Showing posts with label Global Housing Watch. Show all posts

Friday, May 24, 2019

Housing View – May 24, 2019

On cross-country:

- Debate Over Lunch: How Architecture Brings Us Together – OECD

- Identifying booms and busts in house prices under heterogeneous expectations – Journal of Economic Dynamics and Control

- The housing cycle: What role for mortgage market development and housing finance? – Loughborough University

On rent control:

- Housing Supply Dynamics under Rent Control: What Can Evictions Tell Us? – American Economic Association

- Spatial Misallocation and Rent Controls – American Economic Association

- The Effects of Second-Generation Rent Control on Land Values – American Economic Association

- Who Pays for Rent Control? Heterogeneous Landlord Response to San Francisco’s Rent Control Expansion – Stanford University

On the US:

- Press Briefing on the Evolution and Future of Homeownership – Federal Reserve Bank of New York

- An expert’s 7 principles for solving America’s housing crisis – Vox

- Monetary Policy, Housing Rents, and Inflation Dynamics – Federal Reserve Board

- The Great Recession, education, race, and homeownership – Economic Policy Institute

- Why Isn’t The Black Homeownership Rate Higher Today Than When The 1968 Fair Housing Act Became Law? – Forbes

- ‘Fairbnb’ Wants to Be the Unproblematic Alternative to Airbnb – Citylab

- Trump Administration Wants To Cut Funding For Public Housing Repairs – NPR

- California Today: Lawmakers Shelve a Potential Remedy to the Housing Crisis – New York Times

- 3 Top REITs With High Dividend Yields Above 5% And Secure Payouts – Seeking Alpha

- Labor Demand Shocks and Housing Prices Across the United States: Does One Size Fit All? – Economic Development Quarterly

- Undersupply in Housing Inventory – CoreLogic

- Spain’s Richest Person Bets Billions on Prime U.S. Real Estate – Bloomberg

- Despite Resistance, Cities Turn to Density to Tackle Housing Inequality – CityLab

- Special Incentive for Property Buyers: A Foreign Passport – New York Times

- Shortage of cheaper houses stifles U.S. homes sales – Reuters

- California’s big housing bill tanked. Newsom is partly to blame – Los Angeles Times

- How Do Mortgage Refinances Affect Debt, Default, and Spending? – Harvard Joint Center for Housing Studies

On other countries:

- [Canada] Real estate prices and banking performance: evidence from Canada – Journal of Economics and Finance

- [India] Affordable Housing as Human Right – Yale University

- [Portugal] The impact of Airbnb on residential property values and rents: evidence from Portugal – Ideas

- [United Kingdom] UK housing: Resilient in the face of turmoil – ING

On cross-country:

- Debate Over Lunch: How Architecture Brings Us Together – OECD

- Identifying booms and busts in house prices under heterogeneous expectations – Journal of Economic Dynamics and Control

- The housing cycle: What role for mortgage market development and housing finance? – Loughborough University

On rent control:

- Housing Supply Dynamics under Rent Control: What Can Evictions Tell Us?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, May 17, 2019

Housing View – May 17, 2019

On cross-country:

- House Prices Are Up: Should We Be Happy? – IMF

- How real-estate barons have ridden the tech boom – The Economist

- “Housing affordability is a key determinant of individual well-being and overall economic growth” The World Bank Look at Housing, Mobility and Welfare – Housing Europe

- This Land is whose Land? Picking the Housing Europe annual conference theme – Housing Europe

- European Summer School for young professionals 2019 – Housing Europe

On the US:

- California’s Rent Control Advocates Are About To Get What They Want, Good and Hard – Reason

- Special briefing on new construction, housing supply, and home prices – American Enterprise Institute

- Proposed Rule Could Evict 55,000 Children From Subsidized Housing – NPR

- Chipping away at the mortgage deduction – Brookings Institute

- The Capital Region needs more housing – Brookings Institute

- AEI Housing Center announces 10 best and worst metro areas to live in for science, technology, engineering, and math (STEM) jobs – American Enterprise Institute

- A great choice by the Federal Housing Finance Agency – American Enterprise Institute

- Second Home Buyers and the Housing Boom and Bust – Federal Reserve Board

- When Airbnb Listings in a City Increase, So Do Rent Prices – Harvard Business Review

- Chinese nationals purchase more U.S. residential real estate than buyers from any other foreign country, but Trump’s trade war could soon end that – MarketWatch

On other countries:

- [Canada] Combatting Money Laundering in BC Real Estate – CityNews

- [Canada] Poloz Underestimates Housing Slump, Capital Economics Says – Bloomberg

- [China] The Demand for Reverse Mortgages in China – VoxChina

- [Netherlands] Amsterdam Parliament Seeks Three-Year Freeze for Housing Resales – Bloomberg

- [Singapore] Do Real Estate Agents Have Information Advantages in Housing Markets? – Journal of Financial Economics

On cross-country:

- House Prices Are Up: Should We Be Happy? – IMF

- How real-estate barons have ridden the tech boom – The Economist

- “Housing affordability is a key determinant of individual well-being and overall economic growth” The World Bank Look at Housing, Mobility and Welfare – Housing Europe

- This Land is whose Land? Picking the Housing Europe annual conference theme – Housing Europe

- European Summer School for young professionals 2019 – Housing Europe

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, May 13, 2019

Evolution of Macroprudential Policies in Korea

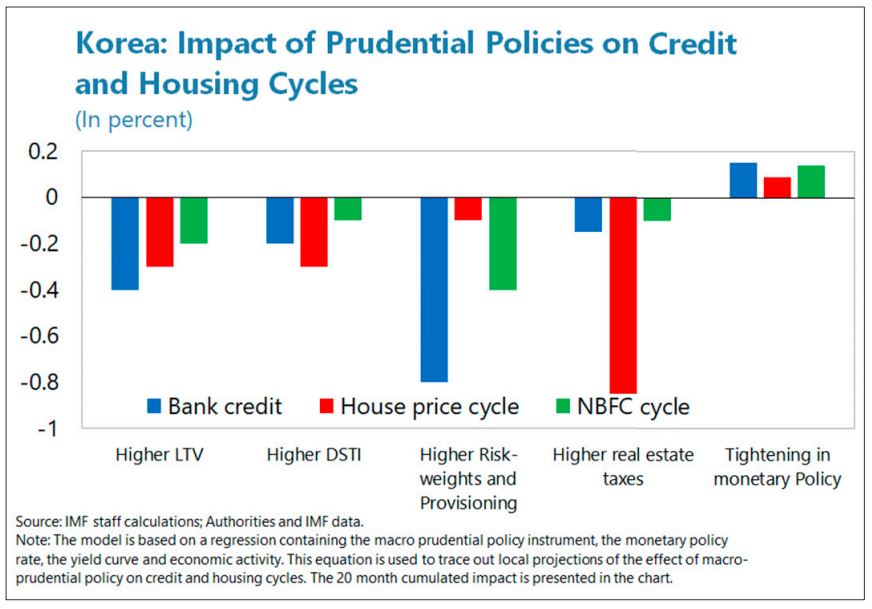

From the IMF’s latest report on Korea:

“Evidence for Korea suggests that financial stability will not necessarily materialize as a natural by-product of a so-called appropriate monetary policy stance. Although the effects of monetary and macroprudential instruments may overlap, they are not perfect substitutes. Empirical evidence for Korea shows that macroprudential policy have made two active contributions to limit financial risks to the wider economy:

- Preempting aggregate weakness by limiting the buildup of risk, thereby reducing the occurrence of crises. Macroprudential policies can reduce the procyclical feedback between asset prices and credit.

- Reducing the systemic vulnerability by increasing the resilience of the financial system. By building buffers, macroprudential policy helps maintain the ability of the financial system to provide credit to the economy, even under adverse conditions.

Policymakers should be mindful that macroprudential policy is not free of costs and that there may be trade-offs between the stability and the efficiency of financial systems. For instance, when policymakers impose high capital and liquidity requirements on financial institutions, they may enhance the stability of the system, but they also drive up the price of credit. For macroprudential policy to contribute to financial stability and social welfare, its objectives need to be defined clearly and in a manner that can form the basis of a strong accountability framework.”

From the IMF’s latest report on Korea:

“Evidence for Korea suggests that financial stability will not necessarily materialize as a natural by-product of a so-called appropriate monetary policy stance. Although the effects of monetary and macroprudential instruments may overlap, they are not perfect substitutes. Empirical evidence for Korea shows that macroprudential policy have made two active contributions to limit financial risks to the wider economy:

- Preempting aggregate weakness by limiting the buildup of risk,

Posted by at 3:33 PM

Labels: Global Housing Watch

Housing Market in Luxembourg

From the IMF’s latest report on Luxembourg:

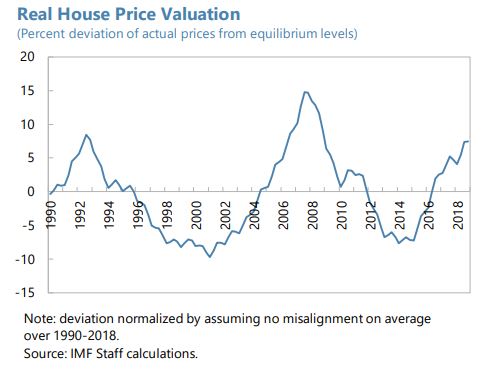

“Real house prices are estimated to be slightly overvalued in 2018. The percent deviation between the actual house price index and the predicted house price index suggests that real house prices were slightly overvalued, by about 7.5 percent in 2018.

Going forward, given supply constraints, Brexit-related immigration flows could add demand pressures and increase overvaluation of residential real estate (RRE) prices.

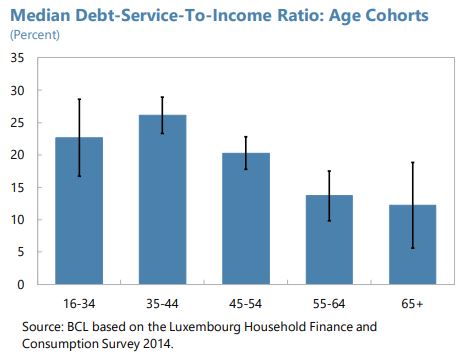

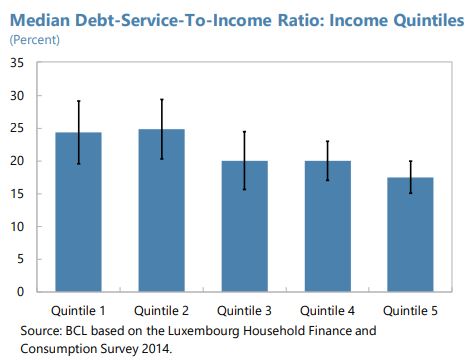

However, elevated household indebtedness indicates medium-term vulnerabilities, especially among younger age cohorts. Household debt remained high at about 170 percent of net disposable income in 2017, placing Luxembourg above the average of OECD countries. According to the latest available data from CSSF, 32 percent of households have a debt-service-to-income (DSTI) ratio greater than 45 percent. Disaggregated data from Household Finance and Consumption Survey (2014) indicates very high debt-to-income and DSTI ratios for younger cohorts (below 45 years old). The median and 75th percentile DSTI ratios were approaching 25 and 40 percent of disposable income, respectively. Classified by income quintiles, debt service burden is larger for poorer households (quintiles 1 and 2). In 2018, the share of adjustable rate mortgages in new mortgages remained stable at about 50 percent, indicating that some household balance sheets remain vulnerable to interest rate risks. These vulnerabilities would be exacerbated should monetary policy normalize faster than anticipated.

Rising RRE prices and elevated household indebtedness require continued monitoring of financial stability risks including banks’ ability to absorb price declines. Non-performing loans (NPLs) in the real estate sector remain low, with the ratio of total NPLs in RRE to total assets of the domestic banking system at 0.18 percent. However, borrower-based indicators point towards the need for closer monitoring of financial stability risks. Loan-to-value (LTV) ratios above 80 percent, for instance, are high at 31 percent of the outstanding mortgage stock. This is expected to increase further as one half of all new mortgage loans continue to have LTV ratios above 80 percent.”

From the IMF’s latest report on Luxembourg:

“Real house prices are estimated to be slightly overvalued in 2018. The percent deviation between the actual house price index and the predicted house price index suggests that real house prices were slightly overvalued, by about 7.5 percent in 2018.

