Monday, April 6, 2020

Room to Grow: Housing for a New Economy

Global Housing Watch Newsletter: March 2020

* Below is a conference summary on the US housing market prepared by Enrique Martínez García (Federal Reserve Bank of Dallas). The event was co-sponsored by the Real Estate Center at Texas A&M University and the Federal Reserve Bank of Dallas. The views expressed in this summary are those of the author and do not necessarily reflect the views of the Federal Reserve Bank of Dallas or the Federal Reserve System.

A broad range of economists, industry analysts, and experts met for this pre-coronavirus-upheaval conference held in Dallas during much calmer times on February 21, 2020 to discuss the latest trends affecting the U.S. and Texas housing markets. The speakers talked extensively about demographic factors (the millennials generation) and the many ways in which technology is replacing face-to-face transactions and creating new ways to build, buy and sell, and finance a home (fintech).

Macro trends and housing

Keith Phillips (Federal Reserve Bank of Dallas) and James P. Gaines (Real Estate Center at Texas A&M University) showcased a number of macro challenges and their consequences for affordable housing. Mr. Phillips argued that economy is navigating in an increasingly more uncertain world whereby low long-term interest rates could well prove to be a coin with two faces: on the one hand, low rates support housing markets by making ‘cheaper’ while, on the other hand, the low levels of long-term rates relative to the short-term rates (yield curve inversion) are a powerful signal of the growing risk of recession which in turn is a drag on the housing sector.

Mr. Phillips also highlighted the key role that international oil markets play in the macro outlook and, in particular, on housing in Texas and even in the U.S. as a whole. He cautioned that a downward risk for the U.S., a major oil-producing economy, arises from the possibility that oil prices fell below current prices which at the time stood around $56 per barrel barely above the average break-even price for much of the oil industry in Texas and the rest of the U.S. (which according to the Federal Reserve Bank of Dallas’ Energy Survey ranges between $48 and $54 per barrel).

Frank Nothaft (CoreLogic) further added to this that uncertainty over the severity and length of the coronavirus (COVID-19) outbreak in Wuhan (China) was beginning to disrupt the global economy and cause growing concern. Trying to gauge the potential impact on housing, Mr. Nothaft showed evidence on different areas across the U.S. hit by natural disasters as a case study. He warned that the impact on housing markets that could be expected from similar disruptions could be quickly felt and severe. He also noted that such disruptions tend to be followed afterwards by a spike in common delinquencies and faster house price and rent growth. Little did Mr. Phillips and Mr. Nothaft know how prescient their remarks would turn out to be in just a matter of weeks.

The importance of knowing your customers (millennials)

