Showing posts with label Forecasting Forum. Show all posts

Thursday, March 22, 2018

Paul Ehrlich: “Collapse of civilisation is a near certainty within decades”

From an interview article by Damian Carrington:

“Ashattering collapse of civilisation is a “near certainty” in the next few decades due to humanity’s continuing destruction of the natural world that sustains all life on Earth, according to biologist Prof Paul Ehrlich.

In May, it will be 50 years since the eminent biologist published his most famous and controversial book, the Population Bomb. But Ehrlich remains as outspoken as ever.

The world’s optimum population is less than two billion people – 5.6 billion fewer than on the planet today, he argues, and there is an increasing toxification of the entire planet by synthetic chemicals that may be more dangerous to people and wildlife than climate change.

Ehrlich also says an unprecedented redistribution of wealth is needed to end the over-consumption of resources, but “the rich who now run the global system – that hold the annual ‘world destroyer’ meetings in Davos – are unlikely to let it happen”.

[…]

More of Paul and Anne Ehrlich’s reflections on their book are published in The Population Bomb Revisited.”

From an interview article by Damian Carrington:

“Ashattering collapse of civilisation is a “near certainty” in the next few decades due to humanity’s continuing destruction of the natural world that sustains all life on Earth, according to biologist Prof Paul Ehrlich.

In May, it will be 50 years since the eminent biologist published his most famous and controversial book, the Population Bomb. But Ehrlich remains as outspoken as ever.

Posted by at 1:16 PM

Labels: Forecasting Forum

Monday, March 12, 2018

Can Central Bankers Become Superforecasters?

From a new post by Aakash Mankodi and Tim Pike:

“Tetlock and Gardner’s acclaimed work on Superforecasting provides a compelling case for seeing forecasting as a skill that can be improved, and one that is related to the behavioural traits of the forecaster. These so-called Superforecasters have in recent years been pitted against experts ranging from U.S intelligence analysts to participants in the World Economic Forum, and have performed on par or better by accurately predicting the outcomes of a broad range of questions. Sounds like music to a central banker’s ears? In this post, we examine the traits of these individuals, compare them with economic forecasting and draw some related lessons. We conclude that considering the principles and applications of Superforecasting can enhance the work of central bank forecasting.

[…]

With continuous forecasting challenges on the horizon in coming years, perhaps it is an opportune time to incorporate these ideas in the central banking sphere. Economic forecasting will always be an imperfect science. So while it is unlikely that a major shock such as the global financial crisis would have been averted by improving the accuracy of forecasting efforts in these ways, we believe the lessons learnt through the experiment of Superforecasting have a lot to offer to take forecasting a step forward in that direction. Potentially over time, we might be able to create a next generation of central bank Superforecasters.”

From a new post by Aakash Mankodi and Tim Pike:

“Tetlock and Gardner’s acclaimed work on Superforecasting provides a compelling case for seeing forecasting as a skill that can be improved, and one that is related to the behavioural traits of the forecaster. These so-called Superforecasters have in recent years been pitted against experts ranging from U.S intelligence analysts to participants in the World Economic Forum,

Posted by at 9:10 AM

Labels: Forecasting Forum

Saturday, March 10, 2018

Forecasts in Times of Crises

From a new IMF working paper:

“Financial crises pose unique challenges for forecast accuracy. Using the IMF’s Monitoring of Fund Arrangement (MONA) database, we conduct the most comprehensive evaluation of IMF forecasts to date for countries in times of crises. We examine 29 macroeconomic variables in terms of bias, efficiency, and information content to find that IMF forecasts add substantial informational value as they consistently outperform naive forecast approaches. However, we also document that there is room for improvement: two thirds of the key macroeconomic variables that we examine are forecast inefficiently and 6 variables (growth of nominal GDP, public investment, private investment, the current account, net transfers, and government expenditures) exhibit significant forecast bias. Forecasts for low-income countries are the main drivers of forecast bias and inefficiency, reflecting perhaps larger shocks and lower data quality. When we decompose the forecast errors into their sources, we find that forecast errors for private consumption growth are the key contributor to GDP growth forecast errors. Similarly, forecast errors for non-interest expenditure growth and tax revenue growth are crucial determinants of the forecast errors in the growth of fiscal budgets. Forecast errors for balance of payments growth are significantly influenced by forecast errors in goods import growth. The results highlight which macroeconomic aggregates require further attention in future forecast models for countries in crises.”

From a new IMF working paper:

“Financial crises pose unique challenges for forecast accuracy. Using the IMF’s Monitoring of Fund Arrangement (MONA) database, we conduct the most comprehensive evaluation of IMF forecasts to date for countries in times of crises. We examine 29 macroeconomic variables in terms of bias, efficiency, and information content to find that IMF forecasts add substantial informational value as they consistently outperform naive forecast approaches. However,

Posted by at 10:57 PM

Labels: Forecasting Forum

Tuesday, March 6, 2018

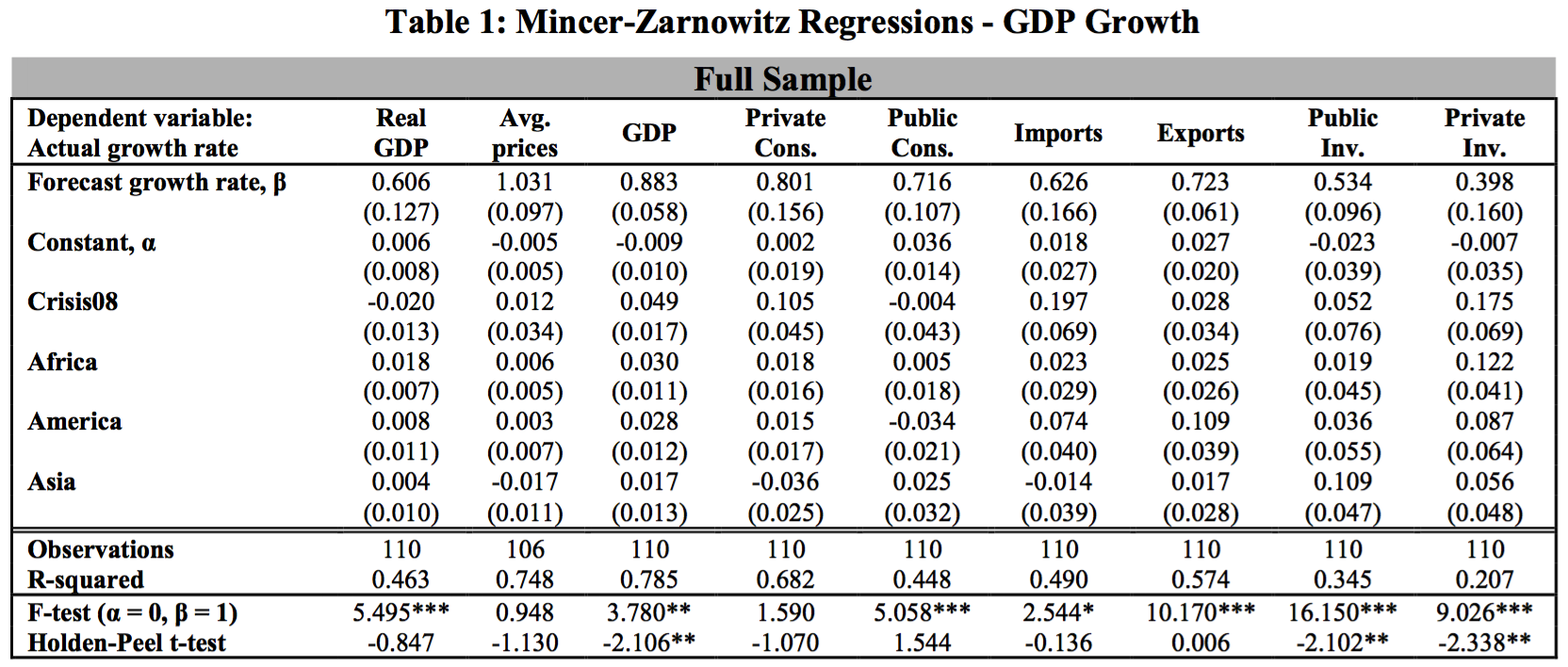

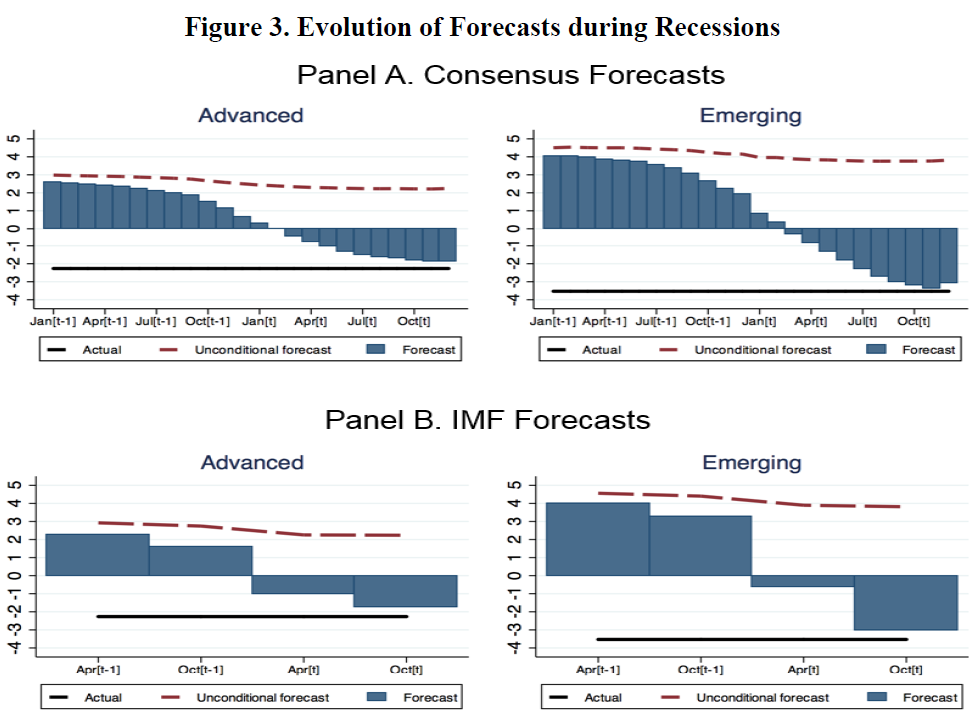

How Well Do Economists Forecast Recessions?

