Showing posts with label Global Housing Watch. Show all posts

Monday, July 1, 2019

Summer Reading: Recommendations by Experts on Housing Markets

Global Housing Watch Newsletter: June 2019

Looking for something to read over the summer? We asked experts for suggestions on books and papers to read on housing markets. Below are their picks:

Perceptions of House Price Risk and Homeownership by Manuel Adelino (Duke University), Antoinette Schoar (MIT) and Felipe Severino (Dartmouth College)

Nominated by: Ian Bright (ING)

Why? “People in the US generally consider buying a home to be a safe investment but there is considerable variation depending on income and age and between renters or owners. Further, the risks associated with home ownership are perceived to be much lower than and not correlated with owning shares but are positively correlated with past and expected movements in house prices. The results support suggestions that bubbles develop in house prices and help explain why individuals place more of their wealth towards housing than seems efficient. Similar patterns seem to exist in several European countries but have not been analyzed as thoroughly.”

Building the city: urban transition and institutional frictions by J. Vernon Henderson, Tanner Regan, and Anthony J. Venables

Nominated by: Remi Jedwab (George Washington University)

Why? “Very few papers have data on buildings and housing prices in developing countries.”

House Prices, (Un) Affordability and Systemic Risk by Efthymios Pavlidis, Ivan Paya and Alexandros Skouralis (all at Lancaster University Management School)

Nominated by: Enrique Martínez-García (Federal Reserve Bank of Dallas)

Why? “This is a very interesting contribution in an area (the intersection between housing economics and financial stability) that has a lot of academic and policy interest and few references. In this paper, the authors show employing the ∆CoVaR methodology developed by Adrian and Brunnermeier (2011, 2016) on U.K. data that, when the real estate sector is under distress, the tail risk of the entire financial system increases significantly. Their novel work also lends empirical support to the hypothesis that the banking sector is central for the transmission of systemic risk from housing to the overall financial sector. These results are, therefore, very relevant to assess the health of the financial system and its exposure to housing (for financial stability purposes).”

Order without Design: How Markets Shape Cities by Alain Bertaud (New York University)

Nominated by: Stephen Malpezzi (University of Wisconsin-Madison)

Why? “Order Without Design is one of the most important books ever written about cities. Acclaimed planner-architect-urbanist Alain Bertaud distills lessons from a half century of practical and analytical work in dozens of cities ranging from New York and Paris, to Sana’a and Port-au-Prince. Transport, land and housing, labor markets, urban form, and the proper role of urban planning are all covered concisely yet in amazing depth. Rigorous yet eminently readable, the book is a lively demonstration of the gains from trade between planners and economists.”

Boom Town: The Fantastical Saga of Oklahoma City, its Chaotic Founding… its Purloined Basketball Team, and the Dream of Becoming a World-class Metropolis by Sam Anderson

Nominated by: Paavo Monkkonen, (University of California, Los Angeles)

Why? “By far the best “city” book I have read in a long time is called Boom Town by Sam Anderson. The history of Oklahoma City is fascinating! Not so much about housing markets, but it does have a chapter on the land rush settlement of the city (which is an amazing story) as well as segregation and urban renewal.”

Triumph of the City: How Our Greatest Invention Makes Us Richer, Smarter, Greener, Healthier, and Happier by Edward L. Glaeser (Harvard University)

Nominated by: Frank Nothaft (CoreLogic)

Why? “Urbanization has been a global trend that accelerated with the industrial revolution. Harvard Professor Edward Glaeser presents the basic tenets of urban economics in an accessible manner to reach a wide audience, to reveal why cities have been the spark for innovation and the engine for job creation. He places the evolution of urbanization within an historical context: The Black Plague and slums of early industrialization have largely given way to modern metropolises that serve as the focal point for economic vitality. His writing flows naturally and is punctuated with examples he has observed in his international research. Today in America the urban core is experiencing a renaissance of activity and attracting new millennial households. You do not have to be a PhD economist to understand how this has occurred once you have read his book.”

