Thursday, June 30, 2022

Housing Market in Slovak Republic

From the IMF’s latest report on Slovak Republic:

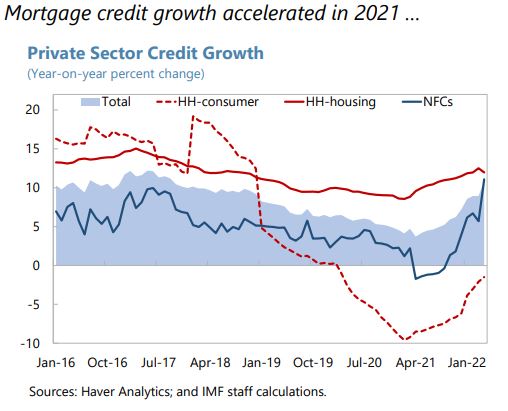

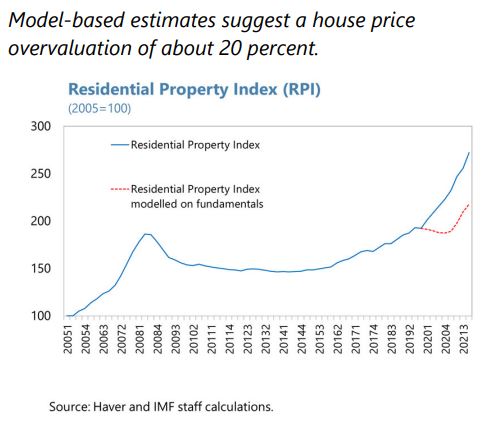

“House price growth has continued to accelerate amid rapid mortgage credit growth, driven by record low borrowing costs and looser credit standards. House price growth increased throughout 2021, reaching 22 percent y/y in 2022:Q1, with a wide gap between actual and model-predicted house prices. While housing affordability (as captured by the share of disposable income taken up by mortgage payments) remained quite high until mid-2021 given low interest rates and robust wage growth, and housing cost overburden for lower-income households is moderate from an international perspective, tightening financial conditions and higher inflation could quickly change this.