In my latest IMF working paper with Zidong An and Joao Jalles, “We describe the evolution of forecasts in the run-up to recessions. The GDP forecasts cover 63 countries for the years 1992 to 2014. The main finding is that, while forecasters are generally aware that recession years will be different from other years, they miss the magnitude of the recession by a wide margin until the year is almost over. Forecasts during non-recession years are revised slowly; in recession years, the pace of revision picks up but not sufficiently to avoid large forecast errors. Our second finding is that forecasts of the private sector and the official sector are virtually identical; thus, both are equally good at missing recessions. Strong booms are also missed, providing suggestive evidence for Nordhaus’ (1987) view that behavioral factors—the reluctance to absorb either good or bad news—play a role in the evolution of forecasts.”

In my latest IMF working paper with Zidong An and Joao Jalles, “We describe the evolution of forecasts in the run-up to recessions. The GDP forecasts cover 63 countries for the years 1992 to 2014. The main finding is that, while forecasters are generally aware that recession years will be different from other years, they miss the magnitude of the recession by a wide margin until the year is almost over.

Posted by at 8:38 AM

Labels: Forecasting Forum

Tuesday, February 27, 2018

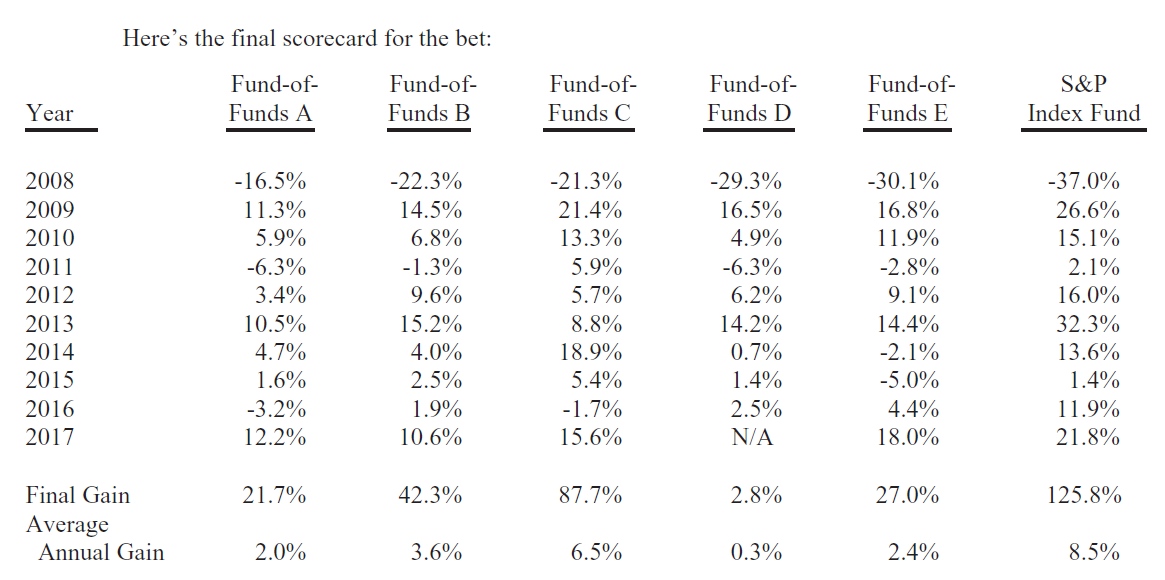

Warren Buffett Summarizes Investment Lessons from Winning His 10-year Bet that a Passive S&P 500 Index Fund Would Out-Perform Actively Managed Hedge Funds

From a new blog by Mark J. Perry:

“In Warren Buffett’s 2017 annual letter to shareholders, released on Saturday, he discussed the ten-year bet he made in 2007 that an unmanaged, low-cost S&P-500 index fund would out-perform an actively managed group of high-cost hedge funds over a ten-year period from 2008 to 2017, when performance is measured on a basis net of fees, costs, and all expenses. See posts here, here and here for past coverage of Buffett’s famous bet.”

From a new blog by Mark J. Perry:

“In Warren Buffett’s 2017 annual letter to shareholders, released on Saturday, he discussed the ten-year bet he made in 2007 that an unmanaged, low-cost S&P-500 index fund would out-perform an actively managed group of high-cost hedge funds over a ten-year period from 2008 to 2017, when performance is measured on a basis net of fees, costs, and all expenses.

Posted by at 6:17 AM

Labels: Forecasting Forum, Macro Demystified

Subscribe to: Posts