Showing posts with label Forecasting Forum. Show all posts

Friday, December 8, 2017

2018 Housing Forecasts

2018 Housing Forecasts collected by Bill McBride:

Posted by at 8:09 PM

Labels: Forecasting Forum, Global Housing Watch

Monday, October 30, 2017

Debt Sustainability Analyses for Low-Income Countries: An Assessment of Projection Performance

From a new IMF working paper: “This paper develops new error assessment methods to evaluate the performance of debt sustainability analyses (DSAs) for low-income countries (LICs) from 2005-2015. We find some evidence of a bias towards optimism for public and external debt projections, which was most appreciable for LICs with the highest incomes, prospects for market access, and at ‘moderate’ risk of debt distress. This was often driven by overly-ambitious fiscal and/or growth forecasts, and projected ‘residuals’. When we control for unanticipated shocks, we find that biases remain evident, driven in part by optimism regarding government fiscal reaction functions and expected growth dividends from investment.

From a new IMF working paper: “This paper develops new error assessment methods to evaluate the performance of debt sustainability analyses (DSAs) for low-income countries (LICs) from 2005-2015. We find some evidence of a bias towards optimism for public and external debt projections, which was most appreciable for LICs with the highest incomes, prospects for market access, and at ‘moderate’ risk of debt distress. This was often driven by overly-ambitious fiscal and/or growth forecasts,

Posted by at 4:25 PM

Labels: Forecasting Forum

Sunday, September 3, 2017

Why economic forecasting has always been a flawed science

A BBC Radio 4 programme quoted my research:

“Prakash Loungani at the IMF analysed the accuracy of economic forecasters and found something remarkable and worrying. ‘The record of failure to predict recessions is virtually unblemished,’ he said.

His analysis revealed that economists had failed to predict 148 of the past 150 recessions. Part of the problem, he said, was that there wasn’t much of a reputational gain to be had by predicting a recession others had missed. If you disagreed with the consensus, you would be met with scepticism. The downside of getting it wrong was more personally damaging than the upside of getting it right.”

Continue reading here.

A BBC Radio 4 programme quoted my research:

“Prakash Loungani at the IMF analysed the accuracy of economic forecasters and found something remarkable and worrying. ‘The record of failure to predict recessions is virtually unblemished,’ he said.

His analysis revealed that economists had failed to predict 148 of the past 150 recessions. Part of the problem, he said, was that there wasn’t much of a reputational gain to be had by predicting a recession others had missed.

Posted by at 12:11 AM

Labels: Forecasting Forum

Tuesday, August 1, 2017

Bridging the Gap: Forecasting Interest Rates with Macro Trends

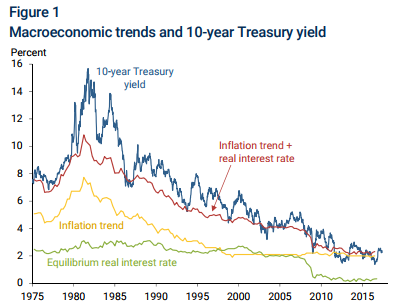

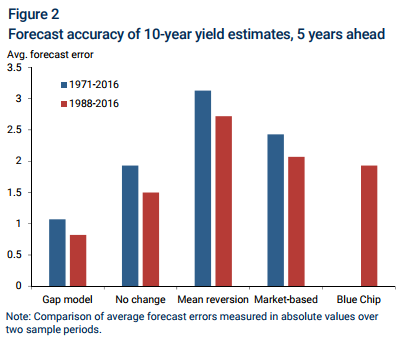

A new economic letter by Michael Bauer says that “Interest rates are inherently difficult to predict, and the simple random walk benchmark has proven hard to beat. But macroeconomics can help, because the long-run trend in interest rates is driven by the trend in inflation and the equilibrium real interest rate. When forecasting rates several years into the future, substantial gains are possible by predicting that the gap between current interest rates and this long-run trend will close with increasing forecast horizon. This evidence suggests that accounting for macroeconomic trends is important for understanding, modeling, and forecasting interest rates.”

Continue reading here.

A new economic letter by Michael Bauer says that “Interest rates are inherently difficult to predict, and the simple random walk benchmark has proven hard to beat. But macroeconomics can help, because the long-run trend in interest rates is driven by the trend in inflation and the equilibrium real interest rate. When forecasting rates several years into the future, substantial gains are possible by predicting that the gap between current interest rates and this long-run trend will close with increasing forecast horizon.

Posted by at 9:49 AM

Labels: Forecasting Forum

Thursday, July 27, 2017

Why economists cannot forecast recessions

A new article by Alasdair Macleod quoted my research: “Loungani was recently interviewed for a BBC programme, updating his original paper. In that interview, he claimed that over three decades, of the 150 recessions recorded only two had been forecast, implying that since the turn of the century no recessions had been forecast at all.ii The failure rate has increased to 100%, not decreased, as might be expected from economic models that are updated in the light of experience.”

Continue reading here.

A new article by Alasdair Macleod quoted my research: “Loungani was recently interviewed for a BBC programme, updating his original paper. In that interview, he claimed that over three decades, of the 150 recessions recorded only two had been forecast, implying that since the turn of the century no recessions had been forecast at all.ii The failure rate has increased to 100%, not decreased, as might be expected from economic models that are updated in the light of experience.”

Posted by at 6:43 PM

Labels: Forecasting Forum

Subscribe to: Posts