Evicted: Poverty and Profit in the American City by Matthew Desmond and The Dream Revisited: Contemporary Debates About Housing, Segregation, and Opportunity by Ingrid Ellen and Justin Steil

Nominated by: Stijn Van Nieuwerburgh (New York University)

Why? “I would like to recommend two books, one which I have read and one which I am planning to read. Evicted by Matthew Desmond is an in-depth study of the eviction crisis in America. Through personal anecdote, Desmond tells a gripping story of eviction, housing segregation, and poverty. Towards the end of the book, he generalizes to the macro level and discusses implications for affordable housing policy. Beautifully written and inspiring for any economist interested in pursuing housing research. The second book is The Dream Revisited by Ingrid Ellen-Gould, from the Furman Center at New York University. The book brings together several experts to discuss affordable housing 50 years after the Fair Housing Act.”

Photo by Pj Accetturo

Global Housing Watch Newsletter: June 2019

Looking for something to read over the summer? We asked experts for suggestions on books and papers to read on housing markets. Below are their picks:

Perceptions of House Price Risk and Homeownership by Manuel Adelino (Duke University), Antoinette Schoar (MIT) and Felipe Severino (Dartmouth College)

Nominated by: Ian Bright (ING)

Why?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 27, 2019

Housing View – June 28, 2019

On cross-country:

- A housing market slump could drive global growth to a decade low, economists warn – MarketWatch

- Housing markets and macroeconomic risks – OECD

- Peak property: Building a bubble – Financial Times

- Recent Developments in the Economics of Housing – EconPapers

- Cities Are Surprisingly Fragile – Scientific American

- Residential real estate market cools in the eurozone – ING

On the US:

- 2019 State of the Nation’s Housing Report Shows US Housing Supply Falls Far Short of What is Needed – Harvard Joint Center for Housing Studies

- The Falling Supply of Low-Cost Rentals in US Metros – Harvard Joint Center for Housing Studies

- Working Class Americans Are Finding It Increasingly Difficult To Afford Housing – NPR

- Executive Order Establishing a White House Council on Eliminating Regulatory Barriers to Affordable Housing – White House

- Trump Administration to Take on Local Housing Barriers – Wall Street Journal

- Push to Overhaul Fannie, Freddie Nudges Up Mortgage Costs – Wall Street Journal

- Key Housing Indicators Weaken Further in 2019 – Federal Reserve Bank of St Louis

- The rent is still too damn high and 2020 candidates finally want to do something about it – CNN

- New data point to softening US housing market – Financial Times

- Nobody Knows What to Do About L.A.’s Homelessness Crisis – The Atlantic

- In Defense of Foreign Investment in U.S. Housing – Governing

- Rendezvous with density – Governing

- Democrats Get Serious About Affordable Housing – The American Prospect

On other countries:

- [China] Record Land Sale in Shenzhen Underscores China’s Housing Demand – Bloomberg

- [Italy] The role of arts in Venice’s property market – Financial Times

- [New Zealand] Delivering greater well-being in New Zealand: policy steps to increase housing affordability – OECD

- [Romania] Romania’s housing market cooling – Global Property Guide

- [South Korea] South Korea’s housing market improving – Global Property Guide

- [Sweden] Sweden’s house price boom is officially over – Global Property Guide

- [Ukraine] Ukraine’s housing market remains depressed – Global Property Guide

- [United Kingdom] Ikea wants to build homes in Britain that cost what the buyer can pay – CNN

On cross-country:

- A housing market slump could drive global growth to a decade low, economists warn – MarketWatch

- Housing markets and macroeconomic risks – OECD

- Peak property: Building a bubble – Financial Times

- Recent Developments in the Economics of Housing – EconPapers

- Cities Are Surprisingly Fragile – Scientific American

- Residential real estate market cools in the eurozone – ING

On the US:

- 2019 State of the Nation’s Housing Report Shows US Housing Supply Falls Far Short of What is Needed – Harvard Joint Center for Housing Studies

- The Falling Supply of Low-Cost Rentals in US Metros – Harvard Joint Center for Housing Studies

- Working Class Americans Are Finding It Increasingly Difficult To Afford Housing – NPR

- Executive Order Establishing a White House Council on Eliminating Regulatory Barriers to Affordable Housing – White House

