 7.4 percent in 2014 and 2015, respectively), avoid significant price adjustments, and reduce the rate of future debt build-up, thus reducing the probability of systemic distress. In the absence of a capital inflow surge for the time-being, but still high household leverage, gradually removing the residency-based differentiation in both measures is recommended as systemic risk dissipates. Carefully calibrated changes to the measures could have the additional benefits of helping to reduce the excess supply of high-end housing where nonresident buyers are concentrated and thereby the probability of a sharp downward price correction. Should the activity in certain segments again threaten financial stability, the authorities may consider macroprudential measures that target the specific segments, without a differentiated treatment of non-residents.”

From the IMF’s latest report on Malaysia:

“The authorities continue to closely monitor risks emanating from the housing market, although the risks are deemed manageable (…). House price growth has declined from 6.5 percent in 2017 to 3 percent in 2018H1, and the volume of transactions has also declined. The number of unsold housing units that have been completed or are currently under construction is increasing and is mostly concentrated in high-rise buildings.

Posted by at 9:20 AM

Labels: Global Housing Watch

Friday, March 8, 2019

Housing View – March 8, 2019

On the US:

- Oregon’s new rent control law is only a band-aid on the state’s housing woes – Brookings

- Trickle-down housing economics – Northwestern University

- Slicing New York’s Housing Pie – New York Times

- Lens, Manville Shape Discussion of How Housing Can Be Coupled to Transit – Citylab

- Protect First Time Buyers and Taxpayers. Let the “Patch” Expire – American Enterprise Institute

- Boston Wants to Flip More Market-Rate Apartments into Affordable Housing – Next City

- Real Time Economics: More Americans Are Buying a Home Again – Wall Street Journal

- Climate change is hurting coastal real estate values. Oh, we’re losing ocean fish, too –Los Angeles Times

- Ask the Economist with Skylar Olsen – DSNews

- The Affordable Housing Crisis Across The U.S.: ‘Where We Call Home,’ Part 1 – wbur

- Oregon, the Rent Control State – Wall Street Journal

- Housing Affordability for Renters Index: Local Perspective and Migration – Urban Institute

- Three differences between black and white homeownership that add to the housing wealth gap – Urban Institute

- Housing Finance At A Glance: A Monthly Chartbook, February 2019 – Urban Institute

- How student debt may foster homeownership – University of Chicago

- Cheaper Housing Options Boost Homeownership in Some U.S. Metros – Bloomberg

- Redfin: These housing markets give low-income families a better shot at the American Dream – HousingWire

On other countries:

- [Australia] The Housing Market and the Economy – Reserve Bank of Australia

- [Australia] Australian House Prices Provide Food for Doves and Hawks – Bloomberg

- [Australia] Here Are the Winners From Australia’s Property-Market Downturn – Bloomberg

- [China] Chinese Banks Will Rise or Fall With the Property Market – Wall Street Journal

- [Luxembourg] No end in sight for upward housing market spiral in Luxembourg – Financial Times

- [Netherlands] As Amsterdam Overheats, Investors See Rent Cap Scaring off Money – Bloomberg

- [Portugal] Portugal’s housing market is strengthening – Global Property Guide

- [Thailand] Thailand’s modest house price rises – Global Property Guide

- [United Kingdom] Some of Britain’s wealthiest areas hit by house price drops of up to 25 percent – Global Property Guide

On the US:

- Oregon’s new rent control law is only a band-aid on the state’s housing woes – Brookings

- Trickle-down housing economics – Northwestern University

- Slicing New York’s Housing Pie – New York Times

- Lens, Manville Shape Discussion of How Housing Can Be Coupled to Transit – Citylab

- Protect First Time Buyers and Taxpayers. Let the “Patch” Expire – American Enterprise Institute

- Boston Wants to Flip More Market-Rate Apartments into Affordable Housing – Next City

- Real Time Economics: More Americans Are Buying a Home Again – Wall Street Journal

- Climate change is hurting coastal real estate values.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, March 1, 2019

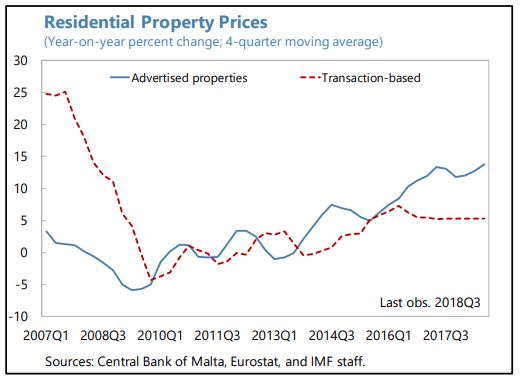

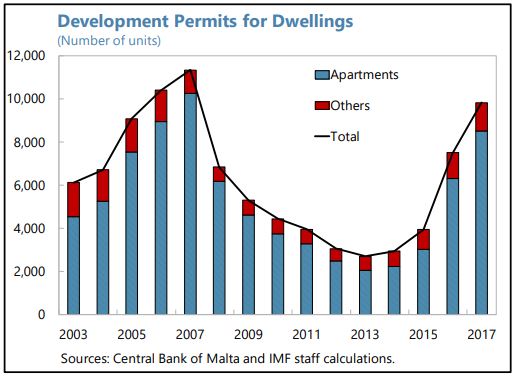

Housing Market in Malta

From the IMF’s latest report on Malta:

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge, recent house price trends can largely be explained by fundamentals such as e.g., strong immigration flows, rising disposable income, portfolio rebalancing towards property investment and a delayed supply response. Other factors such as the extension of the first-time home-buyer stamp duty relief, the reduced tax rate on rental income, surging demand for tourist accommodation and, for the high-end segment, the IIP may also have played a role (but are not directly controlled for in the empirical analysis conducted in Annex I).

Banks’ exposure to housing-market-related risks is high and increasing, and the introduction of macroprudential measures should proceed as planned. All the more so that households’ indebtedness is relatively high, low income households are vulnerable to housing price corrections and flexible interest rate on mortgages are prevalent.7 Against this backdrop, recent efforts to close data gaps (loan-level data collection) and the planned introduction of borrowerbased macroprudential measures such as caps to loan-to-value (LTV) ratios at origin, stressed debt service-to-income (DSTI) limits, and amortization requirements are steps in the right direction (see text table).

To be more effective, the new borrower-based measures could be refined in due course and exemptions to the LTV limit could be narrowed. To avoid excessive risk concentration, speed limits should be defined in terms of the total value of new loans, not in terms of the number of new loans, and speed limits for loans against secondary and buy-to-let properties, the likely most speculative segment, should be lowered as soon as concerns about any initial disruptions dissipate. Finally, the scope of the new borrower-based measures should be extended to also cover non-bank mortgage loans.

Rapidly rising housing costs are affecting vulnerable households. The government recently relaxed the eligibility requirements for rent subsidies, but the scheme should be periodically reviewed to ensure it remains targeted on low-income households. Further efforts should also be envisaged to accelerate the provision of social housing, including by fiscally incentivizing private investments.

Authorities’ Views

Rapidly rising property prices are viewed by the authorities as mainly reflecting economic fundamentals. Inflows of foreign labor and higher income in general are fueling housing demand. The authorities also see the impact of tax benefits for first and second-time home buyers, the reduced tax rate on rental income and the IIP as marginal. They stressed that the planned borrower-based macroprudential measures were carefully calibrated to have minimal market impact upon their introduction. The authorities have agreed that there is room for refinement, in due course, and emphasized that they can easily recalibrate the measures to mitigate financial stability risks emanating from the housing market in a timely and effective manner. The authorities also recognize the growing importance of making housing more affordable for vulnerable households. They emphasized the progressive nature of the new rent subsidy scheme. Projects are underway to increase the stock of social and affordable housing.”

From the IMF’s latest report on Malta:

“Rapidly rising house prices and rents may eventually pose financial stability risks while putting some vulnerable households at risk of poverty. Policies that help mitigate the rapid increase of house prices and make rents more affordable while strengthening households and banks’ balance sheets should be encouraged.

