Friday, June 10, 2022

Housing Market in Canada

From the Bank of Canada:

“The vulnerability associated with elevated house prices (Vulnerability 2) increased further over the past year. Key developments in the housing market—strong demand relative to supply, driven partly by an increasing share of investors; prices reaching all-time highs in most regions; and expectations that these price increases will continue in most major cities—point to further imbalances in prices compared with a year ago.

A large misalignment of house prices relative to longer-term fundamentals could lead to an abrupt price correction in the future. Such a correction can, in turn, bring on financial stress for households because housing often represents their largest asset (see “A large decline in household income and house prices”).

It is too early to tell whether the recently observed decrease in resale activity and prices will be temporary or is the start of a deeper, lasting decline. A sudden reversal of the influx of housing investors seen during the pandemic could amplify downward pressure on prices (Box 2).

After months of exceptionally strong activity in the housing market, resales slowed considerably in March and April 2022 (Chart 7). Until the early months of 2022, demand—including from investors—was remarkably robust, supported by a desire for more housing space, record-low mortgage rates and the accumulation of extra savings. Resales are expected to soften as borrowing rates rise and the pandemic-induced demand for more housing space wanes. Recent monthly data reveal a large decline in resale activity. This could reflect a temporary echo effect from some homebuyers making their purchases earlier to avoid the latest mortgage rate increases, or it could signal the beginning of the end of the pandemic upswing.

Growth in house prices has been vigorous and regionally broad-based. In April 2022, house prices were up 24% nationally compared with April 2021, and up 53% relative to April 2020. Despite house prices increasing in nearly all areas, suburbs have experienced the strongest growth—as seen in the Toronto and Montréal regions (Figure 1).15 This dynamic is consistent with the pandemic-induced shift in preferences for more housing space, which is more affordable and widely available in suburban and rural areas than it is in city centres.

Part of the exceptional increase in house prices observed since the start of the pandemic may have reflected extrapolative price expectations. This happens when people come to expect that house prices will rise in the future simply because they have risen in the past. In such a situation, homebuyers may rush into the market out of fear of missing out or may hope to realize a sizable capital gain. Under these conditions, housing demand and prices can then become disconnected from underlying fundamentals, putting prices at risk of a correction in the future. Extrapolative expectations, particularly among investors, could amplify and accelerate price declines if a house price correction were to occur. Such a correction could dampen economic activity not only through confidence effects but also because it reduces household wealth and restricts access to credit (see “A large decline in household income and house prices”). Although house prices declined in April 2022, it is too early to tell whether this is the beginning of a substantial correction in prices.

Before the tightening of monetary policy in March, extrapolative expectations appeared to have broadened. The Canadian Survey of Consumer Expectations conducted in February revealed that many Canadians were expecting house prices to increase substantially over the next year. In fact, this is the highest rate for this response since the Bank introduced this survey question in 2016. These elevated expectations also appeared to be broadening. For the first time, the Bank’s House Price Exuberance Indicator characterized house prices in most major Canadian cities as exuberant in the first quarter of 2022 (Chart 8).16 However, these indicators were collected before the slowdown in housing activity and price growth in April. It remains to be seen whether data for the second quarter will support the same conclusion.

The share of Canadians buying homes as investment properties grew in 2021. The increased presence of investors in the real estate market can amplify the vulnerability associated with elevated house prices (Box 2).

Box 2: Vulnerabilities associated with investors in residential real estate

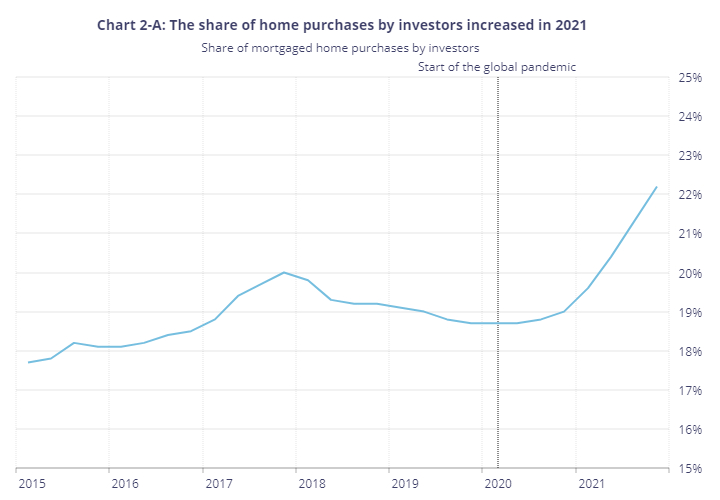

In an environment of low mortgage rates and rapid increases in house prices, expectations of a large capital gain can make houses an attractive asset for investors. For the purpose of this analysis, investors are defined as existing mortgage holders who obtain an additional mortgage to purchase a property. In 2021, they made purchases at a faster pace than first-time or repeat homebuyers. Investors accounted for over 22% of mortgaged purchases in the fourth quarter of 2021, up from 19% in 2019 (Chart 2-A).17

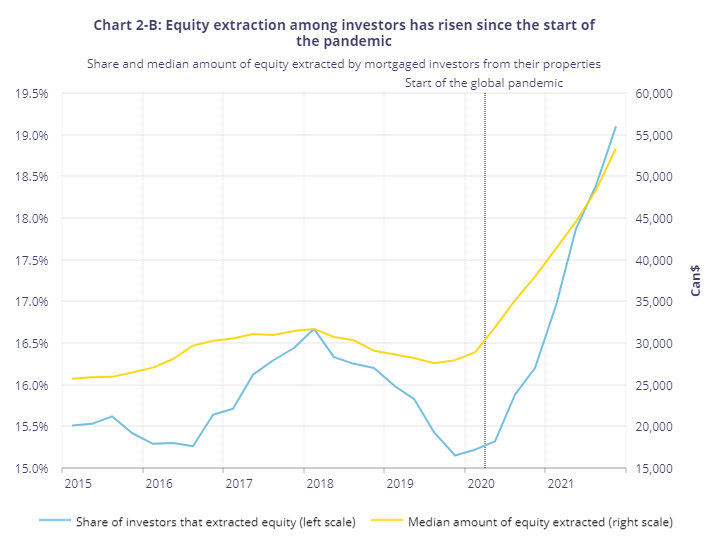

Investors are increasingly extracting equity from their existing properties to support new purchases. The share of investors who took out at least $5,000 in equity in the three months before they purchased an investment property rose substantially since the start of the pandemic (Chart 2-B). The amount of equity these investors took out through home equity lines of credit or mortgage refinancing also noticeably increased. For about one-third of these investors, the equity extracted was equal to or greater than the down payment on their subsequent purchase. This proportion is up from just over one-fifth in 2019. The increased use of equity gains to finance purchases highlights the feedback loop between rapid gains in house prices and the stronger demand for housing that investors generate.

Investors can amplify house price cycles. Investors can play an important role in the housing market if they make their property available to renters on a long-term basis. But investors can also increase vulnerabilities linked to higher house prices:18

- During housing booms, greater demand from investors can add to bidding pressures and intensify price increases.

- When prices are stable or declining or mortgage carrying costs are rising, holding real estate as an investment becomes less attractive. The incentive to sell may be greater for investors who risk falling into a negative equity position on one or more properties, also known as being “underwater.” A negative equity position can prevent the future sale of a property if the investor does not have enough liquid assets to cover the shortfall.

Although investors typically earn more income than non-investors, they tend to have higher loan-to-income ratios, once all the mortgages they hold are accounted for, and higher debt servicing costs.19, 20 If an income shock occurs—whether a reduction in employment or rental income because, for example, some tenants become unemployed—highly leveraged investors may need to sell one or more of their properties to recover some liquid assets. Although investors may not be considered as financially vulnerable as non-investor households given the amount of equity they have tied up in real estate, investors could intensify the effect of an economic slowdown by adding downward pressure on housing demand and prices.”

Posted by at 8:24 AM

Labels: Global Housing Watch

Subscribe to: Posts