- Trump Administration to Take on Local Housing Barriers – Wall Street Journal

- Push to Overhaul Fannie,

Posted by at 12:41 PM

Labels: Global Housing Watch

Tuesday, June 25, 2019

Assessing House Prices in Canada

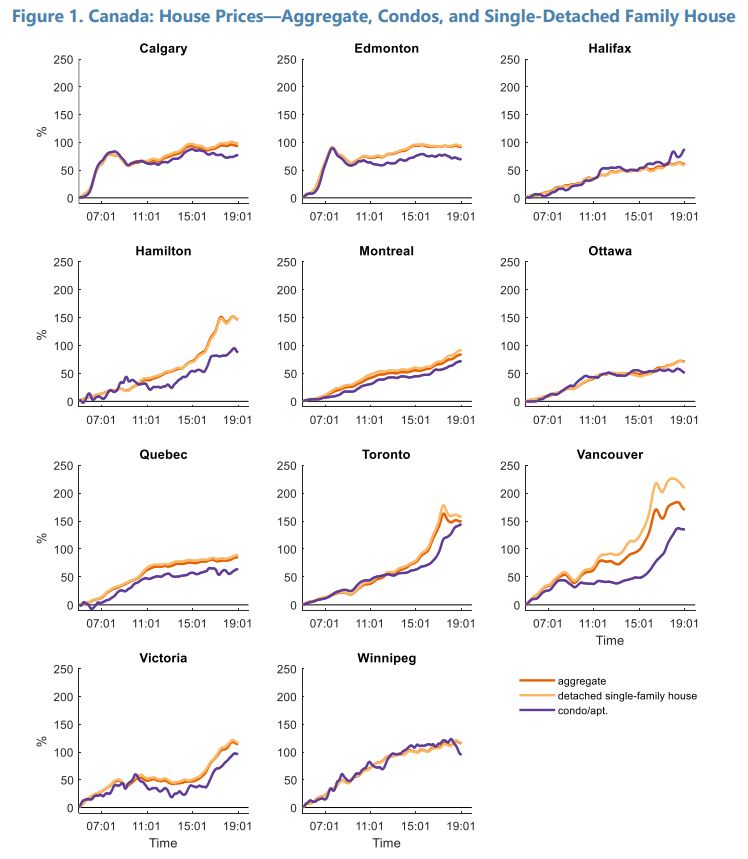

From the IMF’s latest report on Canada:

“House prices in most Canadian regions can be explained by economic fundamentals, but prices in Hamilton, Toronto, and Vancouver are currently well-above estimated attainable levels. Since 2000, house price developments in most metropolitan regions can be explained by robust income growth and a decline in mortgage interest rates. House prices have broadly increased in line with households’ borrowing capacity. However, since 2015, prices in Hamilton, Toronto, and Vancouver have deviated significantly from fundamentals. By the end of 2018, pricing gaps stood at around 50 percent for Toronto and Vancouver, and almost 60 percent for Hamilton.

The overvaluations currently observed in Hamilton, Toronto, and Vancouver are not unprecedented. In 2006, house prices in Calgary and Edmonton increased sharply above estimates of borrowing capacity. Pricing gaps normalized by 2012 due to a combination of moderate declines in house prices, strong household income growth, and a decline in interest rates. Looking ahead, housing markets in Hamilton, Toronto, and Vancouver are not likely to benefit from such significant declines in interest rates. This suggests that without very strong income growth, there is a risk of further price corrections in these markets.

Nationwide increases in price-to-income ratios have significantly lowered housing affordability. Declines in mortgage rates have generally been rapidly priced in by housing markets, increasing price-to-income and loan-to-income ratios. With rising price-to-income ratios, down payments have become larger, increasing the time it takes to save for a house, and adversely impacting housing affordability. While housing affordability has deteriorated in all of the regions examined, the deterioration has been most marked in Hamilton, Toronto, and Vancouver.

If house prices rapidly reflect households’ ability to borrow, even well-intentioned policies that improve access to credit are likely to increase house prices and adversely impact affordability. Policy measures that increase households’ capacity to borrow—such as increasing the mortgage loan amortization period or subsidizing loans—will likely put additional upward pressure on prices. Indeed, for such measures to work, the supply of housing would need to be exceptionally (and unrealistically) elastic, even in the short run. As such, policy measures focused on increasing housing supply are needed to durably improve housing affordability over the long term.”

From the IMF’s latest report on Canada:

“House prices in most Canadian regions can be explained by economic fundamentals, but prices in Hamilton, Toronto, and Vancouver are currently well-above estimated attainable levels. Since 2000, house price developments in most metropolitan regions can be explained by robust income growth and a decline in mortgage interest rates. House prices have broadly increased in line with households’ borrowing capacity. However, since 2015, prices in Hamilton,

Posted by at 3:51 PM

Labels: Global Housing Watch

U.S. Housing Market

From the IMF’s latest report on the United States:

- FSAP recommendation on housing finance: “Reinvigorate the momentum for comprehensive housing market reform”

- Developments: “Housing finance and the U.S. housing market have not been reformed comprehensively. Since the last FSAP, no legislative or executive action has been taken to reduce substantially the footprint of Fannie Mae and Freddie Mac (“Enterprises”).

As conservator, however, the (FHFA has required market-based credit risk transfers from the Enterprises to the private sector at an increasing level since 2013. Indeed, between their initiation in 2013 and June 2018, the Enterprises have transferred a portion of credit risk on approximately $2.5 trillion of unpaid principal balance (UPB) with a combined Risk in Force (RIF) of about $81 billion. The Enterprises have also jointly developed a common securitization platform. FHFA issued a final rule on the uniform mortgage-backed security in February 2019 to align Enterprise policies and practices that affect cash flows of To-Be-Announced (TBA) eligible mortgage-backed securities. These requirements apply to both the Enterprises’ current offerings and to the new Uniform Mortgage-Backed Security (UMBS), which the Enterprises plan to begin issuing in June 2019. These Enterprise reforms have been accomplished administratively and have not reformed the entire housing finance system, which would require legislative action.

Since 2015, the FHFA has directed the Enterprises to fund the Housing Trust Fund and Capital Magnet Funds (as required by the 2008 Housing and Economic Recovery Act) by transferring a portion of total new acquisitions to these funds, which are administered by the Department of Housing and Urban Development (HUD) and Treasury Department, respectively. FHFA has the discretion to suspend the Enterprise allocations to the affordable housing funds, including the Housing Trust Fund, if the allocations are contributing to the Enterprise’s financial instability.

The Senior Preferred Stock Purchase Agreements (PSPAs) between the Treasury and each Enterprise continue to provide financial strength for the Enterprises. They ensure the ability of the Enterprises to meet their financial obligations and are structured so that they will have minimal net worth as all profits above the capital reserve amount are transferred to Treasury each quarter. The capital reserve amount had been declining by $600 million per year and was scheduled to decline to zero by January 2018. However, on December 21, 2017, FHFA and the Department of the Treasury agreed to reinstate a $3 billion capital reserve amount for each Enterprise to prevent draws on the PSPA due to fluctuations in the Enterprises’ income due to the normal course of business. Despite the new capital reserve, the December 2017 tax cuts caused the Enterprises to draw a combined total of $4 billion at the end of that quarter, reflecting value loss in deferred tax assets that followed enactment of the Tax Cuts and Jobs Act of 2017.

In June 2018, FHFA issued a proposed rule on Enterprise capital requirements. The rule would implement a new framework for risk-based capital requirements and two alternatives for a revised minimum leverage capital requirement for the Enterprises. The capital requirements in this rule would continue to be suspended while the Enterprises remain in conservatorship.

On March 27, 2019, the White House issued a Presidential Memorandum on Federal Housing Finance Reform. The memorandum establishes principles for reform and assigns responsibility to the Secretaries of the Treasury and HUD to develop plans for administrative and legislative reforms for the Enterprises and the housing programs of the federal government. As part of the process, the Treasury Department and HUD are required to consult with the leaders of other government agencies involved in housing finance and economic policy, including FHFA, and must submit the plan to the President for approval.”

From the IMF’s latest report on the United States:

- FSAP recommendation on housing finance: “Reinvigorate the momentum for comprehensive housing market reform”

- Developments: “Housing finance and the U.S. housing market have not been reformed comprehensively. Since the last FSAP, no legislative or executive action has been taken to reduce substantially the footprint of Fannie Mae and Freddie Mac (“Enterprises”).

As conservator, however, the (FHFA has required market-based credit risk transfers from the Enterprises to the private sector at an increasing level since 2013.

Posted by at 11:33 AM

Labels: Global Housing Watch

Housing Market in Denmark

From IMF’s latest report on Denmark:

“The housing market plays a vital role in Denmark, reinforcing macro-financial linkages. High mandatory pension contributions and household savings have created a pension system that has facilitated the development of the world’s largest covered bond market in percent of GDP. Insurance companies, pension funds, and foreign investors are among the largest holders of covered bonds, which are issued by MCIs to fund household mortgages (…). Thus, housing asset exposures interlink MCIs, pension funds, insurance, foreign investors, and the household sector. Hence, shocks to real estate may impact negatively households’ financial and non-financial assets, hindering consumption; thus, reinforcing macro-financial linkages (SIP 2018).

High household leverage amid high house valuations remains a key source of macrofinancial vulnerability. High house prices, a favorable tax treatment, and easy access to low-cost borrowing incentivize the funding of housing with large mortgages. These factors explain why Danish households’ debt-to-income ratios are among the highest in advanced economies. Large liabilities are counterbalanced by large assets (housing and pension). However, high gross debt, combined with illiquid assets (concentrated in real estate) expose households to price and interest rate shocks that can impact asymmetrically their balance sheet. Two types of households appear particularly vulnerable. Households who have purchased in potentially overvalued urban areas (SIP 2018), where loan-to-income (LTI) ratios and credit growth are higher than anywhere else. And low-income households who spend a significant share of their income on housing. These vulnerabilities are compounded by the large proportion of variable-rate and interest-only mortgages in the system (…).

Recent developments are encouraging but further action is needed. Staff welcomes the comprehensive suite of policies that have been implemented in recent years. These include policies targeting households and financial intermediaries in the form of macroprudential policies (SIP 2018), supervisory guidance for MCIs and banks, and a reform of property taxation (IMF 2017). While overall house prices are softening and households are switching to loans with higher amortization and lower interest rate risk, staff advocates further deployment of coordinated policies to address remaining vulnerabilities.

Macroprudential instruments. In an economy with elevated house prices, rules targeting loan-to-value (LTVs) become less binding. Thus, increased focus on income-based measures, including debt-to-income (DTI), loan-to-income (LTI) and debt-service-to-income (DSTI) might prove more effective in addressing high leverage and encourage faster amortization. Staff welcomes rules implemented in 2018 to limit lending via interest-only and floating-rate mortgages to highly-indebted households.21 However, authorities could strengthen DTI restrictions for all loans, irrespective of their loan-to-value ratios. Tighter limits on income based measures for interest-only and adjustable-rate mortgages should also be considered, while calibrating limits to these measures for lower risk groups—first-time home buyers and low-levered households—and where financing is via fixed–rate mortgages.22 Highly-leveraged households—with debt-to-income above 400 percent—should be subject to mandatory amortization, irrespective of amortization periods (SIP 2018).

Macroprudential framework. A review of the efficacy of policy implementation is encouraged, including a review of institutional arrangements (…). The process followed by the SRC to arrive at a recommendation can take too long, potentially hindering implementation. Given that the decision-making power lies with the government, there is a risk that political considerations could delay the consensus process that tends to form the basis of such recommendations (FSAP 2014). Experience from other countries indicates that improvements in timeliness can be achieved by assigning independent authorities a macroprudential mandate which includes legal powers to implement macroprudential policy with corresponding transparency and accountability requirements.

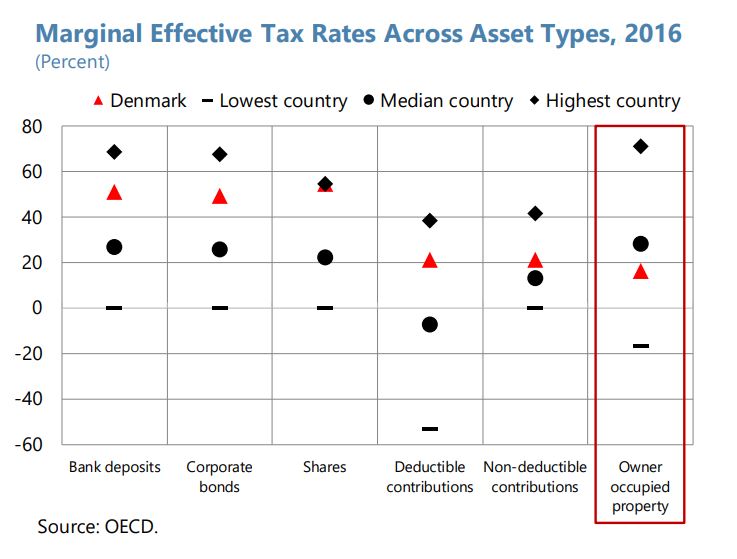

Tax policy. Tax treatment of owneroccupied housing is very favorable compared to other savings vehicles and most OECD countries. MID should be reduced further, taking advantage of the current low rate environment. To incentivize homeowners to swap risky mortgages, MID could be made conditional on amortizing and/or fixed rate mortgages. Balancing tax incentives for pension contributions could release resources for larger down-payments; thereby reducing household leverage.

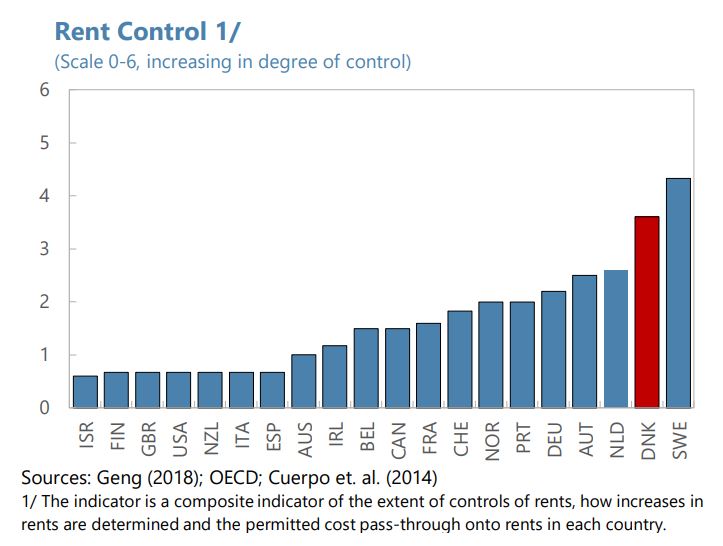

Housing supply. Rent controls in Denmark, among the highest in advanced economies, should be reduced to stimulate the rental market, while protecting the interest of the most vulnerable. Restrictions on the size of new apartments should be relaxed in urban areas to improve demand-supply mismatches. Upgrading of public transportation could relieve house price pressures around fast growing urban centers. Streamlined zoning and planning procedures across municipalities could increase supply, thereby alleviating price pressures.

Authorities agree that macro-financial risks stemming from the interaction between high household leverage and high house valuations should be followed closely. Authorities indicate that household resilience to interest rate increases likely improved as more homeowners continue shifting towards fixed rate mortgages and longer fixing periods. They also welcome the recent softening in apartment prices. The authorities argue that additional measures would require further analysis of the effects on the housing market and the overall economy. Authorities see the macroprudential framework as well functioning including the timeframe for the CCyB implementation and SRC’s independence. The DN notes that the long-term success of the framework depends on policy-makers’ continued implementation of the SRC’s recommendations.”

From IMF’s latest report on Denmark:

“The housing market plays a vital role in Denmark, reinforcing macro-financial linkages. High mandatory pension contributions and household savings have created a pension system that has facilitated the development of the world’s largest covered bond market in percent of GDP. Insurance companies, pension funds, and foreign investors are among the largest holders of covered bonds, which are issued by MCIs to fund household mortgages (…).

Posted by at 11:19 AM

Labels: Global Housing Watch

Subscribe to: Posts