Sunday, July 31, 2022

The Upside-Down Housing Market

From Joseph Politano (Apricitas Economics):

“America has an acute shortage of housing. Its largest and most prosperous cities impede, restrict, or forbid large amounts of construction, and since the Great Recession output of suburban single-family homes has remained depressed. Real rents increased at the fastest pace in history during the late 2010s, housing vacancy rates remain near historic lows, and record numbers of young Americans live with their parents due to housing unaffordability.

For the better part of the that last decade, home prices in America have been on a slow march upwards as higher wages and employment levels mixed with structural under-construction. The pandemic sent the housing market into overdrive—work from home supercharged demand for residential living spaces, changing migration patterns upended local housing markets, lower mortgage rates pushed up prices, and supply-chain issues impeded construction projects.

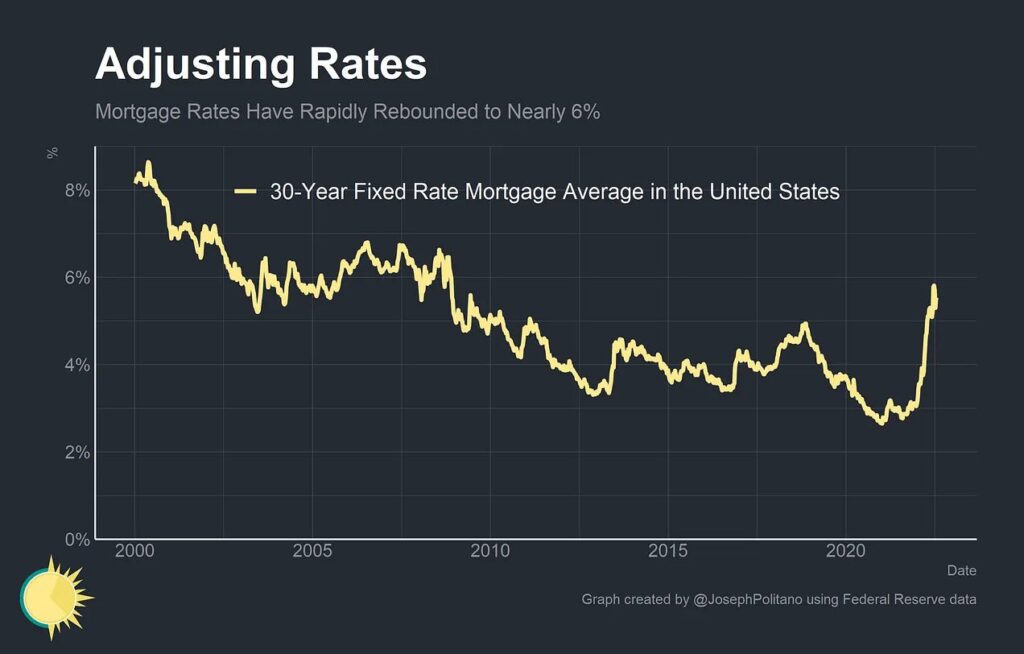

Now, the focus of the Federal Reserve is on constraining credit in order to combat inflation. That’s manifested in higher interest rates across the curve, including higher mortgage rates. In fact, mortgage rates are now higher than at any point since 2010, though they have pulled back a bit from their recent jump to almost 6%. Those higher mortgage rates are turning the housing market upside down—dropping mortgage applications, pulling down homebuilder sentiment, weighing on prices, and crushing housing starts. This mixture of higher rates, strong employment and wage growth, and supply deficiencies is unprecedented in the American housing market.

Mortgage Market Mayhem

Critically, the movements in mortgage rates are unique in modern American history for both their size and speed. After hitting an all time low of 2.6% in early 2021, the average 30-year fixed mortgage rate surged to 5.8% by January 2022 before sliding back to their current levels. Still, the last time mortgage rates were this high was late 2008.”

Continue reading here.

Posted by at 7:27 AM

Labels: Global Housing Watch

Subscribe to: Posts