Wednesday, June 8, 2022

Vulnerabilities in the housing sector from rising mortgage rates

From the OECD’s latest Economic Outlook:

“House prices, along with household debt, rose steadily throughout the pandemic, even in countries in which valuations were already stretched and debt levels already high. With monetary policy now beginning to normalise, mortgage rates are increasing in many OECD countries, raising solvency concerns. However, vulnerabilities appear contained at present due to households’ relatively strong balance sheets and the limited use of adjustable-rate mortgages (ARM). Still, fragile borrowers could be at risk in economies where ARM dominate, debt-service ratios are high and monetary policy is likely to tighten substantially. The potential adverse consequences for households and financial system resilience of a sharper-than-expected house price reversal also need to be prevented, primarily by macroprudential policy tools.

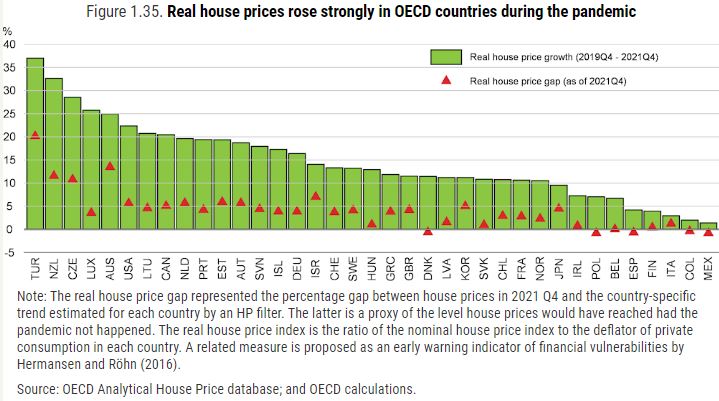

The pandemic pushed house prices to new heights in many countries

House prices rose strongly and quickly in most OECD countries during the pandemic. Between the fourth quarter of 2019 and the fourth quarter of 2021, real house prices rose by 13% in the median OECD economy (Figure 1.35). On average across countries, real house prices in the fourth quarter of 2021 were about 4% higher than expected based on the underlying trend prevailing before the COVID-19 pandemic, suggesting that the pandemic has exacerbated pre-existing tensions in many housing markets. A range of factors can explain this strong and synchronised response of house prices. Exceptionally accommodative monetary conditions, a surge in household savings and unprecedented fiscal support all boosted housing demand during the pandemic, with housing supply temporarily curtailed by mobility restrictions and logistical bottlenecks. Higher financing costs should moderate future housing demand, helping the rise in house prices to abate. A slowdown is already taking place in several key markets, such as the United States, with home sales and prices stabilising or even declining in some large cities, due to rising mortgage rates.

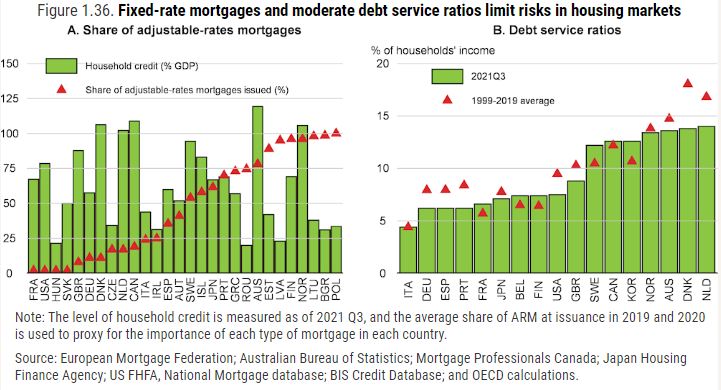

Fixed-rate loans dominate the mortgage landscape

The exposure of households to rising mortgage rates will be damped by the limited use of flexible or adjustable rate mortgages (ARM) in many OECD countries (Figure 1.36, Panel A), although there are also differences across countries in the typical period for which interest rates are fixed (van Hoenselaar et al., 2021). With the exception of Japan and, to some extent, Spain, the largest mortgage markets in advanced economies are heavily dominated by fixed-rate mortgages. In contrast, ARM contracts, which have been shown to be associated with a higher probability of default on mortgages when interest rate rise (Gross et al., 2022), are prevalent in several countries in Southern (Portugal and Greece), Eastern (Poland, Bulgaria, Romania and the Baltics) and Northern Europe (Sweden, Finland and Norway). If monetary policy normalisation proceeds gradually, borrowers should be protected from a sharp increase in financing costs over the medium term. Financially fragile borrowers in countries with independent monetary policies and rising inflation pressures could nonetheless experience a substantial rise in their debt servicing costs, particularly in countries where the ratio of mortgage costs to disposable income is already high for the lowest income quintile (van Hoenselaar et al., 2021).

Households’ savings are high and debt service ratios are still low

Household balance sheets are currently stronger than before the global financial crisis (GFC) in many countries. Stronger regulation in the aftermath of the GFC has limited the amount of risk-taking in the household sector over the last decade. In addition, the recent rise in household debt has been matched by a significant rise in household savings during the pandemic. These savings should support the repayment capacity of many households exposed to adjustable rates, especially if interest rates were to increase more rapidly than expected. Moreover, the low interest rate environment is still keeping average debt service ratios (DSR) in the household sector close or even below their long-term norms (Figure 1.36, Panel B), and significantly below what is considered a stressed DSR. However, aggregate numbers might conceal important heterogeneity, and risks remain that the repayment capacity of low-income borrowers could deteriorate, given the withdrawal of pandemic income support measures and higher inflation.

Macroprudential policies could be strengthened further

Real estate prices might adjust more abruptly. A sharp deterioration in the growth outlook, or a sudden increase in inflationary pressures, could accelerate a correction in housing markets, with potentially damaging consequences for households’ and banks’ balance sheets. Given the large uncertainty surrounding the outlook, it is critical that there are adequate buffers in the banking sector to ensure resilience to unexpected fluctuations in property markets.

Most countries already have policies in place to limit over-indebtedness and associated risks. Following ESRB recommendations (ESRB, 2022), many European countries have recently announced increases in their countercyclical buffer (CCyB) after some relaxation during the pandemic, including some measures explicitly targeting risks in the real estate sector. For instance, Germany’s financial regulator, BaFin, proposed in January 2022 to (i) raise the countercyclical buffer on banks’ domestic exposures to 0.75% of risk-weighted assets (RWAs) from 0% and (ii) to apply an additional systemic risk buffer of 2% of RWAs specifically targeted at residential real estate mortgage loans.

Preventive measures to limit further price increases, such as additional steps to lower LTVs or DSTI ratios, might also be welcome to moderate risks. Some countries have already taken steps to tighten existing tools to moderate new housing loans, while others could consider implementing those tools. In addition to these macroprudential instruments, reforms in rental regulation and property taxation may also be effective means of addressing housing pressures over time. Those tools, along with stronger public investment in social housing and potential land use reforms, especially in job-rich urban areas, could ease the tensions that are still likely to prevail in the medium term (OECD, 2021b). Although the supply of new construction slowed down only moderately during the pandemic, new housing permits and starts dropped significantly in many OECD countries. This gap, along with ongoing supply bottlenecks and labour shortages, is likely to amplify the structural housing shortages affecting many countries.”

Posted by at 7:34 AM

Labels: Global Housing Watch

Subscribe to: Posts