Friday, May 10, 2019

Housing View – May 10, 2019

On cross-country:

- Is co-living an answer to the affordable housing crisis? – World Economic Forum

On the US:

- House Prices at Risk – Money & Banking

- How About Leaving Fannie Mae and Freddie Mac Alone? – Bloomberg

- Cost, crowding, or commuting? Housing stress on the middle class – Brookings Institute

- Housing trade-offs: Affordability not the only stressor for the middle class – Brookings Institute

- Since 2008, Only High-Income People Have Seen Their Housing Costs Drop – Citylab

- [Your city] has a housing crisis. The answer is [more/less] [building/money/regulation] – Brookings Institute

- Following the Money in Residential Real Estate – New York Times

- Does Gentrification Displace Poor Children? New Evidence from New York City Medicaid Data – NBER

- Racial Segregation in Housing Markets and the Erosion of Black Wealth – NBER

- Housing market and bank lending effects on young firms and local economies – VoxEU

- Consumers Temper Optimism on Housing Despite Improved Mortgage Rate Expectations – Fannie Mae

- Fulfilling the Dream of Homeownership: How Do Families and Others Play a Role? – Freddie Mac

- New Taxes and Higher Density Aren’t Fixing Vancouver’s Housing Problem – Citylab

On other countries:

- [Canada] Stephen S Poloz: Risk sharing, flexibility and the future of mortgages – Bank of Canada

- [Canada] Canada’s Housing Will Return to Growth, Central Bank Governor Says – Wall Street Journal

- [Canada] Risks Are Receding in Canada’s Housing Market, Agency Says – Bloomberg

- [Hong Kong] What do we know about Housing Supply? The case of Hong Kong – City University of Hong Kong

On cross-country:

- Is co-living an answer to the affordable housing crisis? – World Economic Forum

On the US:

- House Prices at Risk – Money & Banking

- How About Leaving Fannie Mae and Freddie Mac Alone? – Bloomberg

- Cost, crowding, or commuting? Housing stress on the middle class – Brookings Institute

- Housing trade-offs: Affordability not the only stressor for the middle class – Brookings Institute

- Since 2008,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, May 9, 2019

Snapshots of US Income Taxation Over Time

From Conversable Economist:

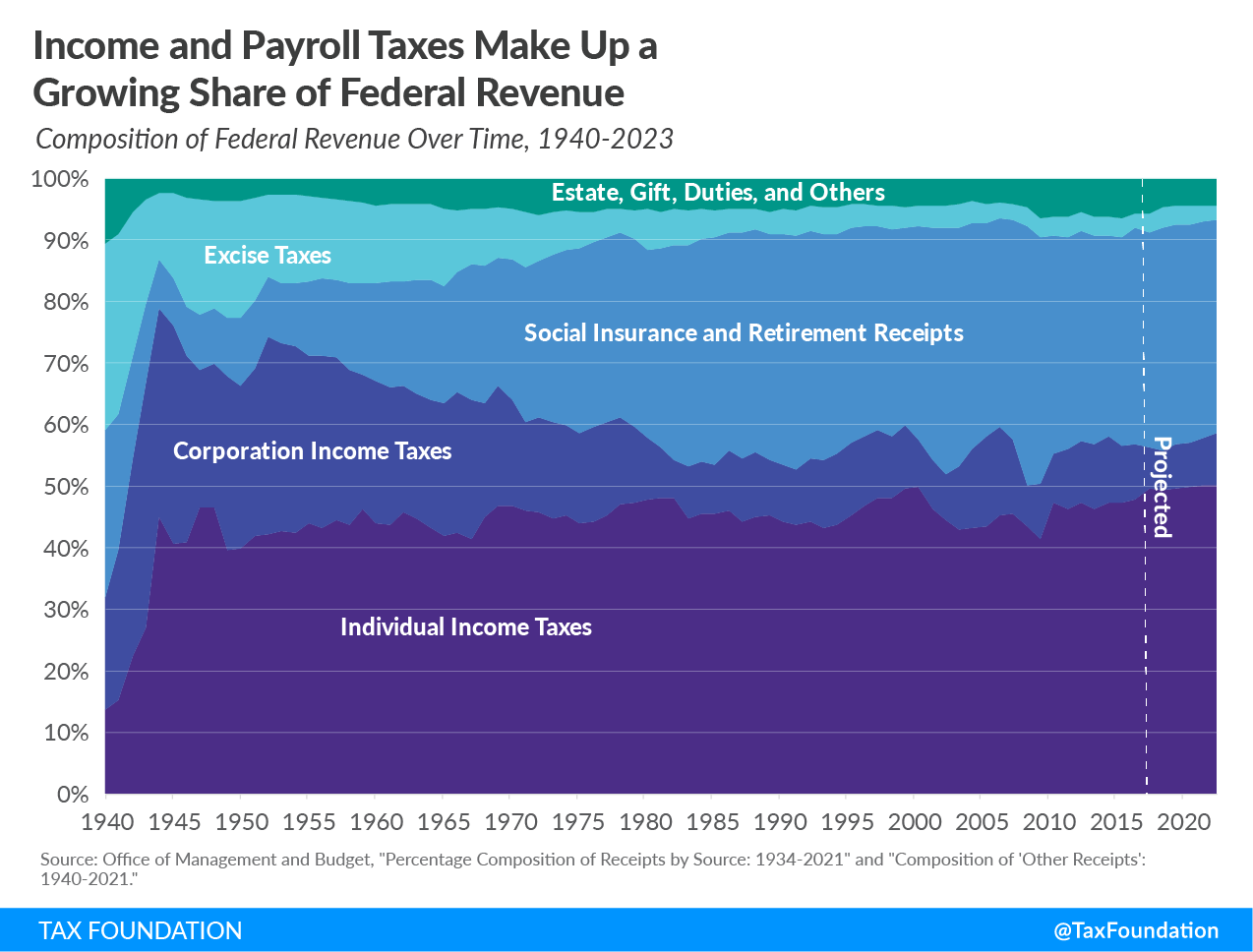

“As Americans recover from our annual April 15 deadline for filing income taxes, here are a series of figures about longer-term patterns of taxes in the US economy. They are drawn from a series of blog posts by the Tax Foundation over the last few months. The Tax Foundation is a nonpartisan group whose analysis typically leans toward side that taxes on those with high incomes are already high enough. However, the figures that follow are compiled from fairly standard data sources: IRS data, the Congressional Budget Office, and the like.

For example, here’s a figure showing what taxes are the main sources of federal income over time from Erica York. She writes: “Before 1941, excise taxes, such as gas and tobacco taxes, were the largest source of revenue for the federal government, comprising nearly one-third of government revenue in 1940. Excise taxes were followed by payroll taxes and then corporate income taxes. Today, payroll taxes remain the second largest source of revenue. However, other sources have shifted in relative importance. Specifically, individual income taxes have become a central pillar of the federal revenue system, now comprising nearly half of all revenue. Following an opposite trend, corporate income and excise taxes have decreased relative to other sources.”

From Conversable Economist:

“As Americans recover from our annual April 15 deadline for filing income taxes, here are a series of figures about longer-term patterns of taxes in the US economy. They are drawn from a series of blog posts by the Tax Foundation over the last few months. The Tax Foundation is a nonpartisan group whose analysis typically leans toward side that taxes on those with high incomes are already high enough.

Posted by at 9:14 AM

Labels: Macro Demystified

Tuesday, May 7, 2019

Is Something Different this Time about the Effect of Technology on Labor Markets?

From Conversable Economist:

“There’s a well-worn conversation about the relationship between new technology and possible job displacement which goes something like this:

Concerned person: “New developments in information technology and artificial intelligence are going to threaten lots of jobs.”

Skeptical person: “Economies in developed countries have been experiencing extraordinary developments and shifts in new technology for literally a couple of centuries. But as old jobs have been dislocated, new jobs have been created.”

Concerned person: “This time seems different.”

Skeptical person: “Every time is different in the specific details. But there’s certainly no downward pattern in the number of jobs in the last two centuries, or the last few decades.”

Concerned person: “Still, the way in which information technology and artificial intelligence replace workers seems different than the way in which, say, assembly lines replaced skilled artisan workers or combine harvesters replaced farm workers. ”

Skeptical person: “Maybe this time will be different. After all, it’s logically impossible to prove that something in the future will NOT be different. But based on the long-run historical pattern, the evidence that new technology leads to shifts in the labor market is clear-cut, while the evidence that it leads to permanent job loss for the population as a whole is nonexistent.”

Concerned person: “Still, this current wave of technology seems different.”

Skeptical person: “I guess we’ll see how it unfolds in the next decade or two.”

The most recent Spring 2019 issue of the Journal of Economic Perspectives has a symposium on “Automation and Employment.” Two of the articles in particular offer a concrete arguments about how something is different with how the current new technologies are interacting with labor markets.

Daron Acemoglu and Pascual Restrepo discuss “Automation and New Tasks: How Technology Displaces and Reinstates Labor.” They suggest a framework in which automation can have three possible effects on the tasks that are involved in doing a job: a displacement effect, when automation replaces a task previously done by a worker; a productivity effect in which the higher productivity from automation taking over certain tasks leads to more buying power in the economy, creating jobs in other sectors; and a reinstatement effect, when new technology reshuffles the production process in a way that leads to new tasks that will be done by labor.”

From Conversable Economist:

“There’s a well-worn conversation about the relationship between new technology and possible job displacement which goes something like this:

Concerned person: “New developments in information technology and artificial intelligence are going to threaten lots of jobs.”

Skeptical person: “Economies in developed countries have been experiencing extraordinary developments and shifts in new technology for literally a couple of centuries. But as old jobs have been dislocated,

Posted by at 11:12 AM

Labels: Inclusive Growth

Globalization, Market Power, and the Natural Interest Rate

From a new IMF working paper by Jean-Marc Natal and Nicolas Stoffels:

“We argue that strong globalization forces have been an important determinant of global real interest rates over the last five decades, as they have been key drivers of changes in the natural real interest rate—i.e. the interest rate consistent with output at its potential and constant inflation. An important implication of our analysis is that increased competition in goods and labor market since the 1970s can help explain both the large increase in real interest rates up to the mid-1980s and—as globalization forces mature and may even go into reverse, leading to incrementally rising market power—its subsequent and protracted decline accompanied by lower inflation. The analysis has important implications for monetary policy and the optimal pace of normalization.”

From a new IMF working paper by Jean-Marc Natal and Nicolas Stoffels:

“We argue that strong globalization forces have been an important determinant of global real interest rates over the last five decades, as they have been key drivers of changes in the natural real interest rate—i.e. the interest rate consistent with output at its potential and constant inflation. An important implication of our analysis is that increased competition in goods and labor market since the 1970s can help explain both the large increase in real interest rates up to the mid-1980s and—as globalization forces mature and may even go into reverse,

Posted by at 11:11 AM

Labels: Macro Demystified

Friday, May 3, 2019

Global Fossil Fuel Subsidies Remain Large: An Update Based on Country-Level Estimates

From a new IMF working paper by David Coady, Ian Parry, Nghia-Piotr Le and Baoping Shang:

“This paper updates estimates of fossil fuel subsidies, defined as fuel consumption times the gap between existing and efficient prices (i.e., prices warranted by supply costs, environmental costs, and revenue considerations), for 191 countries. Globally, subsidies remained large at $4.7 trillion (6.3 percent of global GDP) in 2015 and are projected at $5.2 trillion (6.5 percent of GDP) in 2017. The largest subsidizers in 2015 were China ($1.4 trillion), United States ($649 billion), Russia ($551 billion), European Union ($289 billion), and India ($209 billion). About three quarters of global subsidies are due to domestic factors—energy pricing reform thus remains largely in countries’ own national interest—while coal and petroleum together account for 85 percent of global subsidies. Efficient fossil fuel pricing in 2015 would have lowered global carbon emissions by 28 percent and fossil fuel air pollution deaths by 46 percent, and increased government revenue by 3.8 percent of GDP.”

From a new IMF working paper by David Coady, Ian Parry, Nghia-Piotr Le and Baoping Shang:

“This paper updates estimates of fossil fuel subsidies, defined as fuel consumption times the gap between existing and efficient prices (i.e., prices warranted by supply costs, environmental costs, and revenue considerations), for 191 countries. Globally, subsidies remained large at $4.7 trillion (6.3 percent of global GDP) in 2015 and are projected at $5.2 trillion (6.5 percent of GDP) in 2017.

Posted by at 1:23 PM

Labels: Energy & Climate Change

Subscribe to: Posts