Going forward, given supply constraints, Brexit-related immigration flows could add demand pressures and increase overvaluation of residential real estate (RRE) prices.

However,

Posted by at 10:40 AM

Labels: Global Housing Watch

Friday, May 10, 2019

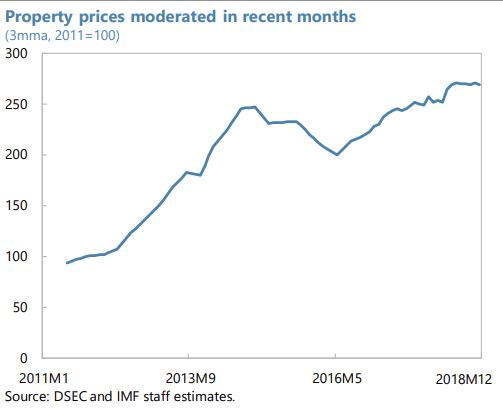

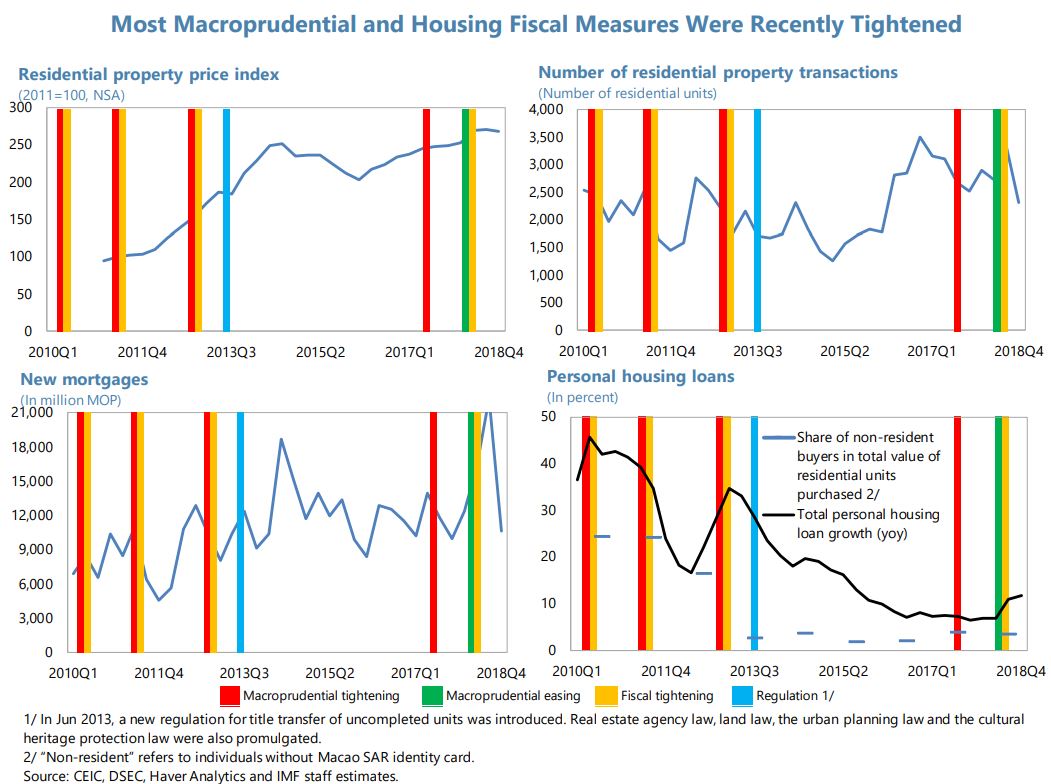

Housing Market in Macao

From the IMF’s latest report on Macao:

“The housing market has strongly recovered with the economic rebound that started in mid-2016, but the market appears to have cooled in the second half of 2018. After falling between mid-2014 and mid-2016, the residential property price index recovered fully between mid2016 and mid-2018 (in real terms), though it stayed flat in the second half of 2018. Even though residential property prices remained below trend in 2018, they appear to remain somewhat overvalued, for smaller units in particular (…).