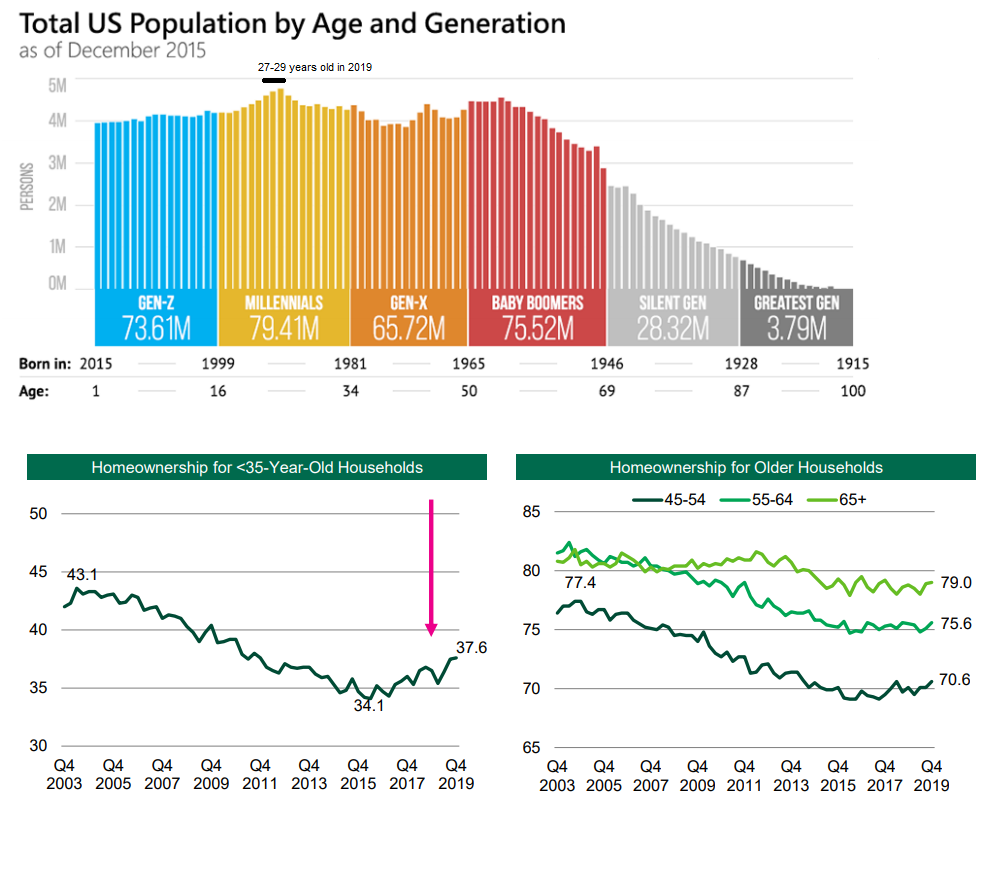

Mr. Gaines singled out two demographic trends in particular that, in his view, will likely upend housing markets for the next decade (at least): (a) housing supply continues to fall behind the demand because housing sales have yet to recover from the pre-2008 recession yet population projections anticipate more growth, and (b) the generational shift from generation X to the millennials is already impacting the why, when, and how to buy and sell a house. Mr. Gaines commented that the boom of 27-29 year-olds (see top plot in Figure 1) is also expected to boost housing demand in the next decade. Many other participants also noted in their remarks the challenges and opportunities for housing posed by the coming of age of millennials in the U.S. which became one of the central themes of the conference.

Echoing Mr. Gaines, Odeta Kushi (First American Financial Corp.) shared that First American’s own projections based on U.S. Census Bureau data suggest an increase in cumulative net new owner-occupied households among millennials in the U.S. (21-39 year-olds in 2019) of well over 15 million by 2040 relative to 2019 levels. Millenials are more educated than previous generations, but the millennials’ median income has only modestly outpaced that of the baby boomers and education itself is taking longer and adds the rising burden of student loans. According to Ms. Kushi, those are some of reasons why the rate of homeownership by age cohort is lower for millennials than it was for generation X or the baby boomers. She also indicated that household formation is crucial for housing—the first-time homebuyer market share is above 50% (at least since 2013)—and that average tenure length has gone up to 12 years (4 more years than in 2005), increasingly dependent on and a consequence of the choices made by millennials.

Jeanette I. Rice (CBRE) argued that, even when single-family is affordable, other aspects of the lifestyle of millennials are also affecting the trends and timing of household formation. Chief among them: (a) delayed “trigger points” for homebuying nowadays (getting married later at 28 for women and 30 for men, starting families later, and having fewer or no kids); and (b) renting is becoming more appealing to young professionals at the start of their careers in part because of the flexibility and ease of mobility from renter tenure. For Ms. Rice those lifestyle choices are contributing to delaying homeownership and continue to tilt the market towards renting multifamily housing. As a result, she concluded, multifamily remains strong and continues to attract a lot of attention and much domestic capital investment and even foreign investment (although foreign investment is mostly concentrated on the coasts and in Austin and Houston within Texas).

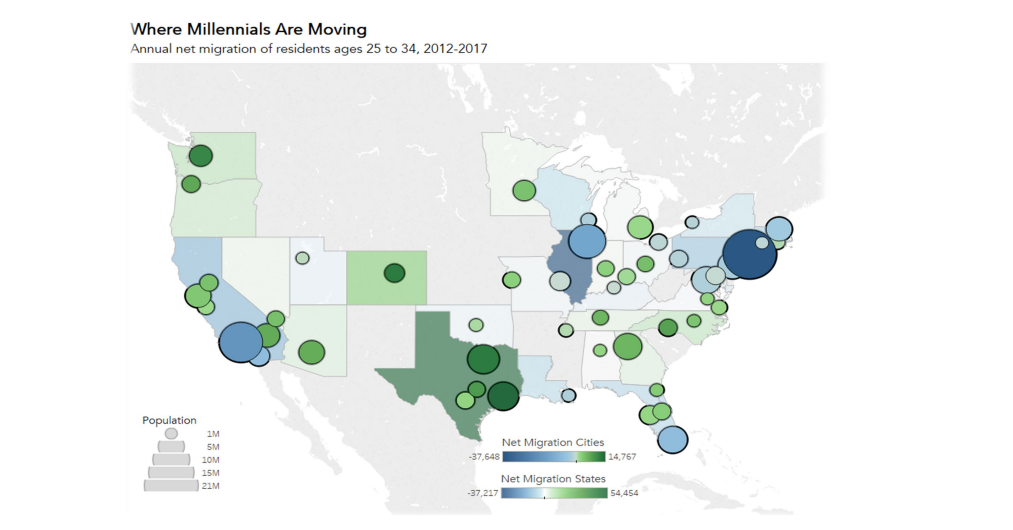

Whether these trends persist, Ms. Rice argued, will depend in part on whether homeownership among millennials picks up pace or not (see bottom plot in Figure 1) and on the ability of the housing sector to provide affordable solutions to address their needs. In relation to this, Ms. Kushi concurred with Ms. Rice on the strength of multifamily but suggested that robust multifamily supply is only part of the solution. She showed (by looking at the number of housing starts) that indeed multifamily recovered by 2013-14 and has been above its historical trends since then unlike single-family housing. However, while this may have contributed to make it relatively cheaper to rent than to buy among the least affordable U.S. metros, those same areas still tend to report among the lowest homeownership rates and largest outward migrations of millennials moving out (Figure 2).

Figure 1. The millennials’ growing role in U.S. housing

Source: Top panel: U.S. Census Bureau, Knoema. Bottom panel: CBRE Research, homeownership rates not seasonally-adjusted. Author’s rendering based on James Clapp (Certainty Home Loans) and Jeanette I. Rice (CBRE)’s figures.

Figure 2. Internal migration (by millennials)

Source: U.S. Census Bureau, First American Financial Corp. Author’s rendering based on Odeta Kushi (First American Financial Corp.)’s figure.

The challenges of housing affordability

To the extent that U.S. and Texas housing have regained their footing over the last decade, Mr. Gaines stated, it certainly has not improved much for the low-price and entry-level segments of the market. Mr. Gaines showed that residential construction in these segments has not recovered relative to its pre-recession peak. The Texas data he reviewed (in itself a microcosm of U.S. housing) shows also that, under $200,000, neither sales nor the supply of vacant developed lots for homes has recovered much. Most significant going forward is that neither have the number of housing starts per capita or building permits in Texas.

Moreover, Ms. Kushi showed that the inventory of new and existing homes for sale is pretty tight in the U.S., at a historic quarter century low. Mr. Gaines indicated that the current months of inventory in Texas is also quite low but particularly so for the low-price segment–in the neighborhood of 2.3 months for homes between $100,000 and $200,000. Similarly, Mr. Nothaft noted that nationally months’ supply for sale by price tier for existing homes is particularly tight for entry-level homes and that new construction is also heavily tilted towards premium (rather than entry-level) home sales across the U.S. Not surprisingly then, one of the main challenges for housing going forward, concluded Mr. Gaines, is how to meet the housing needs in particular of low-income households and new entrants.

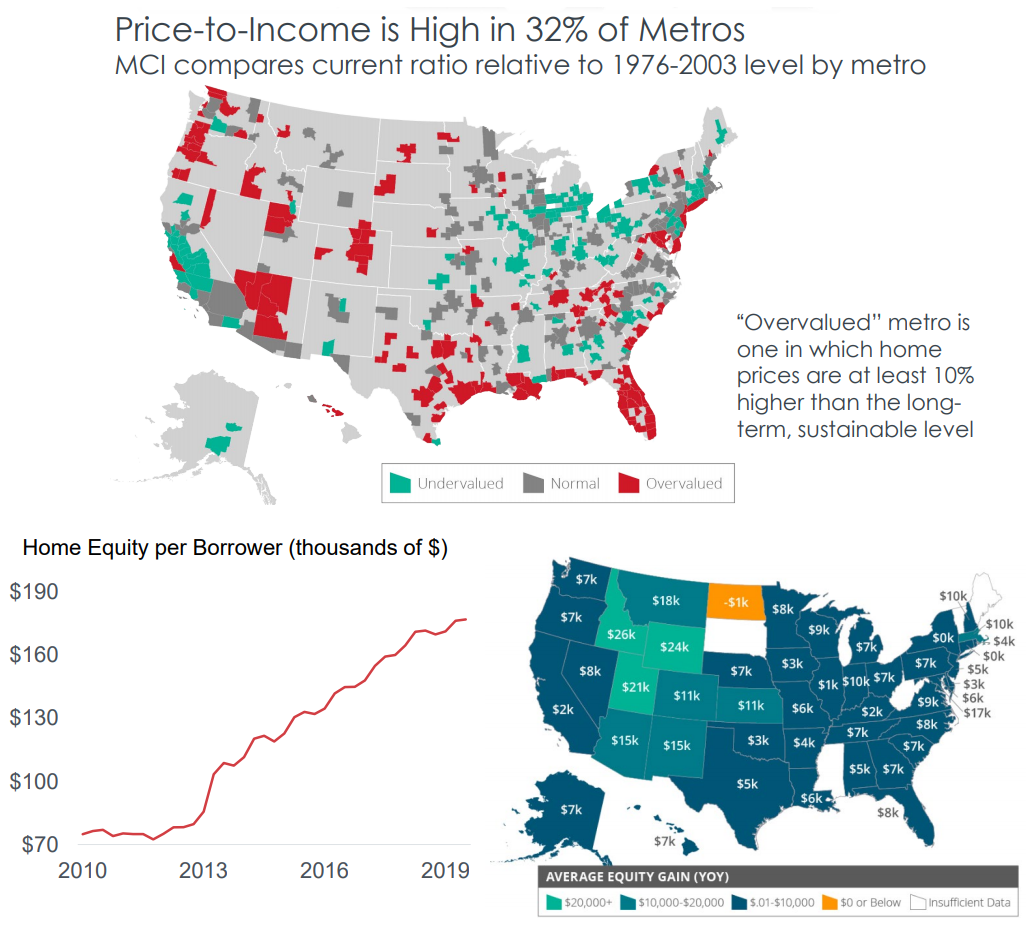

Mr. Gaines also presented evidence that Texas’ median home price growth has almost doubled the state’s median income since 2000. Along the same lines, Mr. Nothaft showed research that CoreLogic had done across all major metropolitan areas in the U.S. gauging the affordability of each metro market. The CoreLogic measure is based on the house price to income ratio relative to its metro-specific sustainable, long-run level. CoreLogic’s findings suggest that house prices have become out of step with incomes for the average household making 32% of all metropolitan statistical areas overvalued as of February 2020 (see top panel of Figure 3). Mr. Nothaft indicated that while no national price bubble can be identified, overvaluation risks and price declines in select areas area a concern.

Moreover, Mr. Nothaft said, the same strong rebound in house prices since 2013 that has worsened affordability has in turn generated large equity gains for homeowners. This housing equity gains have supported household spending—with a record $327 billion spent on home improvement and repairs alone in 2019 (see bottom panel of Figure 3).

Figure 3. Housing affordability in the U.S. and home equity gains

Source: Top panel: CoreLogic Market Condition Indicators (February 4, 2020). Bottom panel: CoreLogic Home Equity Report & Public Records, Joint Center for Housing Studies Leading Indicator of Remodeling Activity. Author’s rendering based on Frank Nothaft (CoreLogic)’s figures.

“Big data”, fintech place in housing finance

Kristopher S. Gerardi (Federal Reserve Bank of Atlanta) forcefully argued for more “big data” at the micro level in finance in order to gauge important risk factors associated with loan portfolios of developers and consumer mortgages. A better understanding of all liens on property including “piggybacks” and home-equity loans (and lines of credit) and about the characteristics of mortgages is critical to assess risks and for financial stability considerations. For instance, Mr. Gerardi argued that lack of data on “piggyback” mortgages, which became common in the 2000s, led to an underestimation of borrower mortgage leverage at origination which was hiding the increasing risks for housing finance prior to the 2008 recession. Lack of data also led to underestimates of certain “risky” mortgage products that facilitated speculation such as interest-only mortgages which we now know accounted for 30-50% of originations during the housing boom period.

Benjamin Navarro (Fannie Mae) noted the importance of government-sponsored enterprise (GSE) reform for the functioning of the markets providing support for housing finance and to ensure credit access for consumers. James Clapp (Certainty Home Loans) seconded the general view that trends in demographics continue to shape the future of housing. However, Mr. Clapp placed the emphasis on some key trends in the financing space and ultimately on the role of technology. Mr. Clapp showed that:

First, refinancing was still going on even as interest rates started to firm up between 2016 and 2019 (but dropping to only around 25% of the market) while purchase volume had been increasing at about 10% yearly during the same period. Second, data on the volume originated shows that about 60% is through retail banking, 10-25% is wholesale (but growing), and the rest accounts for the remaining 20-25% (which tends to be higher during refinancing periods). Independent mortgage bankers (IMBs) play a larger role on the retail side, particularly serving low- and middle-income customers. Third, the estimates show that one of the major loan expense items for lenders nowadays is the tech expense (over $1000 per loan according to the most recent estimates he discussed).

From all of this, Mr. Clapp noted that mid-size banks and large IMBs have seen their per loan costs increase sharply as they play catch up with the large banks who mostly operate with more sophisticated custom-built solutions and are able to spend more on technology. These technology expense numbers, Mr. Clapp argued, reflect the increasing role that technology is playing as a market disruptor. In his view, technology is both a response to and a reason for the continued compression of margins in loan origination. He also noted that the mortgage lending industry is being re-shaped by new technologies and the lenders’ own survival is increasingly dependent on the ability to spend in order to adapt their business models and adopt those technologies—among them, in particular, fintech.

Mr. Clapp also indicated that while disruption used to come from business-to-business (B2B) alternatives, now is in fact more and more about business-to-consumer (B2C) alternatives. B2B disruptors include the likes of Ellie Mae (founded in 1997), Finicity (1999), Black Knight (2008), FormFree (2008), Total Expert (2012), Blend (2012), Lead aggregators, Simplifile, Docutech, etc. And, more recently, the new crop of B2C consumer-direct fintech include much-talked-about startup banks like Varo (1 million customers), Monzo (3 million), Chime (5 million), MoneyLion (5.7 million), Revolut (8 million), Figure, etc.

Rethinking the supply-side of (affordable) housing

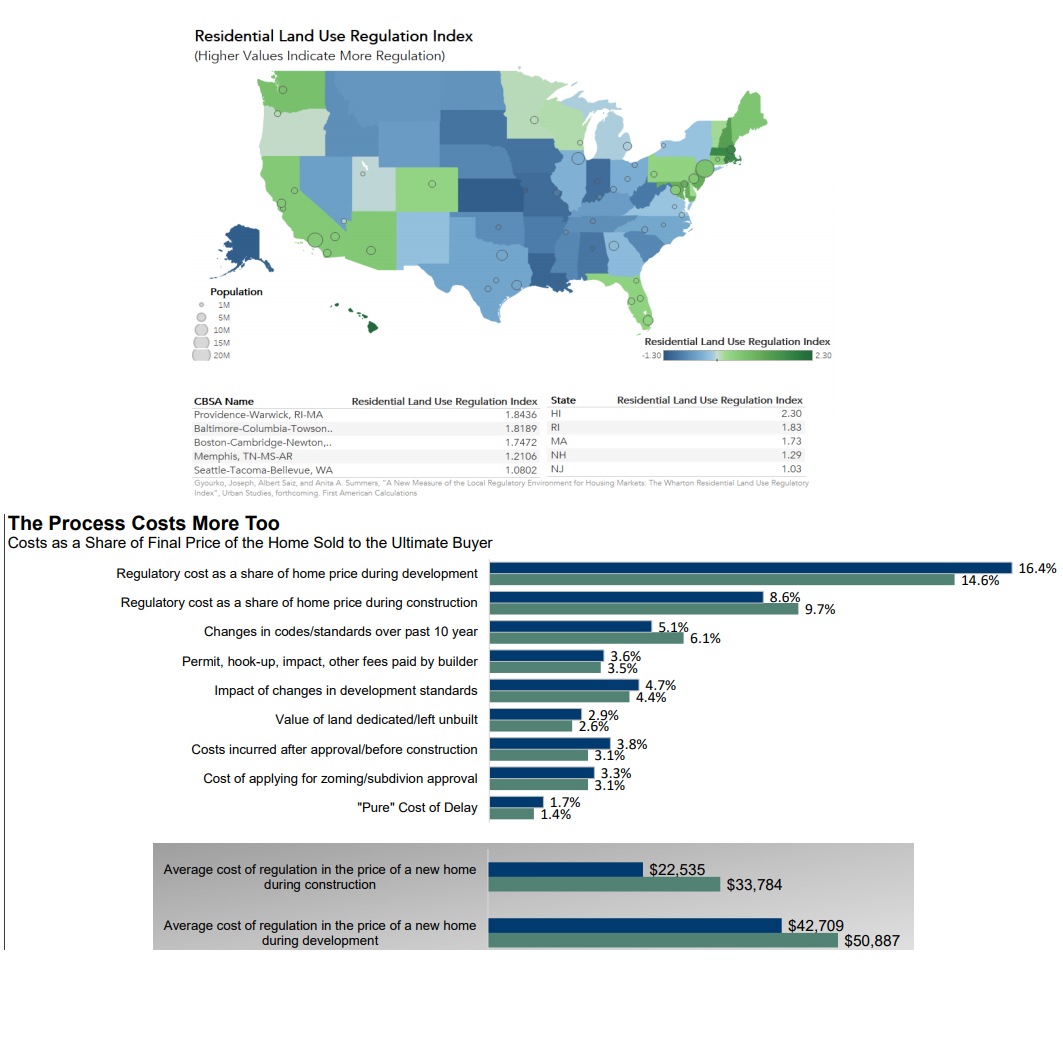

Mr. Nothaft showed that costs of building materials have been increasing more than inflation (lumber and steel, drywall and insulation, plumbing and electrical, and masonry and roofing all outpaced inflation between December 2016 and December 2019). Mr. Gaines showed similar trends for Texas with land values (and also improvement costs) being notably higher on more recent construction. Ms. Kushi argued that labor shortages are partly to blame for the increase in construction costs—the ratio of construction job openings to hires, for instance, has gone up fourfold since 2012. However, she also argued that tighter regulation particularly on residential land use (as can be seen in Figure 4) remains one of the major factors driving overall construction and urban land development costs up. And, in her view, a supply-restricted market ultimately drives up prices and makes housing less affordable.

The concern about regulation is an issue that was echoed and extensively discussed by Paige Shipp (Metrostudy) as well. Ms. Shipp argued that a great deal of this added regulatory burden arises from changes in societal attitudes (notably, NIMBY or Not In My Backyard views) that are becoming more widespread and impacting housing markets at the local level. Related to this, Ms. Rice noted the increasing mismatch between what is affordable and what is desired (which may reflect the desire for higher standards that in part motivates NIMBY regulations) is yet another reason discouraging homeownership among millennials.

Ms. Shipp argued that current market trends in construction are increasingly determined by technology. In Ms. Shipp’s view, the changes are partly organic arising from the need to adapt to a changing environment (NIMBY regulations, etc.) or dictated by the necessity to keep homes affordable (higher density through multifamily and lower square footage).

Ms. Shipp also highlighted how financing for real estate technology developments is booming (with venture-backed capital leading the way forward) driven by the ever-growing need to build quality homes at affordable prices. Changes are, arguably, long overdue since the way houses are being built is basically the same way it was 60 years ago with huge inefficiencies and material waste. Among the most relevant trends arising from technological innovation, Ms. Shipp cited off-site construction (for example, the experiences of BMC, Entekra, Ecocor and Blu Homes) or the growing use of 3D printing. Mr. Navarro similarly alluded in his remarks to the impact on affordability of modular homes and other alternative construction methods.

And, finally, Ms. Shipp argued that change can also come from technologically-enabled disruption—an issue that was cited by Federal Reserve Bank of Dallas President Robert Kaplan in his opening remarks to the conference and that President Kaplan extensively discusses in his work. Some of the disruption can come simply from outside forces, Ms. Shipp noted, citing the example of Berkshire Hathaway’s acquisition of Clayton Homes. Others may come by altering the business model in very fundamental ways. For instance, Ms. Shipp spoke of companies that are getting a lot of traction whose business model is based on removing the agent from the process: Zillow, Opendoor, RedfinNow, Offerpad, Orchard, knock, etc. She also cited on-going efforts to integrate housing in broader sales platforms (Amazon’s recent partnership with Realogy) and even circumvent the builders (start-ups selling pre-fabricated houses through Amazon, etc.).

Concluding remarks

As Pia Orrenius (Federal Reserve Bank of Dallas) said in her closing remarks, much has changed in housing over the past decade and many of the trends discussed at this conference will surely continue to be scrutinized going forward and will be revisited at the next conference in two years. But, certainly, we are living through interesting and challenging times for the U.S. housing sector with still much… room to grow.

Figure 4. The impact of tighter regulation on U.S. housing

Source: Bottom panel: NAHB, First American Financial Corp, Gyourko et al. (forthcoming). Author’s rendering based on Odeta Kushi (First American Financial Corp.)’s figures.

Session 1—Overview of Texas Economy and Housing Markets

From left to right: Keith Phillips (Federal Reserve Bank of Dallas), Harold D. Hunt (Real Estate Center at Texas A&M University), and James P. Gaines (Real Estate Center at Texas A&M University).

Session 2—The Future of Housing Finance

From left to right: W. Scott Frame (Federal Reserve Bank of Dallas), James Clapp (Certainty Home Loans), Benjamin Navarro (Fannie Mae), and Kristopher S. Gerardi (Federal Reserve Bank of Atlanta).

Keynote

Frank Nothaft (CoreLogic).

Session 3—Housing Trends and Outlook

From left to right: Odeta Kushi (First American Financial Corp.), Laila Assanie (Federal Reserve Bank of Dallas), Jeanette I. Rice (CBRE), and Paige Shipp (Metrostudy).

About the Author

Enrique Martínez García is a senior research economist and policy advisor at the Federal Reserve Bank of Dallas. He works on the Federal Reserve Bank of Dallas International House Price Database and on the joint Federal Reserve Bank of Dallas—Lancaster University Management School International Housing Observatory and has done extensive research on topics related to housing. Of particular interest because of their relevance to this conference would be his research on the impact of oil prices on housing (Grossman et al. (2019) and his research on testing and date-stamping breaks due to mildly explosive behavior that can be indicative of unsustainable house prices across metro areas in Texas and the U.S. (Grossman et al. (2016) and Grossman et al. (2019)). Martínez García thanks Valerie Grossman (Federal Reserve Bank of Dallas) and Luis Bernardo Torres (Real Estate Center at Texas A&M University) for their helpful suggestions and feedback.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts