Thursday, June 30, 2022

Housing Market in Portugal

From the IMF’s latest report on Portugal:

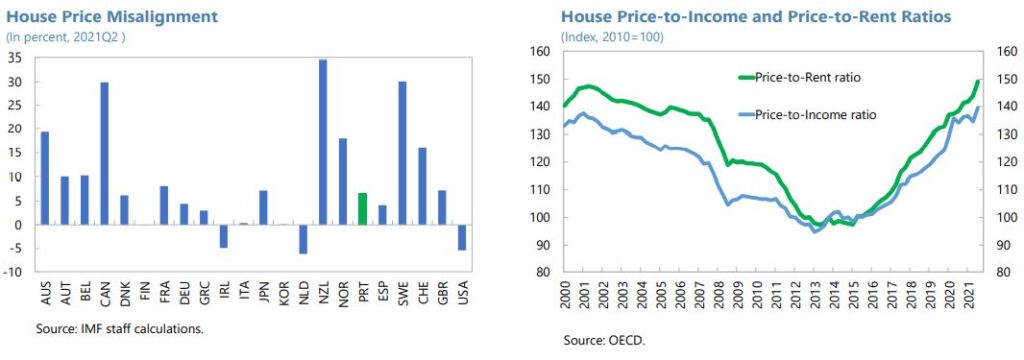

“Since 2015, Portuguese house price growth outpaced the EA average by almost 30 percentage points. This pace was sustained throughout the pandemic, with residential real estate prices gaining nearly 20 percentage points in real terms and relative to rents.

Available estimates suggest overvaluation of residential real estate. Based on indicators developed by the ECB, Banco de Portugal estimates point to an over-valuation of 8 to 16.5 percent (see Banco de Portugal, December 2021 Financial Stability Report). IMF model-based estimates of house price misalignments relative to fundamentals point to an overvaluation of 7 percent as of mid-2021. However, since mid-2021 house prices increased by 5.7 percent by end-2021. Price-to-rent and price-to income ratios have reached the highest levels since 2000.

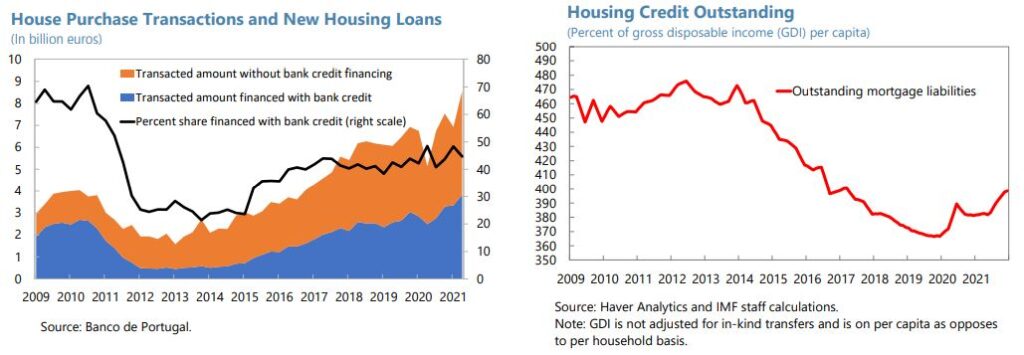

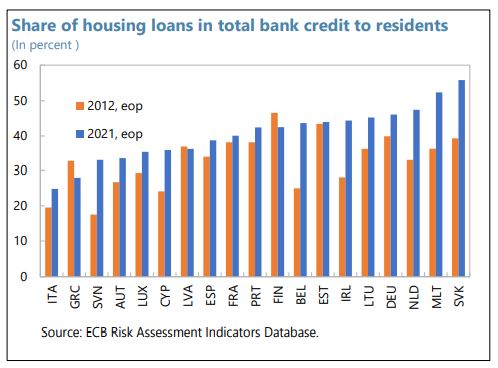

Domestic bank credit has not been a key driver of house prices yet. Even before the pandemic, Portugal had become one of EA’s most dynamic real estate markets partly reflecting tax incentives for foreigners and the Golden Visa program, whereby non-resident flows contributed to drive up housing prices. With households deleveraging since 2012–13, outstanding house credit to disposable incomes declined by 100 pp between 2014 and 2019. Housing credit growth turned positive only from 2019, driven by improved consumer confidence and low interest rates. While credit it still below historical averages, some estimates suggest small but positive credit gaps emerging in recent years. Housing supply shortages also played a role in boosting prices, with relatively subdued construction activity in the pre-pandemic years, although the construction sector remained resilient throughout the pandemic. Some cities (e.g., Lisbon) also saw a compression in price variation, with lower-end prices seeing steep gains.

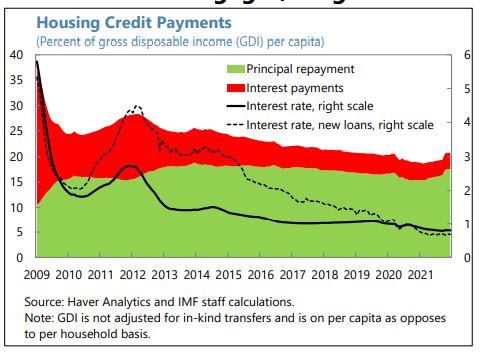

Although aggregate housing debt service as a share of disposable income was declining before the pandemic, this trend has slowed. On a per capita basis, average mortgage payments correspond to about 1/5th of household gross disposable income, marginally lower than the peak during the 2012–13 sovereign debt crisis. Also, mortgage interest payments declined from about 12 percent of disposable income in 2012H1 to about 3 percent in 2021. Principal repayments dipped temporarily due to moratoria.

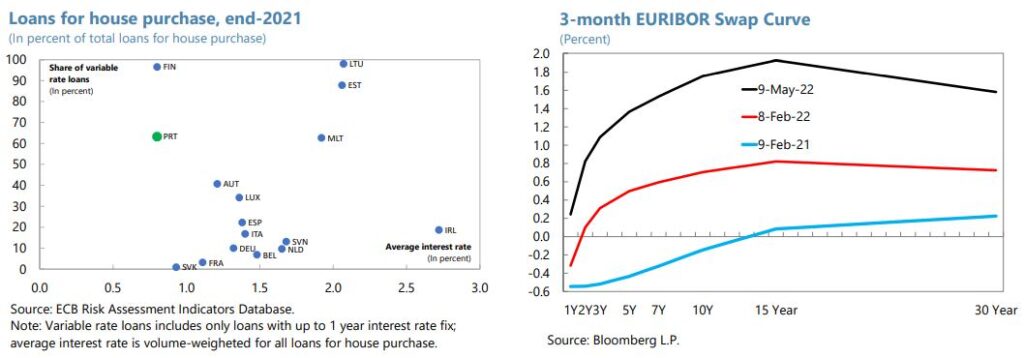

With house lending relying predominantly on variable rate mortgages, a significant increase in interest rates would quickly erode household incomes. Three quarters of housing loans have rate fixation of up to one year, with Euribor as the benchmark, while only a small fraction has fixed rates for longer than 10 years. Compared to early 2021, 2-year swap rates have widened by over 150 basis points reflecting expectations of ECB monetary tightening. With historic and euro-area’s lowest mortgage interest rates as of 2021Q4 – 0.7 percent for new mortgages and 0.8 percent for all outstanding –a 1 pp higher rate could raise household interest payments from 3.2 percent to about 7.2 percent of average household income, potentially also impacting aggregate demand. As per BdP’s borrower-based macroprudential policy measures, banks are recommended to consider a 300 basis point interest rate shock in the calculations of DSTIs for new mortgages.

The Bank of Portugal expanded its macroprudential toolkit in 2018, including measures on new credit agreements relating to residential property and consumer credit (also see Neugebauer and others 2021, Banco de Portugal Financial Stability Report, December 2021). Supervisory data indicate that borrower profiles improved in 2019, partly reflected in the increase in the share of mortgage credit granted to borrowers with net income above median. Nonetheless, the average maturity of new loans has not undergone gradual convergence towards 30 years, which prompted new macroprudential guidance from April 2022 on limits to maximum maturities. As regards the interest rate risk, and as mentioned above, the measures stipulate that banks should take into account the impact of higher interest rates in the calculations of DSTI, which is a mitigating factor. More generally, risks need to be closely monitored and consideration should be given on further strengthening capital positions, in accordance with the ESRB guidance, should vulnerabilities from the residential real estate sector continue increasing.

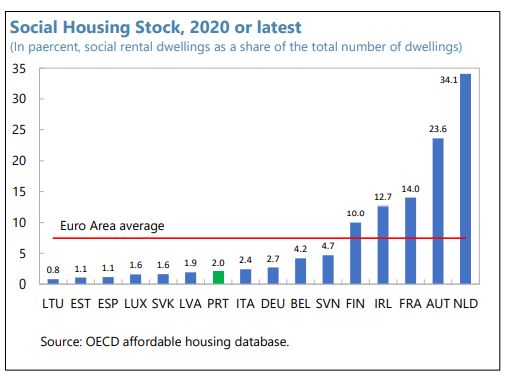

In view of rising house prices and limited social housing, housing affordability has also been a growing concern. House prices to disposable income are high among EA countries. Social housing is also limited, at about 2 percent of the total housing stock compared to EA average of 7.5 percent. In this context, the NGEU financed NRRP provides an opportunity for such investments to increase the stock of affordable rental housing for low-income families, which can also facilitate job mobility.”

Posted by at 12:37 PM

Labels: Global Housing Watch

Subscribe to: Posts