Tuesday, February 19, 2019

Housing Market in Slovenia

From the IMF’s latest report on Slovenia:

“Housing prices have completed their recovery from the deep slump during the double-dip crisis (2008–14) and continue to grow robustly, but current valuations do not point to overheating. The authorities have adopted macroprudential policy tools preemptively and continue to monitor developments. Easing supply constraints on the housing market could help to moderate future price increases.

Residential real estate prices rose at their fastest pace in 2017 since the outbreak of the crisis, recording the third highest rate in the euro area and a record number of transaction. Prices of used apartments in Ljubljana increased by 14.8 percent during 2017, compared to the national average increase of 11.8 percent. The overall housing price index rose 13.4 percent during the year to 2018: Q2.

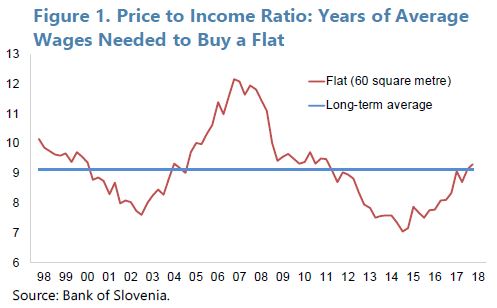

Housing remains affordable in historical and international comparison, and further appreciation in real house prices is likely. Wages and disposable incomes have increased since 2008, while real estate prices have only just reached their pre-crisis level. By some measures, the ratio of real estate prices to incomes stood at their long-term average in 2018 (Figure 1). At 54.4 percent, Slovenia has the second-lowest urbanization rate in the EU. Continued urbanization and growth in household incomes are expected to fuel continued appreciation of real estate prices.

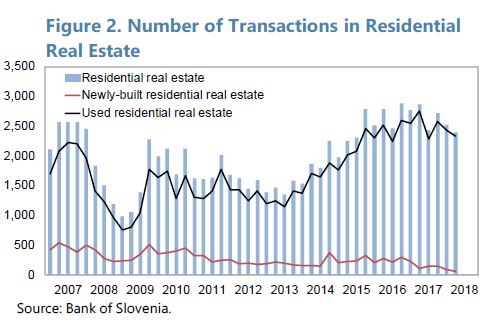

The supply of new residential housing has failed to keep pace with demand. The stock of housing in Slovenia is low by regional standards with 410 units per 1000 residents (compared to 547 in Austria and 524 in Croatia). The number of residential real estate transactions has been rising after 2013, yet the sales of newly-built units has dropped further from very low levels (Figure 2). The lack of supply response is related to the bankruptcy of major construction companies during the crisis years, the reluctance of banks to finance new construction, and constraints placed on new construction by urban planning and regulation.

Mortgage financing is not a significant driver of housing price developments. Slovenia has a comparatively high level of owner-occupied housing (77 percent of households, compared to 60 percent in the euro area, but comparable to other CEE countries). Only about 10 percent of households have a mortgage (19 percent in the euro area), and about a third of recent housing transactions was carried out with equity (i.e., without bank financing). The growth in mortgage lending has been positive since 2013, nearly reaching 5 percent year-on-year in 2017, but has since fallen back to below 4 percent.

The BoS has adopted macro-prudential policy tools as a preemptive step. Current data do not point to an overheating housing market or exposure by the banking sector. However, continued price increases and the inflexible supply response suggest the need for close monitoring. Guidance to banks on loan-to-value and DSTI ratios related to residential real estate transactions and a countercyclical capital buffer were implemented in 2016. In 2018, the applicability of the ratios was expanded to include not only mortgages but all household debt, prompted by rapidly growing consumer lending (albeit from a low level). Early adoption of the tools affords the banking sector time to adjust and monitor lending practices accordingly.

The government seeks to improve the supply of social housing. In 2015, Slovenia adopted its National Housing Program 2015–25 which calls for a new rental policy and an increase in social housing stock for the benefit of vulnerable groups, including young families and the elderly. The National Housing Fund, currently financing social housing investments by municipalities, could become a direct supplier, alleviating shortages of affordable housing.

Urban planning practices could be reformed to ease the supply of new housing. Zoning restrictions and the effort and time required to obtain all required permits before starting new construction projects impede the market response to rising house prices. Regulatory reform could therefore help to increase supply and slow the increases in real estate prices and rents.”

Posted by at 3:28 PM

Labels: Global Housing Watch

Subscribe to: Posts