Wednesday, March 15, 2017

OPEC’s Rebalancing Act

From iMFdirect by Rabah Arezki and Akito Matsumoto:

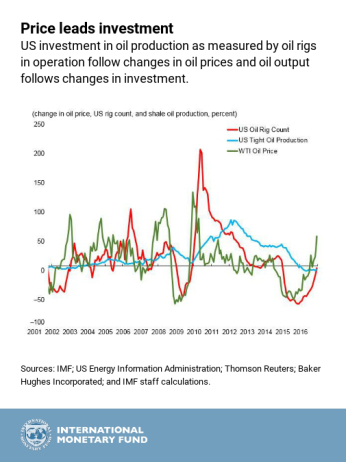

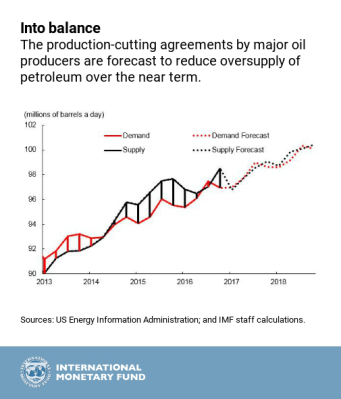

In November 2014, the Organization of Petroleum Exporting Countries (OPEC) decided to maintain output despite a perceived global glut of oil. The result was a steep decline in price.

Two years later, on November 30, 2016, the organization took a different tack and committed to a six-month, 1.2 million barrel a day (3.5 percent) reduction in OPEC crude oil output to 32.5 million barrels per day, effective in January 2017. The result was a small price increase and some price stability.

But the respite may be temporary, because the price increase is likely to stimulate other oil production that can come on line quickly. A recent sharp decline in prices because of higher than expected oil inventories in the United States underlines the temporary nature of the respite the OPEC agreement provides.

Continue reading here.

From iMFdirect by Rabah Arezki and Akito Matsumoto:

In November 2014, the Organization of Petroleum Exporting Countries (OPEC) decided to maintain output despite a perceived global glut of oil. The result was a steep decline in price.

Two years later, on November 30, 2016, the organization took a different tack and committed to a six-month, 1.2 million barrel a day (3.5 percent) reduction in OPEC crude oil output to 32.5 million barrels per day,

Posted by at 1:54 PM

Labels: Energy & Climate Change

IMF on the Decline in Labor Share of Income

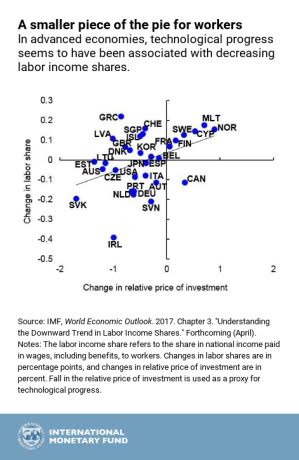

The IMF’s forthcoming World Economic Outlook will have a chapter on what drives the decline in the labor share of income in many countries around the world. Previewing the chapter (see figure above), IMF Managing Director Lagarde wrote that “trade and technological innovation have allowed countries to grow the economic pie and improve living standards, while lifting hundreds of millions of people out of poverty. Yet more could be done to mitigate the unwelcome side-effects seen in some places—including a rise in income inequality, job losses in shrinking sectors, and protracted economic and social problems across structurally weaker regions.”

For earlier work on inequality and the decline in labor share of income, see Krugman’s post for a summary, this F&D article for a longer description or this working paper for the gory details.

The IMF’s forthcoming World Economic Outlook will have a chapter on what drives the decline in the labor share of income in many countries around the world. Previewing the chapter (see figure above), IMF Managing Director Lagarde wrote that “trade and technological innovation have allowed countries to grow the economic pie and improve living standards, while lifting hundreds of millions of people out of poverty. Yet more could be done to mitigate the unwelcome side-effects seen in some places—including a rise in income inequality,

Posted by at 7:27 AM

Labels: Inclusive Growth

Friday, March 10, 2017

Trade Integration in Latin America and the Caribbean

Below is the executive summary of a new IMF report:

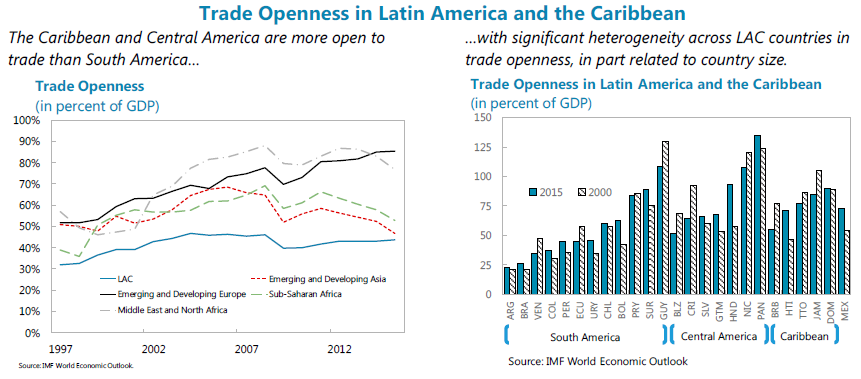

“This cluster report takes stock of and explores opportunities for trade integration in Latin America and the Caribbean (LAC). Drawing on a set of 12 analytical studies that will be issued as working papers, the report examines the determinants of trade, explores the potential to enhance LAC’s trade integration, and assesses the associated economic and social effects. To deepen understanding of the region’s policy options and trade strategies, the report also incorporates the views of LAC country authorities based on responses to a survey. This provides an opportunity to examine the alignment of recommendations based on the analytical findings with the region’s current trade policy priorities, with the caveat that the survey was conducted between late 2015 and mid-2016, prior to the most recent developments in the global trade landscape.

The report finds that LAC can reap important growth benefits from further trade integration. With trade integration below that of other regions, there is scope for LAC to increase trade as an engine of growth and help offset the weaker economic outlook without adversely affecting overall income inequality. While there is potential to enhance both inter- and intra-regional trade integration, renewed political momentum within LAC in support of greater trade openness could provide an important impetus to further intra-regional trade integration in particular. In this context, regional trade integration could be promoted through a regional trade agreement, convergence of trade rules and regulatory standards, and measures to support trade facilitation. Strategies to bolster the region’s inter-regional integration could be centered on unilateral liberalization as a complement to existing efforts to expand LAC’s network of trade agreements.

This report also emphasizes the importance of complementary policies. Continued regional efforts to strengthen infrastructure and human capital would be useful as part of a broad growth strategy. But they can also enhance trade integration, including by facilitating participation in global value chains which may offer new opportunities for technology transfer, and are critical to diversifying and upgrading the complexity of LAC’s exports. Finally, strengthened social safety nets can help lessen adjustment costs linked to further integration and promote an equitable distribution of gains from trade.”

Below is the executive summary of a new IMF report:

“This cluster report takes stock of and explores opportunities for trade integration in Latin America and the Caribbean (LAC). Drawing on a set of 12 analytical studies that will be issued as working papers, the report examines the determinants of trade, explores the potential to enhance LAC’s trade integration, and assesses the associated economic and social effects. To deepen understanding of the region’s policy options and trade strategies,

Posted by at 11:45 AM

Labels: Inclusive Growth

Trade, Growth and Inequality in Latin America and the Caribbean

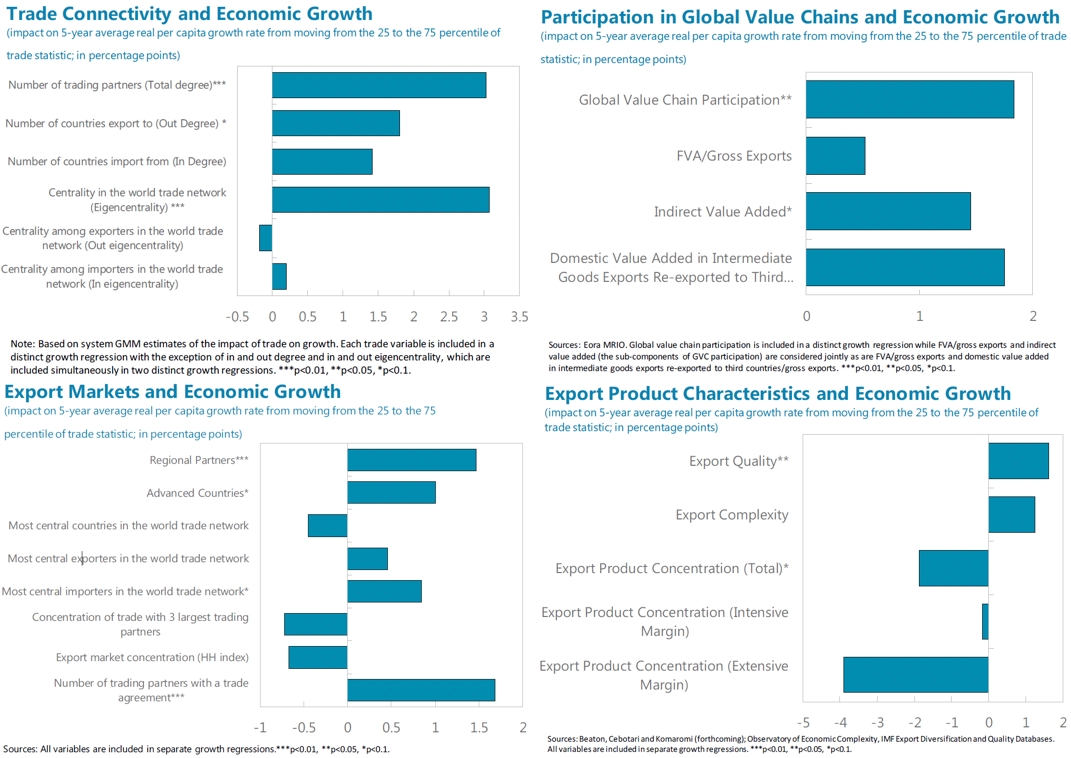

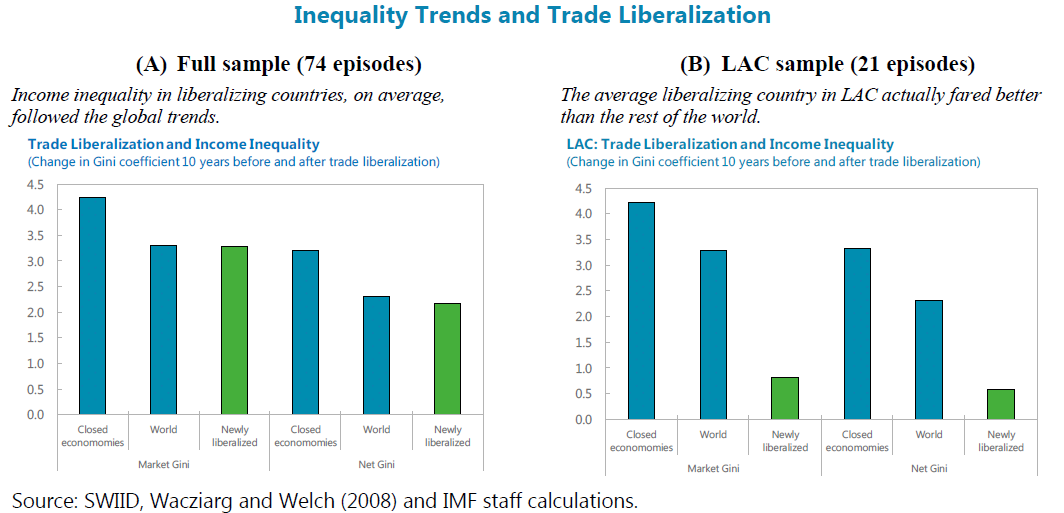

A new IMF working paper studies “the relationship between international trade, economic growth and inequality with a focus on Latin America and the Caribbean. The paper combines two approaches: First, [this paper employs] a cross-country panel framework to analyze the macroeconomic effects of international trade on economic growth and inequality considering the strength of trade connections as well as characteristics of countries’ export markets and products. Second, [this paper considers] event studies of past episodes of trade liberalization to extract general lessons on the impact of trade liberalization on economic growth and its structure and inequality. Both approaches consistently point to two broad messages: First, trade openness and connectivity to the center of the trade network has substantial macroeconomic benefits. Second, [no] statistically significant or economically sizable direct impact of trade on overall income inequality.”

A new IMF working paper studies “the relationship between international trade, economic growth and inequality with a focus on Latin America and the Caribbean. The paper combines two approaches: First, [this paper employs] a cross-country panel framework to analyze the macroeconomic effects of international trade on economic growth and inequality considering the strength of trade connections as well as characteristics of countries’ export markets and products. Second, [this paper considers] event studies of past episodes of trade liberalization to extract general lessons on the impact of trade liberalization on economic growth and its structure and inequality.

Posted by at 11:24 AM

Labels: Inclusive Growth

Monday, March 6, 2017

Global House Prices: An Update

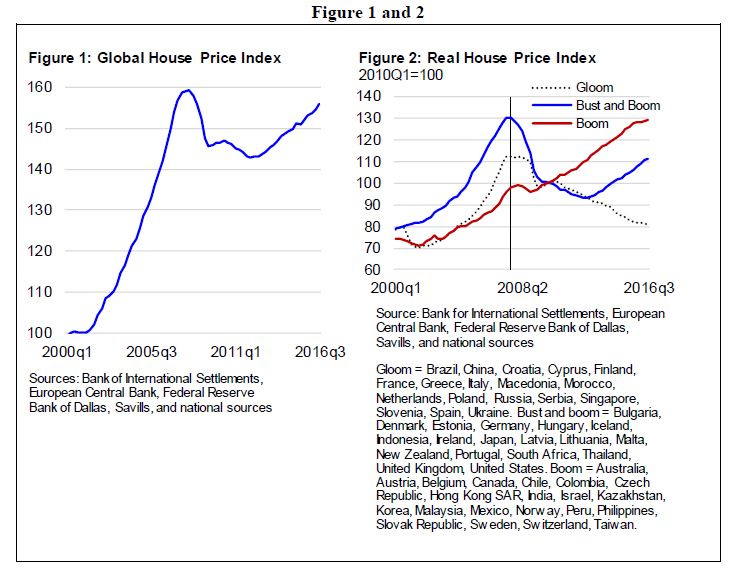

The IMF’s Global House Price Index—an average of real house prices across countries—continued to climb up in the third quarter of 2016 (Figure 1). This is the sixteenth consecutive quarter of positive year-on-year growth in the index. However, house prices are not rising everywhere around the world. As noted in our Q4 2016 Quarterly Update (and as covered in the Wall Street Journal), house price developments in the countries that make up the index fall into three clusters: gloom, bust and boom, and boom (Figure 2).

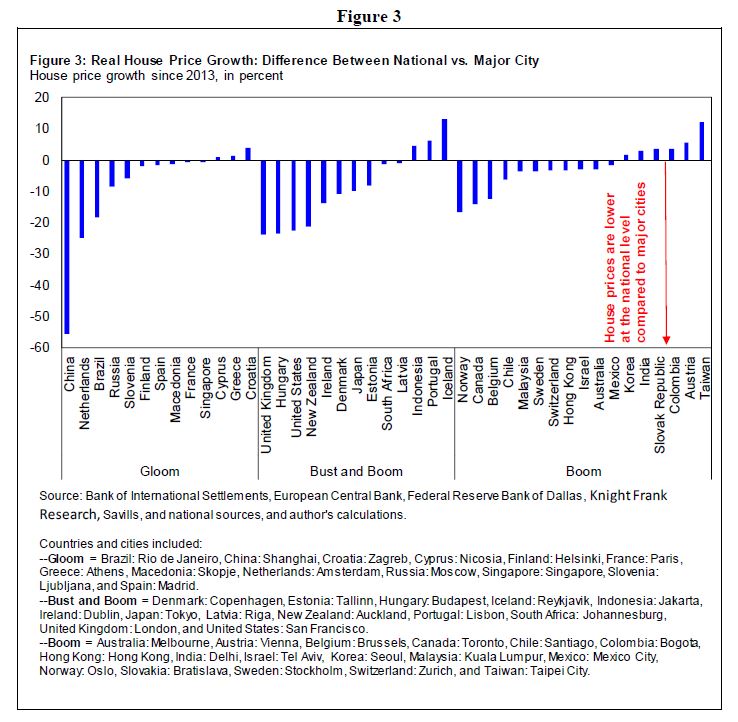

The Q1 2017 Quarterly Update digs a little deeper and shows that house prices are also not climbing up everywhere within countries. Figure 3 shows that in many countries, house prices are subdued at the national level compared to the city level.

Recent IMF assessments provide a more nuanced view of the within country house price developments.

- On Australia, IMF assessment points out that house price gains have moderated. However, the extent of cooling has varied considerably across cities. The strongest price increases continue to be recorded in Sydney and Melbourne, where underlying demand for housing remains strong. With house prices still rising ahead of income, standard valuation metrics suggest somewhat higher house price overvaluation relative to the previous IMF assessment.

- On Austria, IMF assessment notes that the cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna, while prices in the rest of the country appear broadly in line with fundamentals.

- On Turkey, IMF assessment points out that the housing market exhibits significant variations across cities. Regional variations have been further accentuated by the presence of more than 2.7 million Syrian refugees since March 2011. Cities near the Syrian border, which have absorbed larger masses of Syrian refugees have seen significant rises in local housing prices since 2011, though they have moderated in recent years.

The IMF’s Global House Price Index—an average of real house prices across countries—continued to climb up in the third quarter of 2016 (Figure 1). This is the sixteenth consecutive quarter of positive year-on-year growth in the index. However, house prices are not rising everywhere around the world. As noted in our Q4 2016 Quarterly Update (and as covered in the Wall Street Journal), house price developments in the countries that make up the index fall into three clusters: gloom,

Posted by at 9:20 PM

Labels: Global Housing Watch

Subscribe to: Posts