Friday, December 9, 2022

House Prices in Canada

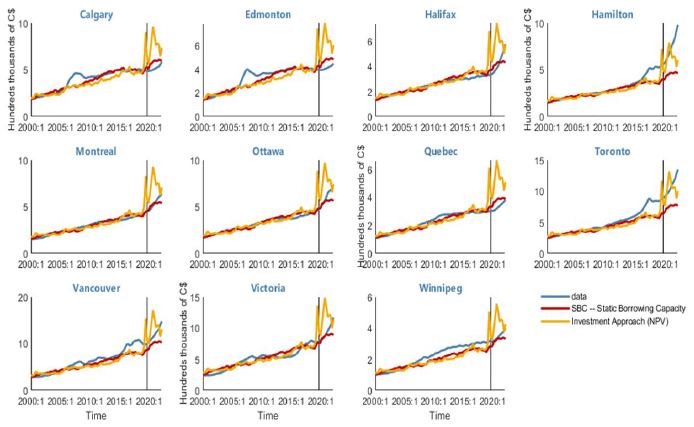

From the IMF’s latest report on Canada:

“The sharp increase in Canadian house prices, particularly during the pandemic, naturally raises the question of whether an asset price bubble was forming, or whether fundamentals explained most or all of the price run-up. Extending the analysis in Andrle and Plašil (2019), standard mortgage affordability formulas were used to link interest rates, income growth, and other household fundamentals to so-called “attainable” house prices in eleven Census Metropolitan Areas (CMAs) across Canada.

Staff analysis shows that in most locations—with the notable exceptions of Toronto and Hamilton—the change in house prices through the first half of 2021 was fully explained by households’ expanded borrowing capacity (which was driven by historically low mortgage rates and growing income). From mid-2021 onward, however, the growth in house prices in most CMAs exceeded the growth in attainable prices, suggesting some frothiness.

Even the apparent frothiness of the past eighteen months, however, is explainable if one considers

the perspective of investors. For investors, low interest rates, the expectation of economic recovery, and

broadly unchanged long-term growth expectations made prospective real estate cash flows more valuable than for the average owner-occupier. The “r-g” differential returned to its 2019 lows, and in most CMAs, the investor-implied valuation of the median house exceeded observed prices. In other words, buying real estate even at prices the median owner-occupier could not afford would still be consistent with achieving the required return on investment.

Looking forward, the projected rise in interest rates from their lows could drag attainable prices

down over 20 percent from their peak. And should regional overvaluations shrink at the same time, the

drop in actual prices could be substantially higher than this.”

Posted by at 6:02 AM

Labels: Global Housing Watch

Subscribe to: Posts