Thursday, October 29, 2015

Global House Prices: Gloom, Boom or Doom?

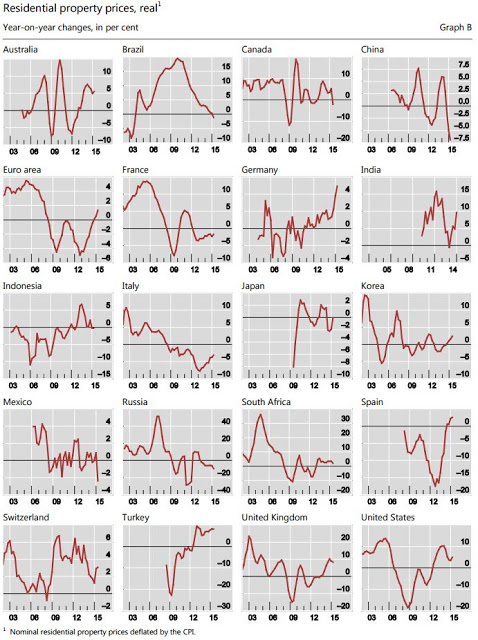

On countries where house prices are booming, the Economist notes that “Taking an average of our two measures [price-to-income and price-to-rent], houses are more than 30% overvalued in six markets [Australia, Belgium, Canada, Hong Kong, Sweden, and United Kingdom].” Meanwhile, Scotiabank points out that “The persistence of historically low interest rates is highly supportive of global housing demand. However, heightened economic uncertainty and still soft job markets remain a headwind to a stronger housing outlook in many nations. Among the more robust housing markets globally, including Canada, Australia, the U.K. and Ireland, stretched affordability could pose an increasing challenge.” All of these developments are happening against a background where the IMF “foresees lower global growth compared to last year, with modest pickup in advanced economies and a slowing in emerging markets, primarily reflecting weakness in some large emerging economies and oil-exporting countries.”

House price developments by region

Africa & Middle East and Central Asia: “South Africa’s housing market is slowing, with the price index for medium-sized apartments rising by a meagre 0.6% during the year to Q2 2015”, notes Global Property Guide. In Nairobi “a building boom is starting (…) Property prices have increased almost fourfold since the early 2000s”, says the Economist. Meanwhile, “Dubai’s residential property prices plunged 11.72% during the year to Q2 2015, the second consecutive quarter of house price falls (…)”, notes Global Property Guide. “The potential of this region for real estate investment is vast given the size of population and rate of urbanisation and economic development. The main barrier will continue to be fear of geo-political issues and conflict (…)”, according to Savills.

Asia and the Pacific: “Asia goes two ways – half of Asia is strong. [while the other half continues to lose steam] (…) Prices continue to fall in five [China, Indonesia, Singapore, Taiwan, and Vietnam] of the ten Asian markets”, according to Global Property Guide. Moreover, “In a bid to limit house price growth, Asia Pacific stands out among global real estate markets as being particularly regulated. Price cooling measures in the form of stamp duty hikes and taxation has had the effect of reducing transaction levels in the prime markets, most notably in Hong Kong and Singapore. Prospects for future growth in the region will be significantly driven by China’s economy, which is currently slowing but likely to receive further stimulus and whose population will be a significant and growing market force for decades to come.”, writes Savills. A new IMF study finds that in Australia “(…) house prices are moderately stronger than consistent with current economic fundamentals, but less than a comparison to historical or international averages would suggest.” In New Zealand, “The resurgence in Auckland house prices over the past year has made the Reserve Bank increasingly concerned about the risks to financial stability. It is certainly on our ‘what keeps us awake at night’ list”,–said Grant Spencer (Deputy Governor) in a speech on Investors adding to Auckland Housing Market Risk. Finally, PropTiger takes a look at where India stands in Asia’s real estate market.

Europe: “Europe is no longer the weakest-performing world region, a title it has held for 15 consecutive quarters”, declares Knight Frank. The latest numbers from Eurostat shows that in the second quarter of 2015 “House prices (…) rose by 1.1% in the euro area and by 2.3% in the EU” compared to a year ago. However, the European Central Bank finds “that the recovery in house prices in the euro area has been rather muted thus far and appears to be weaker than the typical increase observed historically (…). At the same time, corrections of previous overvaluations, together with favorable income and financing conditions, suggest that the current recovery has a better chance of being sustained than the short-lived upturn observed relatively soon after the crisis. (…) the accompanying credit dynamics have thus far remained muted, limiting the build-up of systemic risks to the euro area financial system. The new macroprudential toolkit is also helping to mitigate possible risks in a targeted and granular way.” On other housing market indicators, “Housing supply (…) remained at the same level, with the exception of the number of building permits which increased in 2014. The rate of mortgage lending returned to growth in 2014, thus reversing the declining trend that began following the housing boom in the EU. Total outstanding lending in the EU increased”, according to the European Mortgage Federation.

In the Nordic countries, Roubini Global Economics points out that house prices continue to rise as well as household debt. It also says that “Given the dangerous links between house prices, household debt and bank credit, shocks deriving from higher interest rates, lower house prices and lower disposable income could generate GDP losses of more than 1% over a five-year period. This vulnerability highlights the need the Nordics to make use of risk-management measures (…) However, governments are reluctant to adopt these for fear of upsetting electorates that are already tilting toward anti-system parties.” Moreover, the Central Bank of Denmark says that “In the Copenhagen area, where house prices have risen considerably in recent years, housing taxes have not increased correspondingly. Relative to the property values, homeowners are currently paying substantially less in Copenhagen than in other parts of Denmark, where price increases have been more moderate. (…) there is a risk that price increases have become self-reinforcing, meaning that they are very much determined by expectations of even higher prices in the future.”

Western Hemisphere: “The U.S. housing recovery is gaining traction (…) Canadian home sales and pricing are proving resilient (…) Mexico’s fledgling housing recovery is supported by wide-reaching market reforms aimed at spurring new residential development and broadening access to mortgage lending. Elsewhere in the Americas, property markets in Chile, Colombia and Peru are showing positive but more muted momentum, consistent with a softening in regional growth dynamics. Housing conditions continue to deteriorate in Brazil, with a prolonged recession and rising unemployment compounded by high interest rates and rising inflation”, according to Scotiabank. Brazil is at the end of a cycle (…) In real terms house prices fell 3.65% (…) Average price growth has been slowing down from 18.7% in 2012, 12.3% in 2013, down to 10.2% in 2014”, notes Global Property Guide. Meanwhile, “Costa Rica´s higher-end property market continues to grow rapidly as foreign homebuyers flock in” (Global Property Guide).

Other related developments

Housing affordability: a recent survey finds that “Europe is pessimistic about the opportunities for first-time buyers, with a majority believing that the housing crisis is getting more acute and that society would benefit if prices fell”, according to ING International Survey on Homes and Mortgages.

Impact of low oil prices on house prices: On the impact of the ongoing oil price slump, FannieMae makes a very interesting comparison of current house price risks in oil-producing states in the U.S. to those in the 1980s oil bust. It says: “Real oil prices peaked in 1980, followed by a near-decade-long decline. This included a crash in late 1985. A clear pattern exists. Real oil prices first fell, then with a time lag, oil industry employment declined (along with royalties and state and local tax receipts). This in turn weakened the broader labor market and eventually drove house prices downward as demand fell (…) [The FannieMae study finds that] home price weakness will not be as severe in most oil patch areas as it was in the 1980s. Still, the three states with most risk of a decline are WY, ND, and AK. (…) The resilience of shale oil production will be key. Thus far, in the short run, it has remained relatively viable, and while industry employment has been declining, losses are still modest relative to the 1980s. States with higher oil industry concentrations are showing comparatively weaker general labor markets. Although there is no evidence yet of negative house price effects, given the historical time lags (…),” these developments will need to be followed very closely. In Australia, homes in some mining “towns have lost almost three quarters of their value after the country’s resource boom peaked and commodity prices plunged,” according to CBRE Group Inc.

Impact of interest rates on house prices: On the impact of an increase in monetary policy on house prices, John Williams (Federal Reserve Bank of San Francisco) reaches two conclusions: “First, monetary policy actions have sizable and significant effects on house prices in advanced economies. That is, an increase in interest rates tends to lower real (inflation-adjusted) house prices. Second, this reduction in house prices comes at significant costs in terms of reductions in real gross domestic product and inflation. A typical estimate is that a 1% loss in GDP is associated with a 4% reduction in house prices. This implies a very costly tradeoff of using monetary policy to affect house prices when macroeconomic and financial stability goals are in conflict.” Moreover, “An important channel for monetary policy transmission is through mortgage markets. (…) the effects of an interest rate lift-off, from the zero lower bound, on homeowners depend on three factors: the prevalent mortgage type in the economy (fixed or adjustable rate), the speed of the lift-off, and the inflation rate during the lift-off. This channel of transmission suggests that if the purpose of the lift-off is to normalise nominal interest rates without derailing the recovery, the Federal Reserve Bank and the Bank of England should wait until the economies show convincing signs of inflation taking off. Furthermore, the lift-off should be gradual and in line with inflation”, according to a VoxEU column by Carlos Garriga, Finn Kydland, and Roman Šustek.

Macroprudential and Monetary Policies: In October, the Federal Reserve Bank of Boston and the Bank of Finland held separate conferences on this topic. Also, in a speech on Evaluation and macroprudential policy, Claudia Buch, Deputy President of the Deutsche Bundesbank said that “The available evidence [on macroprudential policy] is very sparse; it is often no more than cross-sectional analyses across different countries derived from short time series.” In another speech by Stefan Gerlach—Deputy Governor at the Central Bank of Ireland—said that “Earlier this year, the Central Bank of Ireland brought in macro prudential measures for residential mortgage lending. The motivation for doing so was to limit lending of the type that was shown to be particularly risky in the financial crisis, and thereby enhance the resilience of both households and banks. (…) It is too soon to assess what the impact of these measures on the economy has been, as only a small number of loans drawn down have been subject to these rules and as banks may have had some initial difficulties implementing the rules. In fact, the banks have not yet been required to report their compliance with the rules. However, we have seen some evidence that house price expectations have declined, suggesting that the speculative element of the property market has become less important, as buyers recognise that risky mortgage lending will not be allowed to fuel another devastating housing bubble.”

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts