Wednesday, July 5, 2017

Are House Prices Overvalued in Norway?

From a new IMF paper on: Are House Prices Overvalued in Norway? – A Cross-Country Analysis:

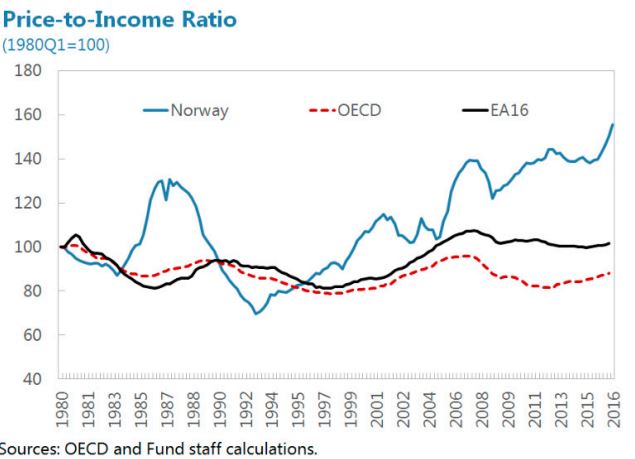

“High and overvalued house prices are a source of vulnerability in Norway, in view of the importance of the housing market to both financial and macroeconomic stability. A large correction of house prices, driven by slower real income growth, a reverse in sentiment, or interest rate hikes could weaken household balance sheets and depress private demand, and in turn adversely affect corporate and bank earnings. The authorities have been vigilant about the risks and have implemented a list of measures to strengthen the resilience of banks and households, including additional bank capital buffer requirements in line with Basel III/CRD IV, higher risk weights on residential mortgages using IRB models, tighter mortgage regulations, and the introduction of the debt-to-income limit of five times the borrower’s gross annual income to complement the loan-to-value (LTV) limits and affordability tests. Nevertheless, further targeted macroprudential measures should be considered to help contain systemic risks if vulnerabilities in the housing sector intensify, including: tighter LTV limits, a reduction in banks’ scope for deviating from mortgage regulations, and/or higher mortgage risk weights.

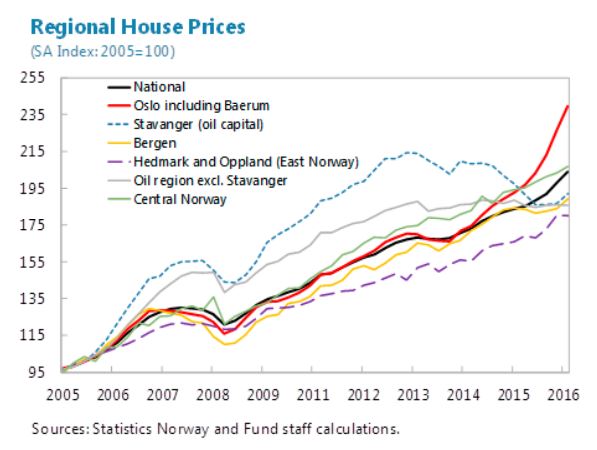

In the longer term, the macro-financial resilience of the economy to housing market shocks should be enhanced through tax reform and structural measures. A stable housing market (without pronounced boom-bust cycles) would contribute to smoother economic development. While macroprudential measures play an important role in containing the buildup of financial imbalances, a holistic approach is needed to fundamentally address the issue: (i) reducing the generous tax preferences for housing investment would help prevent demand distortions and excessive leverage, thereby dampening housing cycles; (ii) while the recent streamlining of building codes―which shortened the time needed to obtain a building permit and finish construction—is welcome, relaxing land-use and remaining constraints on new property construction, including at the municipal level, should facilitate a more efficient use of land and a flexible adjustment of housing supply, which will mitigate house price growth; and (iii) a more developed rental market would help relieve demand pressures—especially in view of the recent large influx of asylum seekers―as well as support labor mobility across regions as the economy goes through structural change.”

Posted by at 11:31 AM

Labels: Global Housing Watch

Subscribe to: Posts