Monday, December 6, 2021

Housing Market in Australia

From the IMF’s latest report on Australia:

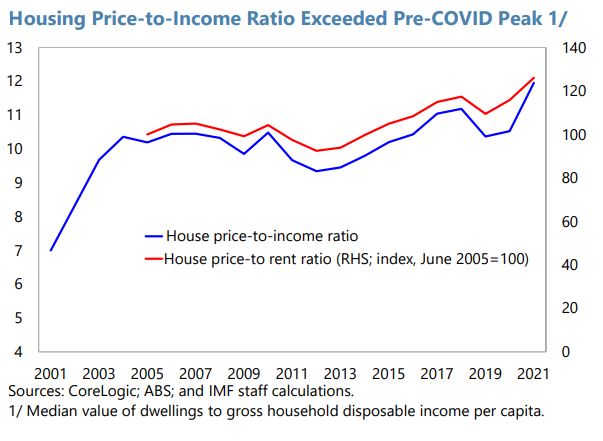

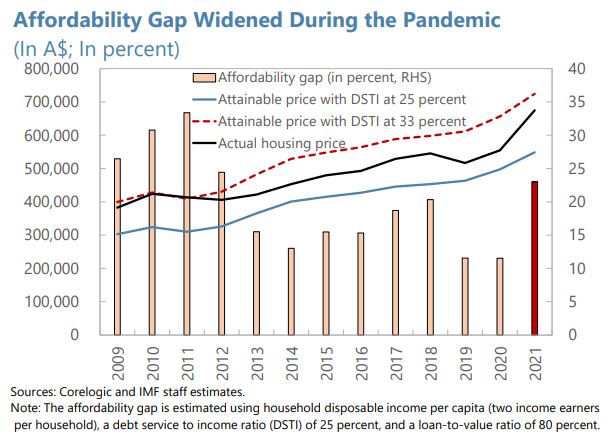

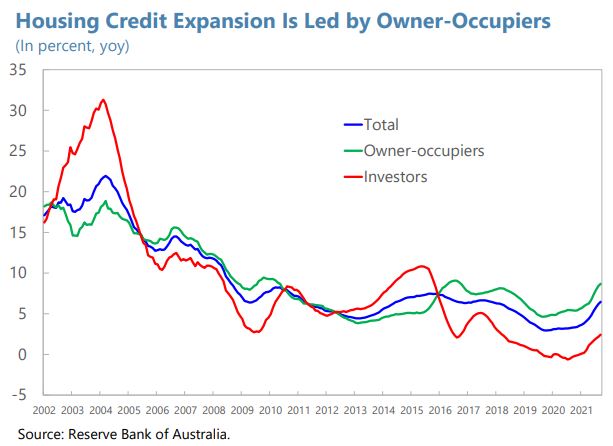

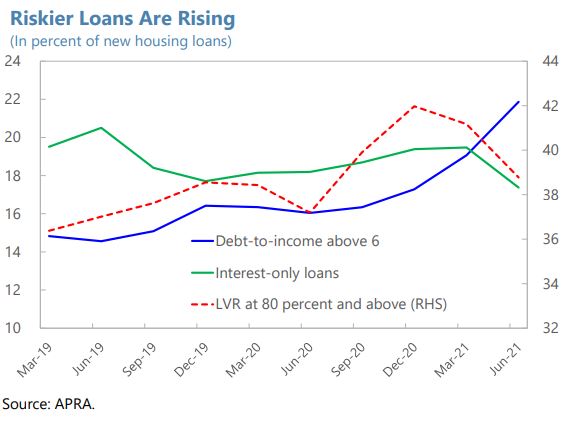

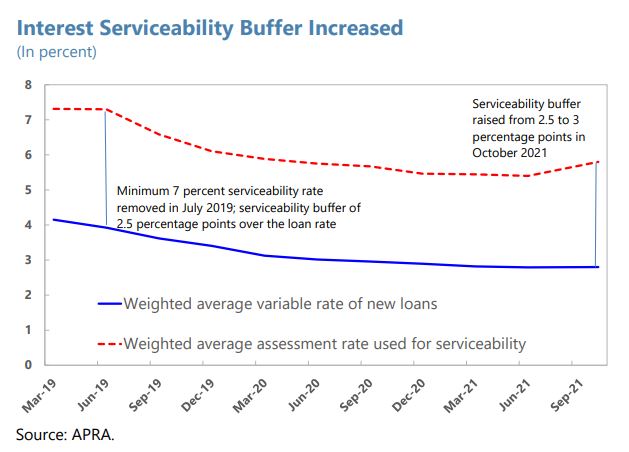

“Housing affordability has deteriorated, and financial risks are building. The housing price-to-income and price-to-rent ratios have risen and exceed pre-COVID peaks. The affordability gap has widened. Housing credit growth is accelerating, reaching 6.5 percent (y/y) in September, driven by owner-occupiers (8.7 percent), with investor loans picking up from a low base (2.4 percent). The risk profile of new loans is deteriorating, as the share of borrowers with high debt-to-income ratios surged from 16 percent pre-COVID to 22 percent.

Macroprudential policy has responded to the changing risk environment. In October 2021, APRA raised the minimum serviceability buffer from 2.5 to 3 percent, requiring lenders to use the higher interest rate spread in assessing borrowers’ ability to service their mortgage loans, thereby strengthening their repayment capacity in case of shocks, such as rising interest rates or income loss.

Staff’s Views

The recent tightening of macroprudential policy is appropriate, and additional measures should be considered if financial-stability risks continue rising. While the surge in house prices has been driven largely by owner-occupiers taking advantage of low mortgage rates and fiscal support programs, high debt-to-income mortgages are on the rise amid elevated household debt, and investor demand has begun to increase from low levels. Lending standards should be monitored closely. With about 70 percent of mortgages at variable rates, borrowers are exposed to rate increases with the expected monetary policy normalization in the medium term. Further macroprudential tightening may be warranted if housing debt continues to outpace income growth and the rise in housing prices leads to increased riskiness of mortgage lending. Options include instituting portfolio restrictions on debt-to-income (DTI) and loan-to-value ratios (LVR), with DTI restrictions likely more effective in curbing investor demand, while LVR restrictions would affect more liquidity-constrained owner-occupiers, in particular first home buyers.

Housing structural reforms are critical for supporting affordability. Supply-side reforms, including more efficient planning, zoning, and better infrastructure, could improve housing supply. Commonwealth and state/territory governments should consider providing more financial incentives for local governments to streamline zoning regulations and improve infrastructure. Promoting flexible work arrangements could allow workers to move away from capital cities, improving affordability. In addition, governments should focus on providing targeted fiscal support for low-income households and expand social housing. This could be complemented by tax reforms to discourage leveraged housing investment.

Authorities’ Views

The authorities stressed that rising risks in home lending motivated the recent macroprudential tightening. They noted that, while lending standards have generally remained prudent, rapid credit growth that outpaces household income growth could build financial vulnerabilities, while the strength of the house price cycle could give rise to more risk-taking and potential erosion of lending standards. They underscored that they would continue to closely monitor trends in residential mortgage lending and were prepared to take further measures if needed. They confirmed that other policy instruments, including DTI and LVR restrictions, could be deployed if necessary. The authorities thought that tax policy was not the right tool to address potential speculative behavior in housing markets, as negative gearing and the capital gains tax discount apply across investments and investments in residential housing are relatively highly taxed, and that macroprudential policy should instead be employed as needed to address financial stability risks.

The authorities agreed that housing supply reform would be important to improve affordability. They highlighted that the Commonwealth has provided funds to support state and local governments in infrastructure provision and concurred that more could be done to promote zoning and planning reforms to boost housing supply. Additional targeted support could also be provided to low-income households to address affordability issues, and the authorities concurred that adequate provision of social housing remained important.”

Posted by at 6:03 PM

Labels: Global Housing Watch

Subscribe to: Posts