Friday, May 10, 2019

Housing Market in Macao

From the IMF’s latest report on Macao:

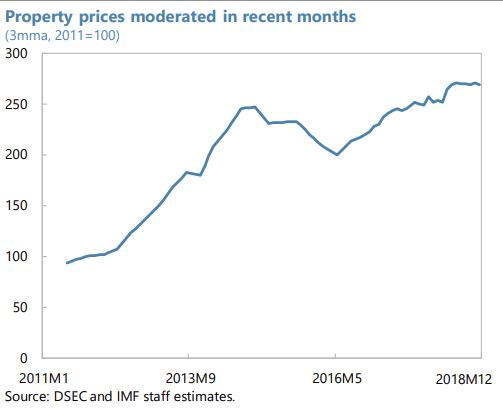

“The housing market has strongly recovered with the economic rebound that started in mid-2016, but the market appears to have cooled in the second half of 2018. After falling between mid-2014 and mid-2016, the residential property price index recovered fully between mid2016 and mid-2018 (in real terms), though it stayed flat in the second half of 2018. Even though residential property prices remained below trend in 2018, they appear to remain somewhat overvalued, for smaller units in particular (…).

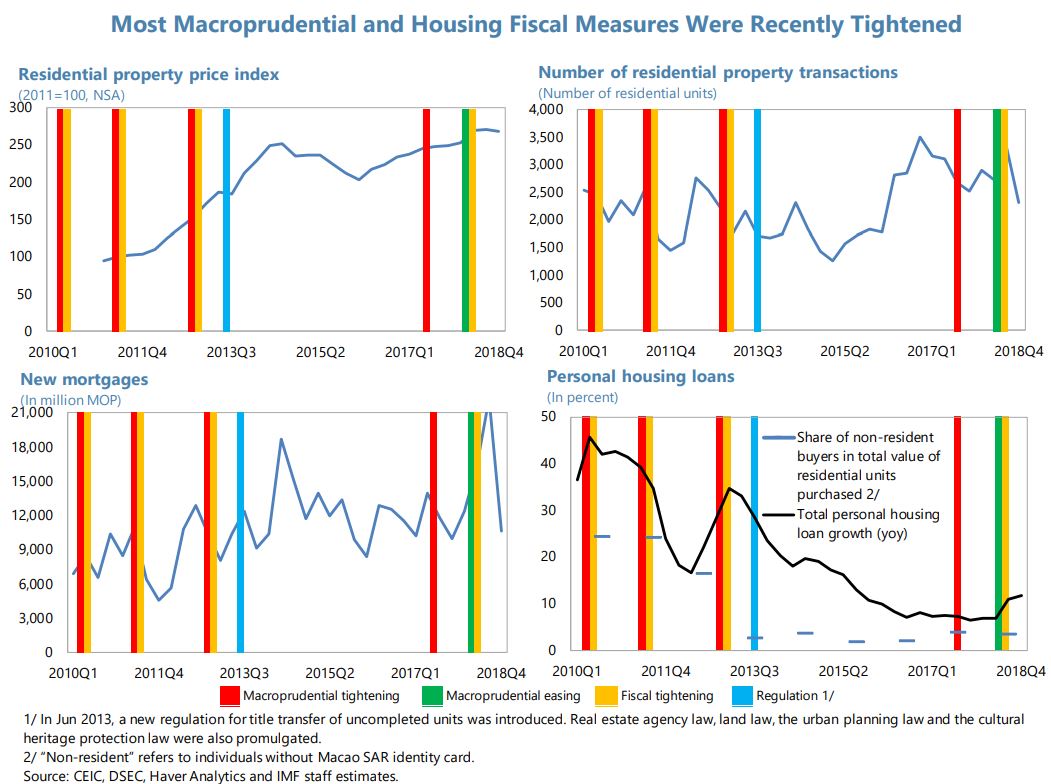

The current housing macroprudential stance and related fiscal measures appear broadly appropriate. Measures were put in place in 2017 and 2018:

- New measures were introduced to mitigate housing market risks via containment of demand. The loan-to-value limit for non-first-time homebuyers was tightened in May 2017. In February 2018, property tax exemptions on vacant properties were removed and a special stamp duty tax on the purchase of non-first residential property was introduced.

On the other hand, the AMCM eased loanto-value limits for young first-time homebuyers to help affordability in February 2018 that may have unintentionally boosted demand and prices in this segment. Systemic risks in the housing market appear broadly contained. The authorities should continue monitoring residential property prices and the effects of recent housing market measures, as they may usually play out with a lag. Further actions should take into account evolving market conditions, including the recent growth deceleration and leveling off in residential property prices. In the event that residential property prices resume strong growth and may pose a risk to financial stability, the authorities could consider tightening macroprudential and/or fiscal-based measures property transactions by nonresidents during the housing market boom in 2010-2011. The main objective was to put in place a preventive measure to strengthen banks’ risk management considering the spike in nonresident NPLs during the Asian Financial Crisis. In 2017, to curb financial stability risks from strong growth in residential property prices, the AMCM tightened LTV for residents and nonresidents simultaneously.

- To attain the same policy objective without differentiating between residents and nonresidents, the authorities could examine whether they can protect against greater credit risk from lending to nonresidents through the existing multi-tiered-LTV structure but without the residency-based feature or by linking the differentiation in LTV limits directly to banks’ risk assessment of loans and borrowers, supported by additional measures such as enhancing information requirements and enforcement across borders and requiring banks to take into account country transfer or legal risk in their risk assessment. Further strengthening supervisory capacity of banks’ mortgage lending, broadly in line with FSAP recommendations (…), will be important to help ensure that these alternative measures are feasible

A broader set of policies should support housing affordability, where continued efforts to boost housing supply will be key. The apparent cooling of the housing market is welcome and may contribute to improving housing affordability. However, remaining affordability concerns should be addressed by a broader set of supply policies:

- Planning, zoning, and other reforms affect supply and prices only with long lags, and underlying demand for housing is expected to remain robust. Housing supply reforms should, therefore, not be delayed. Building on the government’s recent efforts to boost housing supply, plans should advance regulatory policy within a transparent framework that supports private sector supply and boosts well-targeted public housing supply, including via higher infrastructure spending.

- A coordinated government strategy to foster public and private housing supply, including an urban planning framework and urban renewal plan, would help guide reform efforts. While completing needed environmental, design, transportation and other assessments, procedures should be expedited.

Authorities’ Views.

- Housing market and policies. The authorities agreed that the housing market cooled in 2018 but remained somewhat overvalued. They noted that they stand ready to take further actions dependent on market conditions. They considered that the 2018 LTV loosening (for young firsttime homebuyers) was effective in increasing credit for this group, but acknowledged its contribution to higher prices in the small-property segment. On the residency-based LTV, they took note of the recommendation to replace the differentiation between residents and nonresidents with alternative measures. They highlighted that the objectives of the LTV framework are to strengthen banks’ risk management, curb investment/speculation motives, and moderate risks to the financial sector. They explained that the LTV framework is key for Macao SAR’s stability in light of its open capital account and large spillovers from its real estate sector. They highlighted that the 2017 LTV tightening was not aimed at nonresidents as it was done for both residents and nonresidents. They may consider other alternative measures as suggested when appropriate.

- Housing affordability. They agreed that boosting housing supply is key to address affordability concerns. In terms of public housing, they noted that ongoing projects will satisfy public housing needs by 2026 (by when they plan to add 50,000 public housing units) and they will carry on research analysis on public housing demand (including post-2026). They also noted measures under consideration to make public housing more targeted to the vulnerable. They explained that there are authorities which coordinate the strategy on public and private housing and noted that a draft master plan (to be completed in 2019) will support private housing development.”

Posted by at 1:31 PM

Labels: Global Housing Watch

Subscribe to: Posts