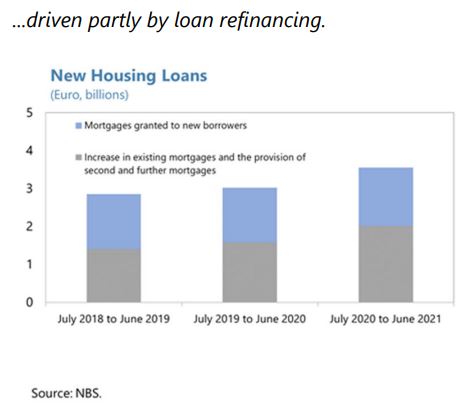

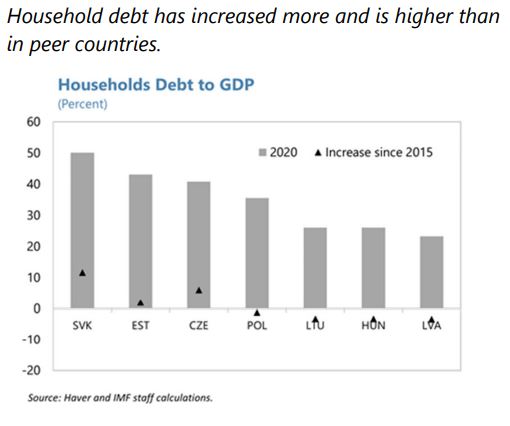

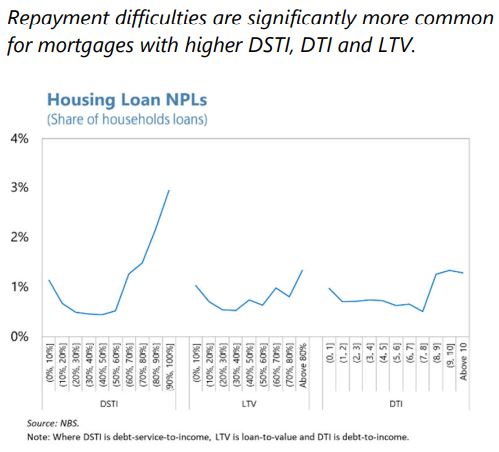

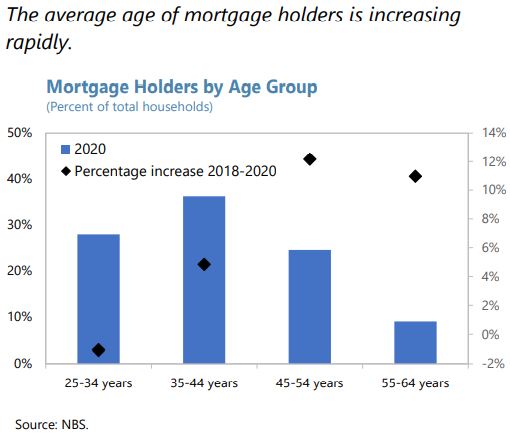

Macrofinancial vulnerabilities related to the housing market warrant close monitoring. Household debt relative to GDP has risen faster and is higher than in peer countries, due to the increase in homeowners with mortgages and the topping-up of existing mortgages. The active use of borrower-based measures has reduced the share of high LTV, DTI, and DSTI mortgages, but the cluster of mortgages right below regulatory limits is a potential source of vulnerability.16 There has also been an increase in mortgages with maturities extending beyond borrowers’ retirement age.

While the macroprudential stance is broadly adequate from a financial stability point of view, the authorities could consider introducing additional macroprudential policy measures to address housing market vulnerabilities if imbalances persist.17 As recommended in the 2021 IMF Staff Report and the ESRB, the NBS could consider introducing capital-based measures on mortgage exposures, including minimum risk weights, to strengthen banks’ resilience to adverse housing market shocks. The NBS could also explore applying the sectoral systemic risk buffer (SyRB) to target systemic risks from mortgage loans under the new Capital Requirements Directive (CRD V) flexibility, after conducting a cost-benefit analysis. To address pockets of vulnerability, such as the concentration of loans below regulatory limits and the rise in loans with maturities beyond retirement age, the authorities could consider adjusting borrower-based measures. For example, additional amortization requirements for new mortgages at the regulatory ceilings could reduce their clustering right underneath those ceilings. The proposal of a gradually falling DTI limit as borrowers approach retirement age would help limit overindebtedness of vulnerable pensioners, though it will be important to monitor its implementation and ensure that it does not reduce excessively access to credit to potentially credit-worthy older borrowers.

Addressing housing supply shortages and reforming property taxation could help alleviate property market pressures. Over the past decade, the overcrowding rate in Slovakia has declined but remains significantly higher than the EU average, especially among the younger population.18 The inflow of refugees might also raise housing demand. Improving housing supply will have social benefits as well as dampen house price growth and associated vulnerabilities. In that regard, the recently approved construction and spatial planning laws, which aim to simplify the construction code, shorten the lengthy building permit process and reduce bureaucracy are welcome. Developing the rental market could also help contain house price inflation. Finally, raising Slovakia’s property taxes would strengthen public finances and dampen overheating pressures.

Authorities’ Views

The authorities broadly concurred with staff’s assessment of housing market risks. They are open to expanding their macroprudential toolkit with capital-based measures, such as minimum risk weights, but a thorough cost-benefit analysis would be needed, especially given the sizable differences in mortgage risk-weights among IRB banks. They plan to introduce age-related DTI limits to address the rise in mortgages with maturities extending beyond retirement age. Their analysis suggests that the early adoption of such a precautionary measure would help limit excessive indebtedness and reduce the accumulation of risks, with only a slight reduction of credit growth. They also highlighted recent regulatory changes to bolster housing supply flexibility.”

Posted by at 12:13 PM

Labels: Global Housing Watch

Subscribe to: Posts