Showing posts with label Energy & Climate Change. Show all posts

Wednesday, November 3, 2021

The Climate Action Gender Gap

This week of the year 2021 is of prime significance for the world as leaders from across countries have gathered in Glasgow, Scotland for the CoP26 summit which is touted to be the biggest environment-based conference after the Paris Summit in 2015.

Besides the heads of states, more than a fifth of the major corporations in the world have pledged to reach the net-zero carbon emissions target by 2030. However, what is striking is how the role of women as climate leaders, investors, and influencers is largely missing from the mainstream discussion on emissions reduction.

This report draws out interesting parallels between seemingly disparate objectives like climate change and diversity, that corporations must address as part of their journey towards a greener planet. It highlights the influence of greater gender equality on an enterprise’s climate outcomes, by having women in leadership positions to act as changemakers, as low-carbon product influencers, and climate-focused business investors.

Click here to read the full report.

This week of the year 2021 is of prime significance for the world as leaders from across countries have gathered in Glasgow, Scotland for the CoP26 summit which is touted to be the biggest environment-based conference after the Paris Summit in 2015.

Besides the heads of states, more than a fifth of the major corporations in the world have pledged to reach the net-zero carbon emissions target by 2030. However, what is striking is how the role of women as climate leaders,

Posted by at 1:36 PM

Labels: Energy & Climate Change, Inclusive Growth

Monday, March 2, 2020

Transitory and Permanent Shocks in the Global Market for Crude Oil

From a new IMF working paper by Nooman Rebei and Rashid Sbia:

“This paper documents the determinants of real oil price in the global market based on SVAR model embedding transitory and permanent shocks on oil demand and supply as well as speculative disturbances. We find evidence of significant differences in the propagation mechanisms of transitory versus permanent shocks, pointing to the importance of disentangling their distinct effects. Permanent supply disruptions turn out to be a bigger factor in historical oil price movements during the most recent decades, while speculative shocks became less influential.”

From a new IMF working paper by Nooman Rebei and Rashid Sbia:

“This paper documents the determinants of real oil price in the global market based on SVAR model embedding transitory and permanent shocks on oil demand and supply as well as speculative disturbances. We find evidence of significant differences in the propagation mechanisms of transitory versus permanent shocks, pointing to the importance of disentangling their distinct effects. Permanent supply disruptions turn out to be a bigger factor in historical oil price movements during the most recent decades,

Posted by at 10:24 AM

Labels: Energy & Climate Change

Wednesday, February 12, 2020

A just transition must help those struggling to heat their homes

From Social Europe post by Monique Goyens:

“In the latest contribution to our series on ‘just transition’, Monique Goyens argues that it must address the people finding it hard to pay their energy bills.

The task of moving to a carbon-neutral society is herculean, but the benefits won’t just include saving the planet. There are also long-term economic gains, even for the most hard-up.

An estimated 50 million around the European Union struggle to keep their homes warm and pay their energy bills. Many suffer from the same problems: poorly insulated homes, ill-suited tariffs, insufficient advice on how to save energy or a combination of all three.

The lowest income earners in the EU spend an increasingly large share of their budget on energy—rising from 6 per cent in 2000 to 9 per cent in 2014. In the short term, for this group, it makes more sense to use energy more efficiently than to invest in solar panels, heat pumps or pellet stoves. It will also deliver faster savings.

The choice should not however be between having a warm home and having food on the table. In making their homes more efficient, people consume less energy to heat their living space and can more easily pay their bills.

But getting people to take action can be complex. Those at risk of energy poverty might feel overwhelmed and prioritise solving other problems, such as warmer clothing or food. Often, they might not know what solutions are out there.

For governments and energy advisers to upload advice about insulation to a website isn’t enough. That advice needs to get out to people. Human contact also helps.”

Continue reading here.

From Social Europe post by Monique Goyens:

“In the latest contribution to our series on ‘just transition’, Monique Goyens argues that it must address the people finding it hard to pay their energy bills.

The task of moving to a carbon-neutral society is herculean, but the benefits won’t just include saving the planet. There are also long-term economic gains, even for the most hard-up.

Posted by at 10:42 AM

Labels: Energy & Climate Change, Global Housing Watch, Inclusive Growth

Monday, February 3, 2020

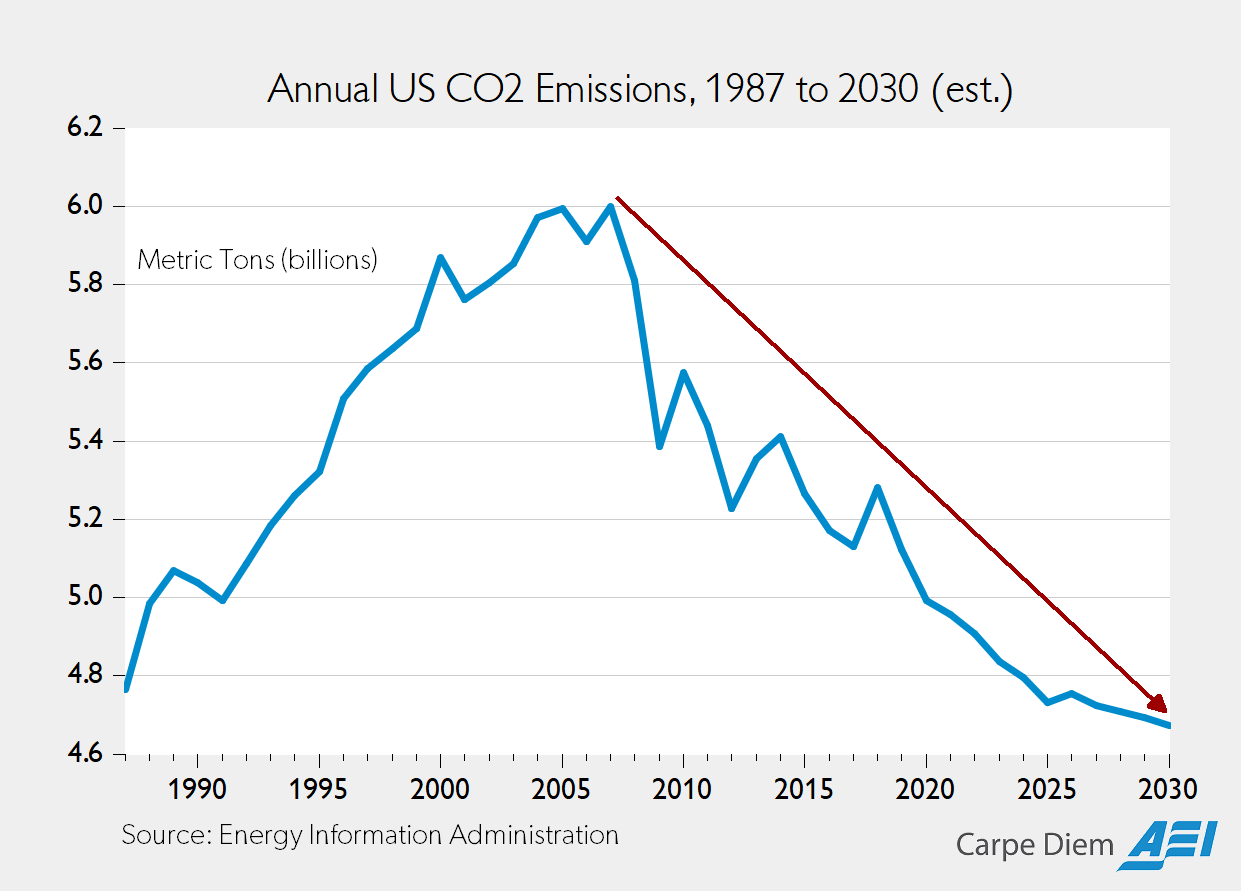

Annual US CO2 Emissions, 1987 to 2030 (est.)

Posted by at 11:17 AM

Labels: Energy & Climate Change

Wednesday, January 15, 2020

Central Banks and Climate Change

From a new VoxEU post:

“Central banks have been called on to contribute to fighting climate change. This column presents a framework for thinking about the issue and identifies some major trade-offs and choices. It argues that climate should be a major part of risk assessments and that capital ratios could be used in a proactive way by applying favourable regimes to ‘green’ loans and investments. It also suggests that central banks may want to take several climate change-related aspects into account when designing and implementing monetary policies. However, the central bank should retain absolute discretion to interrupt any action if its first-priority objective – price stability – were to be compromised.”

“The big question, however, is whether central banks can use their monetary instruments to actively promote the fight against climate change (Honohan 2019). Over the last decade, central banks have significantly expanded their balance sheets, often by a factor of five or ten. In many countries, those balance sheets are now commensurate to the size of the national economy. With such an imprint on the economy and financial markets, central banks could take a more proactive approach to financing the climate transition.

Two possibilities come to mind, both without significant changes to the current operational framework:

- Reorient their asset purchases towards ‘green’ securities

- Modulate haircuts applied to different kinds of collateral used in refinancing operations, thus creating an incentive to detain some and offload others. “

From a new VoxEU post:

“Central banks have been called on to contribute to fighting climate change. This column presents a framework for thinking about the issue and identifies some major trade-offs and choices. It argues that climate should be a major part of risk assessments and that capital ratios could be used in a proactive way by applying favourable regimes to ‘green’ loans and investments. It also suggests that central banks may want to take several climate change-related aspects into account when designing and implementing monetary policies.

Posted by at 1:25 PM

Labels: Energy & Climate Change

Subscribe to: Posts