Friday, July 22, 2022

Housing Market in Singapore

From the IMF’s latest report on Singapore:

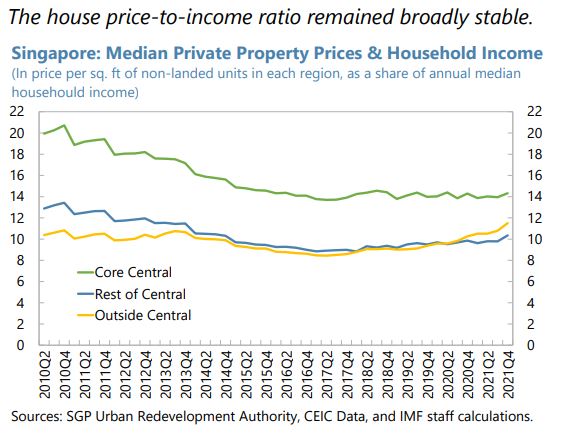

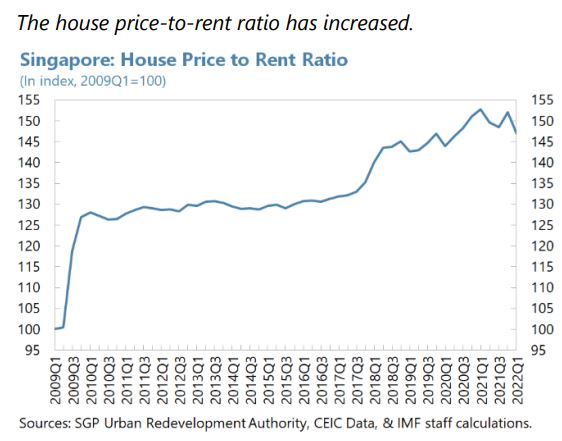

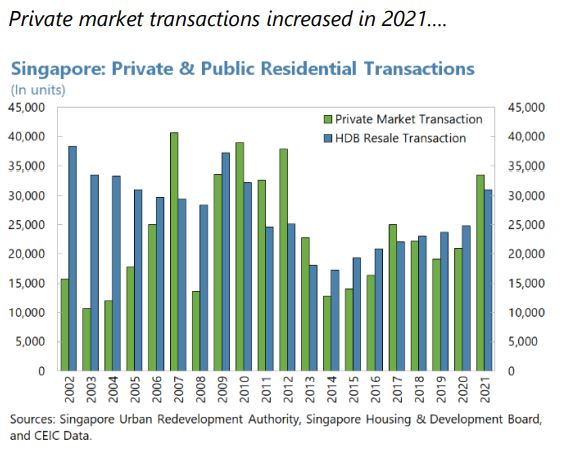

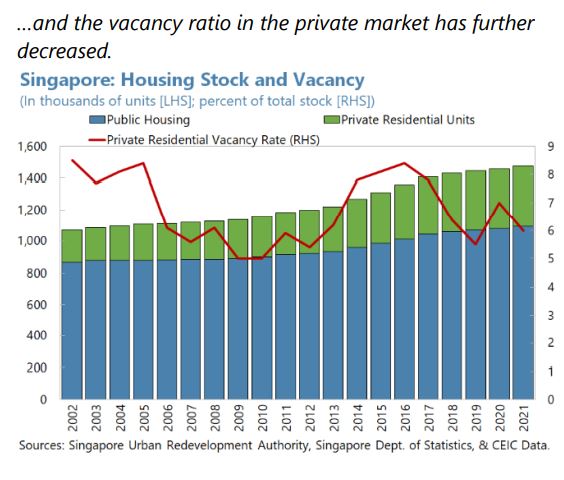

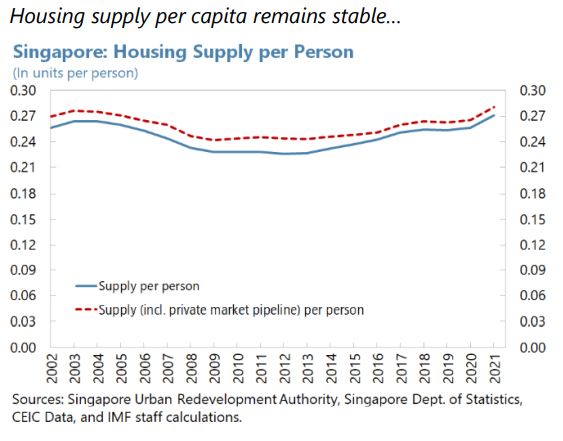

“Driven by strong demand, the private residential housing market runs the risk of diverging further from fundamentals, while commercial real estate is recovering following a few slow years due to the pandemic. House price inflation exceeding pre-COVID trends reflects strong dwelling demand driven by a shift to working from home, changes in domestic household formation with more single home households, increase in foreign demand, low real lending rates and constrained supply exacerbated by the pandemic. Some moderation in price growth occurred during the first quarter of 2022 (…). At close to 90 percent, Singapore already has one of the highest home ownership rates, implying that housing demand is principally being driven by non-residents and resident search for yield activity. Staff analysis suggests that private residential house prices are currently above long-term fundamentals. 13,14 Following a sharp decline in prices in 2020, commercial real estate showed signs of recovery in 2021, with prime office rents rising. However, prices in this segment remain below their pre-pandemic levels.

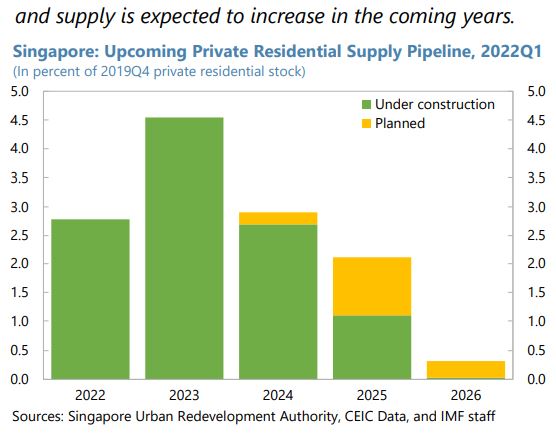

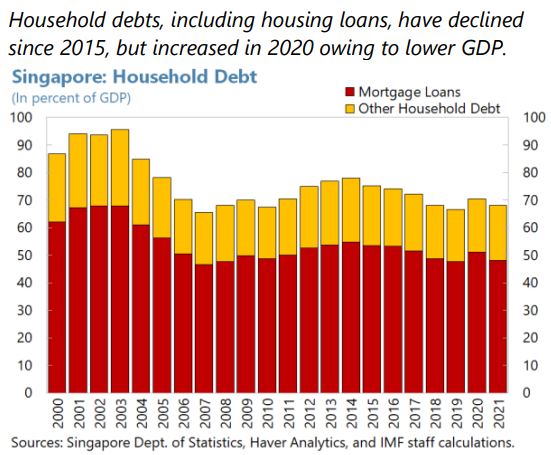

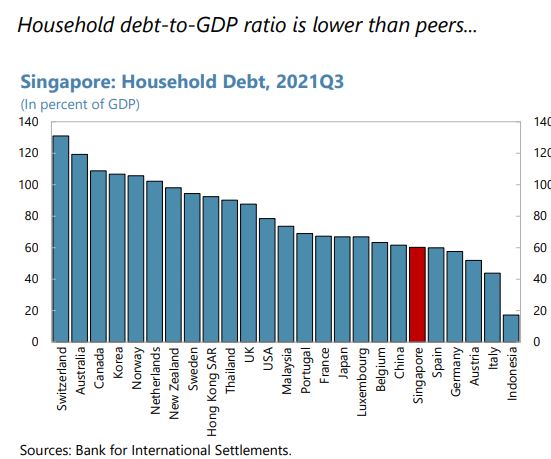

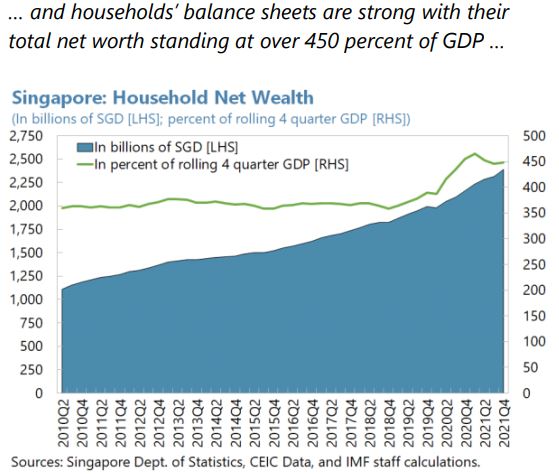

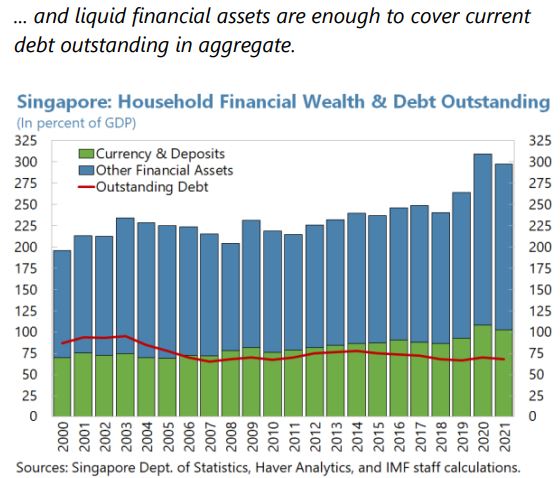

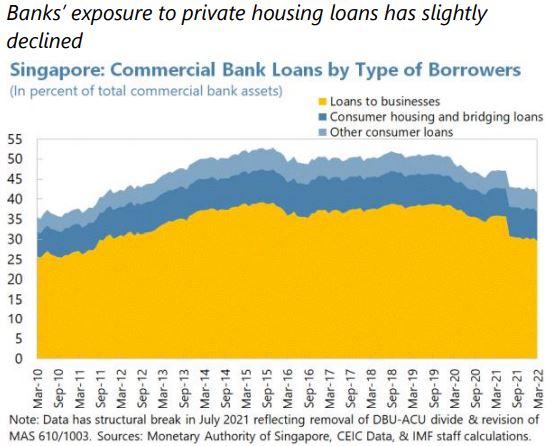

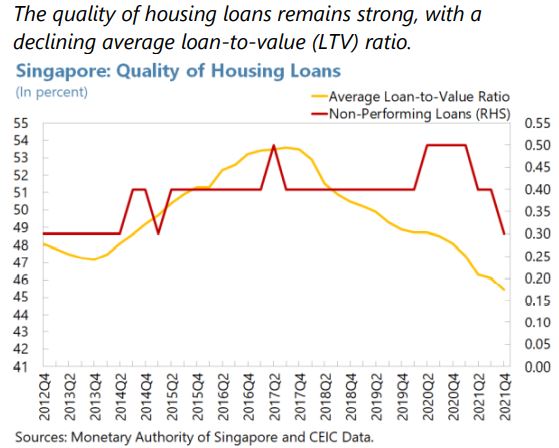

The authorities recently tightened macroprudential measures to cool buoyancy in private and public residential real estate markets, complemented by supply-side measures. Systemic risk is elevated but centered mostly in private residential real estate markets, with key macro-financial transmission channels operating through: (i) an elevated level of household debt, which peaked at 71 percent of GDP during the pandemic, about three quarters of which is secured against real estate; (ii) a high share of mortgages with fixed rates for 3 years or less before transitioning to floating rates; (iii) strong foreign demand sustaining private residential valuations; and (iv) property market related loans representing a third of banks’ total loans by end-2021. Stable average LTV and DS ratios, normally based on conservative interest rate assumptions, are mitigating factors. Recent measures to moderate residential property prices included (i) raising the Additional Buyer’s Stamp Duty (ABSD) rates (text table), (ii) tightening the total debt servicing ratio (TDSR) from 60 to 55 percent, and (iii) tightening the loan to value (LTV) limit for loans from HDB from 90 to 85 percent to encourage greater financial prudence. Based on MAS’ estimates, the resident credit-to-GDP gap was 10.6 percent in Q1 2021 but has since moderated to 0 percent. The authorities have also issued advisories urging prudence in new loan origination, particularly for property purchases. These and other measures complement plans to raise the supply of public and private housing with the Housing and Development Board targeting to raise public flat supply by 35 percent in 2022 and 2023.”

Posted by at 8:14 AM

Labels: Global Housing Watch

Subscribe to: Posts