Strong demand for housing has continued to push up property prices. While some signs of overvaluation have started to emerge,

Posted by at 10:52 AM

Labels: Global Housing Watch

Housing View – March 1, 2019

On cross-country:

- Social rental intermediation. How private landlords can contribute to solve the housing crisis? – Housing Europe

- What are some of the primary driving forces behind the Urban Housing Crunch? – Forbes

- What if the future of housing means accepting that a home isn’t permanent? – Quartz

- Macroprudential approaches to non-performing loans – ESRB

On the US:

- How Monetary Policy Shaped the Housing Boom – New York University

- Inside the Rise and Fall of a Multimillion-Dollar Airbnb Scheme – New York Times

- Rents Are Up? That Depends on Where You Live – New York Times

- California housing crisis podcast: Will a boom in building make housing more affordable? – Los Angeles Times

- UCLA Ziman Program – a First Nationwide – Teaches Affordable Housing Development – UCLA

- U.S. housing outlook stuck in a lull as economy dulls: Reuters poll – Reuters

- Home Prices in 20 U.S. Cities Rise by Least in Four Years – Bloomberg

- Real House Prices and Price-to-Rent Ratio in December – Calculated Risk

- Trouble In The Housing Market – Forbes

- Slowing Home Price Growth and Construction Hit Housing Market – Wall Street Journal

- Is Housing in Your City Getting Unaffordable? Here’s How You Can Help – Citylab

- Can housing reform survive a hall of mirrors? – Boston Globe

- Seattle-area home price cooldown not reaching cheaper parts of housing market – Seattle Times

- California’s housing supply law fails to spur enough construction, study says – Los Angeles Times

On other countries:

- [Australia] Australian Home Lending Now Weakest Since the Mid-1980s – Bloomberg

- [Australia] House price falls in Sydney and Melbourne not all bad, Reserve Bank head says – The Guardian

- [Australia] Australia’s housing data still terrible across the board – Variant Perception

- [Canada] Affordable housing becomes singular focus of Toronto’s new real estate czar – Globe and Mail

- [Canada] Bank of Canada says housing crunch threatens Canadian economy – Fraser Institute

- [Canada] Canada’s housing market set for years of subdued price rises: Reuters poll – Reuters

- [Canada] Another budget, another missed opportunity to tackle B.C.’s housing shortage – Fraser Institute

- [China] Capital Gains Tax would see house prices fall as investors flee market ahead of tax’s implementation – REINZ – New Zealand Herald

- [China] China’s Huge Number of Vacant Apartments Are Causing a Problem – Citylab

- [Denmark] Danish Study Quantifies Impact of House Prices on Consumption – Bloomberg

- [Hong Kong] Why Hong Kong Is Claiming Golf Greens for New Housing – Citylab

- [India] India Cuts Tax on Housing to Boost Real Estate Before Elections – Bloomberg

- [Ireland] Ireland’s house price rises continue, albeit at a much slower pace – Global Property Guide

- [Israel] Changes in the share of first home buyers among young people, based on income level – Bank of Israel

- [Netherlands] House prices expected to keep rising this year, homeownership unattainable for more and more people – Rabobank

- [New Zealand] New Zealand Locks the Doors From the Inside – New York Times

- [New Zealand] Sale of portable cabins booms in New Zealand amid housing crisis – The Guardian

- [Sweden] Refugees and apartment prices: A case study to investigate the attitudes of home buyers – Regional Science and Urban Economics

- [United Kingdom] No-deal Brexit would take a chip off UK home values – Reuters poll – Reuters

- [United Kingdom] Housing costs: Five surprises explained – BBC

- [United Kingdom] A solution to the housing crisis? – Financial Times

On cross-country:

- Social rental intermediation. How private landlords can contribute to solve the housing crisis? – Housing Europe

- What are some of the primary driving forces behind the Urban Housing Crunch? – Forbes

- What if the future of housing means accepting that a home isn’t permanent? – Quartz

- Macroprudential approaches to non-performing loans – ESRB

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts