Monday, June 8, 2015

House Prices in Luxembourg

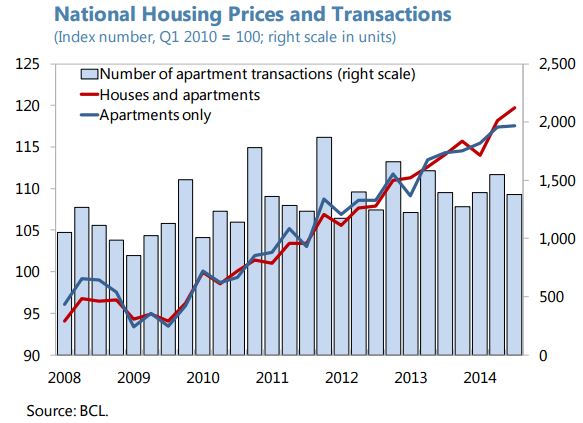

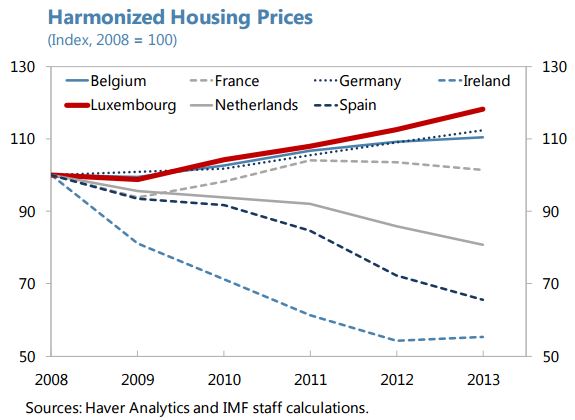

“(…) there is some risk that a protracted period of low interest rates could spawn a credit fueled housing bubble (…). Credit to households has been growing by about 7 percent y/y, yet household debt seems managable (data vary by source). If a bubble were to develop, housing prices could correct, compressing household consumption or triggering defaults and possibly disrupting credit to the economy. With rising housing prices spanning decades, reflecting population and job growth combined with zoning and other rules that constrain supply, there seems no immediate reason to expect a correction, although pockets of risk are possible,” according to the IMF’s new report on Luxembourg.

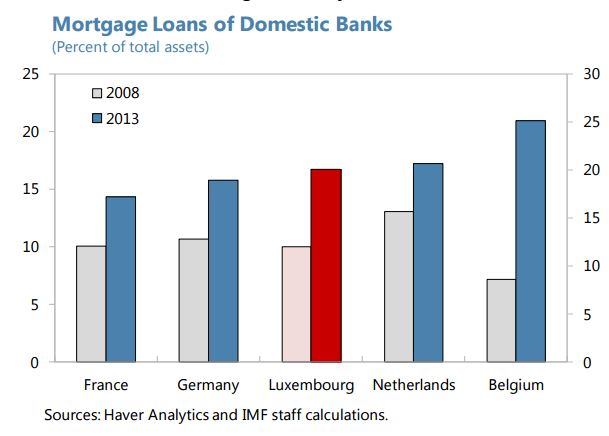

The report also says that “Growth in the housing exposures of locally active banks warrants continued monitoring and readiness to deploy additional macroprudential tools if needed. Housing prices and mortgage lending continue to rise, raising concentration risks. Some households could become overstretched. In late 2012, the CSSF took positive steps to dampen these risks, advising banks to limit loan-to-value (LTV) ratios to 80 percent and imposing higher risk weights on mortgages with higher LTV ratios. Staff advised the authorities to step up data collection on property lending, and to prepare appropriately targeted macroprudential tools for deployment if needed.”

Posted by at 5:54 PM

Labels: Global Housing Watch

Subscribe to: Posts