Friday, March 17, 2017

House Prices in Belgium

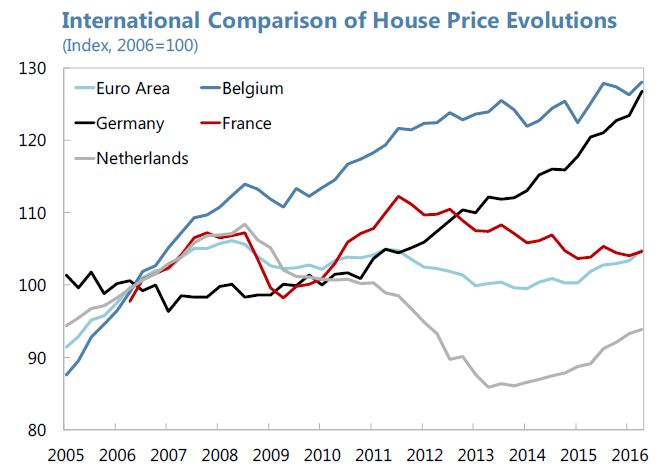

IMF’s latest report on Belgium says:

“Further macro-prudential actions may be needed to address pockets of vulnerability in the housing market. Concerns relate to the continued growth in house prices, combined with rising household indebtedness and significant shares of risky mortgage lending practices, as well as strong expansion in mortgage credit. Various overvaluation estimates are in the range of 0–20 percent. Policy actions could address these issues from various angles:

Direct remedies. In addition to the existing 5-percentage-point add-on to certain domestic mortgage risk weights, the NBB plans to impose additional capital buffers targeted at riskier loans, i.e. mortgage loans with loan-to-value (LTV) ratio higher than 80 percent, effective May 2017 (pending approval from the European authorities). Staff welcomed these measures and called for continued close monitoring of real estate market developments, including possible search-for-yield behavior in the housing market, and discussed possible further measures such as LTV or debt service to income (DSTI) limits to more directly target vulnerable borrowers.

Other buffers. An additional capital cushion, the capital conservation buffer, will also be raised by 2019 by eight banks deemed domestically systemically important, among which are the large mortgage lenders. Another buffer that could be deployed should strong credit growth persist is the counter-cyclical capital buffer, which is currently set to zero. On balance, staff considers this appropriate, in view of the various estimates of the credit gap of near zero6. Close monitoring is nevertheless warranted.”

Posted by at 5:28 PM

Labels: Global Housing Watch

Subscribe to: Posts