Tuesday, June 25, 2019

Housing Market in Denmark

From IMF’s latest report on Denmark:

“The housing market plays a vital role in Denmark, reinforcing macro-financial linkages. High mandatory pension contributions and household savings have created a pension system that has facilitated the development of the world’s largest covered bond market in percent of GDP. Insurance companies, pension funds, and foreign investors are among the largest holders of covered bonds, which are issued by MCIs to fund household mortgages (…). Thus, housing asset exposures interlink MCIs, pension funds, insurance, foreign investors, and the household sector. Hence, shocks to real estate may impact negatively households’ financial and non-financial assets, hindering consumption; thus, reinforcing macro-financial linkages (SIP 2018).

High household leverage amid high house valuations remains a key source of macrofinancial vulnerability. High house prices, a favorable tax treatment, and easy access to low-cost borrowing incentivize the funding of housing with large mortgages. These factors explain why Danish households’ debt-to-income ratios are among the highest in advanced economies. Large liabilities are counterbalanced by large assets (housing and pension). However, high gross debt, combined with illiquid assets (concentrated in real estate) expose households to price and interest rate shocks that can impact asymmetrically their balance sheet. Two types of households appear particularly vulnerable. Households who have purchased in potentially overvalued urban areas (SIP 2018), where loan-to-income (LTI) ratios and credit growth are higher than anywhere else. And low-income households who spend a significant share of their income on housing. These vulnerabilities are compounded by the large proportion of variable-rate and interest-only mortgages in the system (…).

Recent developments are encouraging but further action is needed. Staff welcomes the comprehensive suite of policies that have been implemented in recent years. These include policies targeting households and financial intermediaries in the form of macroprudential policies (SIP 2018), supervisory guidance for MCIs and banks, and a reform of property taxation (IMF 2017). While overall house prices are softening and households are switching to loans with higher amortization and lower interest rate risk, staff advocates further deployment of coordinated policies to address remaining vulnerabilities.

Macroprudential instruments. In an economy with elevated house prices, rules targeting loan-to-value (LTVs) become less binding. Thus, increased focus on income-based measures, including debt-to-income (DTI), loan-to-income (LTI) and debt-service-to-income (DSTI) might prove more effective in addressing high leverage and encourage faster amortization. Staff welcomes rules implemented in 2018 to limit lending via interest-only and floating-rate mortgages to highly-indebted households.21 However, authorities could strengthen DTI restrictions for all loans, irrespective of their loan-to-value ratios. Tighter limits on income based measures for interest-only and adjustable-rate mortgages should also be considered, while calibrating limits to these measures for lower risk groups—first-time home buyers and low-levered households—and where financing is via fixed–rate mortgages.22 Highly-leveraged households—with debt-to-income above 400 percent—should be subject to mandatory amortization, irrespective of amortization periods (SIP 2018).

Macroprudential framework. A review of the efficacy of policy implementation is encouraged, including a review of institutional arrangements (…). The process followed by the SRC to arrive at a recommendation can take too long, potentially hindering implementation. Given that the decision-making power lies with the government, there is a risk that political considerations could delay the consensus process that tends to form the basis of such recommendations (FSAP 2014). Experience from other countries indicates that improvements in timeliness can be achieved by assigning independent authorities a macroprudential mandate which includes legal powers to implement macroprudential policy with corresponding transparency and accountability requirements.

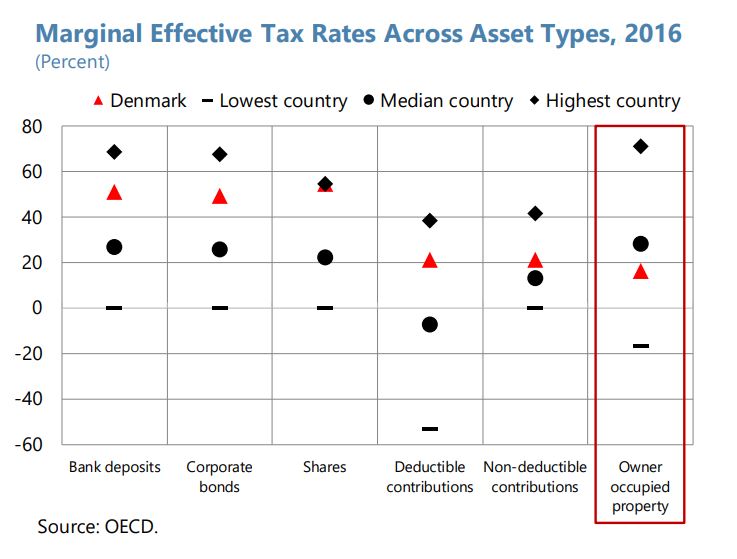

Tax policy. Tax treatment of owneroccupied housing is very favorable compared to other savings vehicles and most OECD countries. MID should be reduced further, taking advantage of the current low rate environment. To incentivize homeowners to swap risky mortgages, MID could be made conditional on amortizing and/or fixed rate mortgages. Balancing tax incentives for pension contributions could release resources for larger down-payments; thereby reducing household leverage.

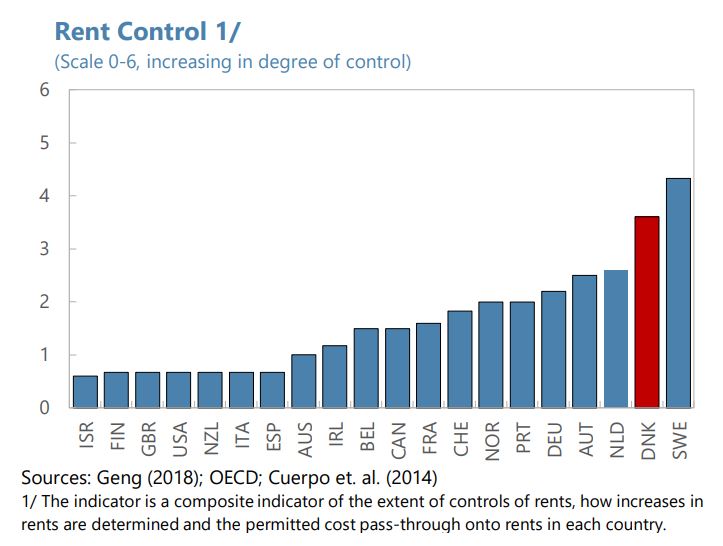

Housing supply. Rent controls in Denmark, among the highest in advanced economies, should be reduced to stimulate the rental market, while protecting the interest of the most vulnerable. Restrictions on the size of new apartments should be relaxed in urban areas to improve demand-supply mismatches. Upgrading of public transportation could relieve house price pressures around fast growing urban centers. Streamlined zoning and planning procedures across municipalities could increase supply, thereby alleviating price pressures.

Authorities agree that macro-financial risks stemming from the interaction between high household leverage and high house valuations should be followed closely. Authorities indicate that household resilience to interest rate increases likely improved as more homeowners continue shifting towards fixed rate mortgages and longer fixing periods. They also welcome the recent softening in apartment prices. The authorities argue that additional measures would require further analysis of the effects on the housing market and the overall economy. Authorities see the macroprudential framework as well functioning including the timeframe for the CCyB implementation and SRC’s independence. The DN notes that the long-term success of the framework depends on policy-makers’ continued implementation of the SRC’s recommendations.”

Posted by at 11:19 AM

Labels: Global Housing Watch

Subscribe to: Posts