Thursday, December 15, 2022

Housing Market Stability and Affordability in Asia-Pacific

From a new IMF Departmental Paper:

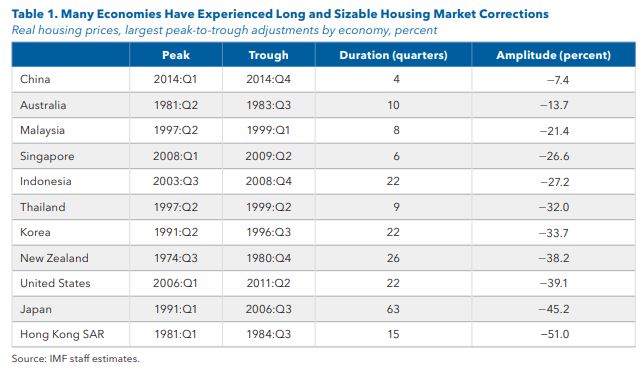

“Housing markets in the Asia-Pacific region are at an important juncture. Having risen over the past decade and during the pandemic, housing prices now appear slated for a decline in many countries. Pronounced housing cycles, which Asia-Pacific has experienced repeatedly also in the past, come at a cost. The buildup of vulnerabilities in the upswing tends to come to the fore during downturns, often with marked impacts on the broader economy. High housing prices and the prospect of increasing mortgage rates, as central banks tighten monetary policy, also imply a significant deterioration in housing affordability.

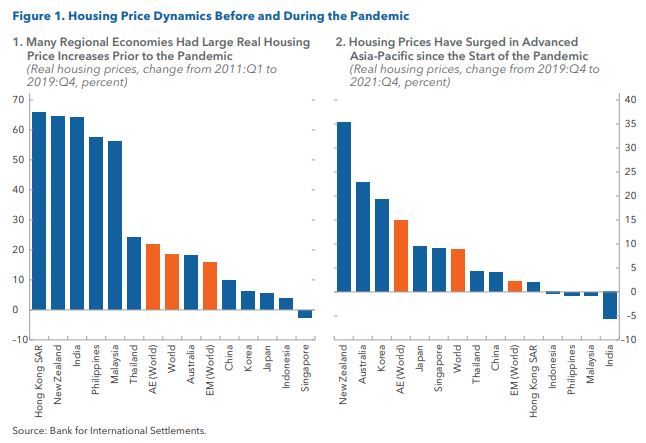

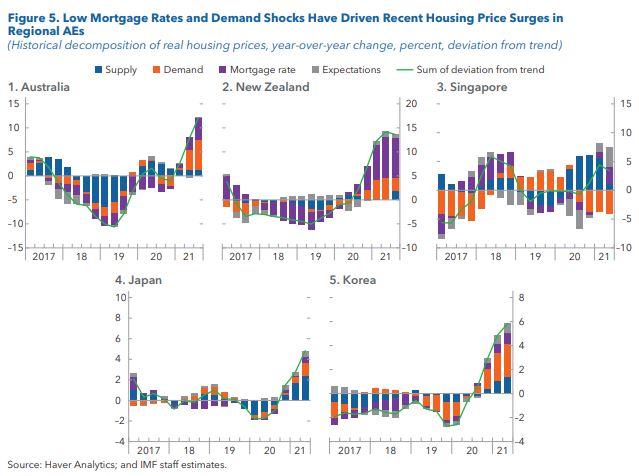

Housing prices in many countries across the region now appear misaligned, with significant downside risk to prices in the period ahead. Price surges during the pandemic, especially in the region’s advanced economies (AEs), were facilitated by low mortgage rates as central banks implemented very accommodative policy stances, along with country-specific demand and supply factors. This led to sizable price misalignment and a marked increase in downside risks to housing prices going forward, in the order of 5-20 percent in some countries. Rising interest rates will add to downside risks going forward. While the financial sectors of major AEs and emerging market economies (EMs) appear sound and would be expected to remain resilient under such shocks, close supervision is warranted for early identification of any pockets of risk.

With higher housing prices, housing affordability has become an increasing concern in the aftermath of the pandemic. Especially in the AEs, households have to stretch their wallets to be able to finance adequate housing, with an increasing share of them now overburdened by that cost. Adequate housing in many emerging market and developing economies (EMDEs) is also less affordable due to high housing prices, reflective of supply being unable to catch up with the rising demand of quickly growing populations. Poorer households in these countries are disproportionately affected.

To address the housing cycle and safeguard financial stability, macroprudential policies should be the first

line of defense. Countries in the Asia-Pacific region by now have a broad toolkit at their disposal, and policies have proven effective at mitigating housing credit growth during upswings. Within the toolkit, demand-side measures, such as loan to value (LTV) and debt service to total income (DSTI) limits, have been more effective than capital-based tools, and the effect of policy tightening during upswings has been generally stronger than stimulatory effects of policy loosening during downturns. While macroprudential measures have been effective at targeting household credit growth, they only have a limited effect on housing prices on average, and only significantly so in regional EMs. Leakages of macroprudential measures are also of concern, and policymakers should widen the regulatory perimeter where needed.

Improving housing affordability requires a multi-faceted policy approach. Facilitating a stronger supply

response will be key in many countries to address underlying imbalances. This includes reviewing land

use regulations, increasing the focus on urban planning, incentivizing the use of idle land, and providing

adequate social and affordable housing, both directly by the public sector and indirectly through incentives for private developers. But supply-side measures often take significant time to produce results, putting a premium on demand-side measures, which work more quickly. Such measures can include targeted government support, progressive taxation on property, targeted macroprudential policy to contain systemic risks while being mindful of its repercussions on lower-income households and owner-occupiers, and making use of targeted financing, insurance, and guarantee mechanisms.”

Posted by at 6:32 AM

Labels: Global Housing Watch

Subscribe to: Posts