The current housing macroprudential stance and related fiscal measures appear broadly appropriate. Measures were put in place in 2017 and 2018:

- New measures were introduced to mitigate housing market risks via containment of demand. The loan-to-value limit for non-first-time homebuyers was tightened in May 2017. In February 2018, property tax exemptions on vacant properties were removed and a special stamp duty tax on the purchase of non-first residential property was introduced.

On the other hand, the AMCM eased loanto-value limits for young first-time homebuyers to help affordability in February 2018 that may have unintentionally boosted demand and prices in this segment. Systemic risks in the housing market appear broadly contained. The authorities should continue monitoring residential property prices and the effects of recent housing market measures, as they may usually play out with a lag. Further actions should take into account evolving market conditions, including the recent growth deceleration and leveling off in residential property prices. In the event that residential property prices resume strong growth and may pose a risk to financial stability, the authorities could consider tightening macroprudential and/or fiscal-based measures property transactions by nonresidents during the housing market boom in 2010-2011. The main objective was to put in place a preventive measure to strengthen banks’ risk management considering the spike in nonresident NPLs during the Asian Financial Crisis. In 2017, to curb financial stability risks from strong growth in residential property prices, the AMCM tightened LTV for residents and nonresidents simultaneously.

- To attain the same policy objective without differentiating between residents and nonresidents, the authorities could examine whether they can protect against greater credit risk from lending to nonresidents through the existing multi-tiered-LTV structure but without the residency-based feature or by linking the differentiation in LTV limits directly to banks’ risk assessment of loans and borrowers, supported by additional measures such as enhancing information requirements and enforcement across borders and requiring banks to take into account country transfer or legal risk in their risk assessment. Further strengthening supervisory capacity of banks’ mortgage lending, broadly in line with FSAP recommendations (…), will be important to help ensure that these alternative measures are feasible

A broader set of policies should support housing affordability, where continued efforts to boost housing supply will be key. The apparent cooling of the housing market is welcome and may contribute to improving housing affordability. However, remaining affordability concerns should be addressed by a broader set of supply policies:

- Planning, zoning, and other reforms affect supply and prices only with long lags, and underlying demand for housing is expected to remain robust. Housing supply reforms should, therefore, not be delayed. Building on the government’s recent efforts to boost housing supply, plans should advance regulatory policy within a transparent framework that supports private sector supply and boosts well-targeted public housing supply, including via higher infrastructure spending.

- A coordinated government strategy to foster public and private housing supply, including an urban planning framework and urban renewal plan, would help guide reform efforts. While completing needed environmental, design, transportation and other assessments, procedures should be expedited.

Authorities’ Views.

- Housing market and policies. The authorities agreed that the housing market cooled in 2018 but remained somewhat overvalued. They noted that they stand ready to take further actions dependent on market conditions. They considered that the 2018 LTV loosening (for young firsttime homebuyers) was effective in increasing credit for this group, but acknowledged its contribution to higher prices in the small-property segment. On the residency-based LTV, they took note of the recommendation to replace the differentiation between residents and nonresidents with alternative measures. They highlighted that the objectives of the LTV framework are to strengthen banks’ risk management, curb investment/speculation motives, and moderate risks to the financial sector. They explained that the LTV framework is key for Macao SAR’s stability in light of its open capital account and large spillovers from its real estate sector. They highlighted that the 2017 LTV tightening was not aimed at nonresidents as it was done for both residents and nonresidents. They may consider other alternative measures as suggested when appropriate.

- Housing affordability. They agreed that boosting housing supply is key to address affordability concerns. In terms of public housing, they noted that ongoing projects will satisfy public housing needs by 2026 (by when they plan to add 50,000 public housing units) and they will carry on research analysis on public housing demand (including post-2026). They also noted measures under consideration to make public housing more targeted to the vulnerable. They explained that there are authorities which coordinate the strategy on public and private housing and noted that a draft master plan (to be completed in 2019) will support private housing development.”

From the IMF’s latest report on Macao:

“The housing market has strongly recovered with the economic rebound that started in mid-2016, but the market appears to have cooled in the second half of 2018. After falling between mid-2014 and mid-2016, the residential property price index recovered fully between mid2016 and mid-2018 (in real terms), though it stayed flat in the second half of 2018. Even though residential property prices remained below trend in 2018,

Posted by at 1:31 PM

Labels: Global Housing Watch

Subscribe to: Posts