Thursday, October 9, 2014

Seven Questions on the Global Housing Markets

The housing sector satisfies an essential need. Housing is an important component of investment and in many countries housing makes up the largest component of wealth. At the same time, housing booms and busts have often been detrimental to financial stability and the real economy. This article describes the state of global housing markets—including the role that foreign investors are playing—and policy responses to manage housing booms.

Question 1. What is the state of global housing markets today?

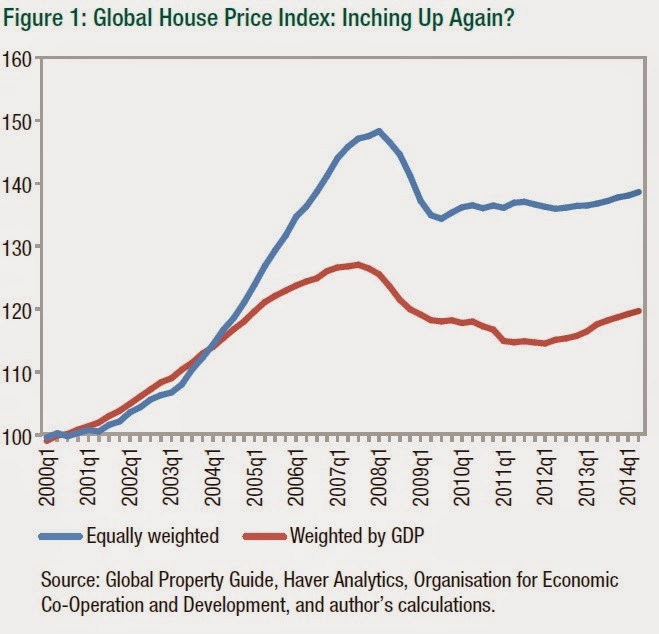

After sharp declines during the Great Recession, the IMF’s Global House Price Index has been inching up over the past two years (Figure 1). During the past year, house prices increased in about half the advanced economies included in this index and about two-thirds of the emerging economies.

In a number of countries—Canada, many countries in the Asia-Pacific region, and many Scandinavian countries—the price of houses have increased steadily after a brief correction during the Great Recession. For many OECD countries, house price-to-income and house price-to-rent ratios remain above historical averages—this is true for example in Australia, Belgium, Canada, Norway, and Sweden. While this provides a broad indication of possible housing market valuations, one should be wary about assessing overvaluation from this evidence alone. Judgments about housing valuation require supplementary information (e.g., credit growth, household indebtedness, lender characteristics, and the method of financing) as well as knowledge about within-country developments (e.g., in some cases the house price increases may be concentrated in particular cities or regions) and institutions.

For instance, Belgium stands out for its high ratios of house prices to rents and incomes. But, on the basis of a more detailed analysis of the supplementary factors, an IMF staff report concluded that “risks of a sharp correction of real estate prices appear contained.” Among other countries, IMF assessments point to modest overvaluations in Canada, Israel, Norway, and Sweden. In many cases, the housing price booms are restricted to particular cities (as in Australia and Germany, for example) or reflect supply constraints (as in New Zealand).

Question 2. How important are foreign investors in global housing markets?

Countries vary in the degree to which they permit foreign investment in their housing markets. According to a survey by the Association of Foreign Investors in Real Estate, the countries with the “most stable and secure” environments for real estate investments for foreign investors are the following: United States, Canada, Germany, Australia, United Kingdom, Sweden, Denmark, Switzerland, France, Japan, and Austria.

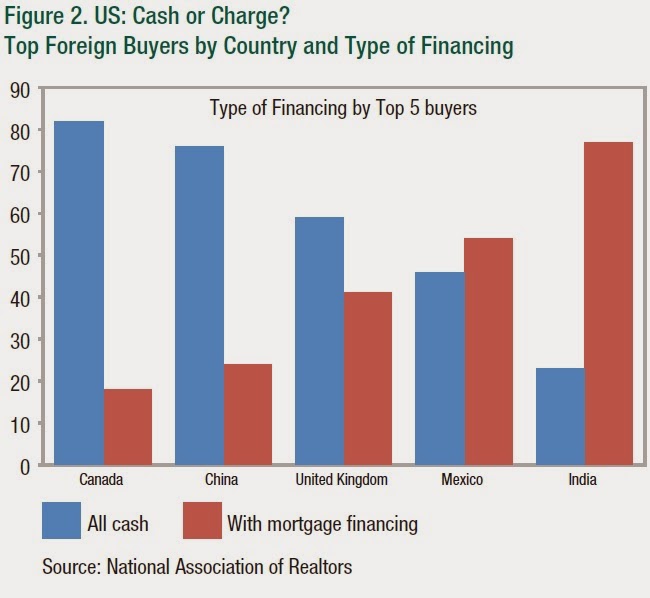

For the United States, the dollar level of international sales is estimated at about 7 percent of the total existing homes sales market of $1.2 trillion. International buyers from five countries—Canada, China, Mexico, India, and the United Kingdom—accounted for half of these transactions. In Australia, foreign residential investment has remained at most around 5–10 percent of the value of dwelling turnover and is concentrated in new, high-priced dwellings in inner-city areas of Sydney and Melbourne. For the United States, there is also survey data on the type of financing (cash vs. mortgage financing) preferred by foreign investors (Figure 2). Buyers from Canada and China rely largely on cash financing, whereas buyers from India use mortgage financing.

Question 3. Is there evidence that foreign investors are boosting house prices?

Industry sources and media discussion often ascribe the strength in housing markets in some countries to the emergence of a global investor class that pushes up prices in particular cities, particularly in high-end segments; over time, this is said to impart a boost to prices in other cities as well.

However, a casual look at the performance of luxury residential markets in a number of global cities does not substantiate this view. Patterns of house price developments in these markets during the past five years are quite varied: an upward trend (Beijing, Shanghai); an upward trend after a correction during the Great Recession (London, Hong Kong SAR, Dubai); flat (Singapore, Tokyo); a downward trend (a steady one in Moscow since 2008; more recent in Paris and Geneva; Sydney since 2008 with a recent uptick). The range of correlation among house price growth in these markets is quite wide, from values of -0.7 and -0.8 at one end to over 0.9 at the other. The highest positive correlations are among the cities in China, whereas the largest negative correlations are with Singapore and Geneva.

For the United States, the National Association of Realtors (NAR) tracks the cities that have been of major interest to foreign investors over the past year as revealed through searches on realtor.com. House price growth over the past year in these cities has been higher than in the other cities that are part of the Case-Shiller house price index (14 percent increase compared with 8 percent). In Australia, there is some indication of a price impact from foreign investors, particularly where there are rigidities in housing supply. But the price impact has not been felt in the parts of the market where Australia’s first home buyers are typically concentrated.

In short, there is little evidence thus far of foreign investors having more than a local impact on house prices.

Question 4. What impact do housing markets have on economic and financial stability?

As noted by Zhu (2014) food, clothing, and shelter are traditionally thought of as basic needs; therefore, the housing sector satisfies an essential need. Housing is an important component of investment and in many countries housing makes up the largest component of wealth. The majority of households tend to hold wealth in the form of their homes rather than in financial assets. In France, for example, less than a quarter of households own stocks, but nearly 60 percent are homeowners. Housing also plays other key roles; for instance, mortgage markets are important in the transmission of monetary policy. Adequate housing can also facilitate labor mobility within an economy and help economies adjust to adverse shocks. Hence, a well-functioning housing sector is critical to the overall health of the economy.

At the same time, housing booms and busts have quite often been detrimental to both financial stability and the real economy. Many major episodes of banking distress have been associated with boom-bust cycles in property prices. Of the nearly fifty systemic banking crises in recent decades, more than two thirds were preceded by boom-bust patterns in housing prices. Housing price booms can be particularly toxic when there is a coincidence between the housing boom and the rapid increase in leverage and exposure of households and financial intermediaries. During the global financial crisis, nearly all the countries with “twin booms” in real estate and credit markets—21 out of 23 countries—ended up suffering from either a financial crisis or a severe drop in GDP growth relative to the country’s pre-crisis performance. In contrast, of the seven countries that experienced a real estate boom but not a credit boom, only two went through a systemic crisis and these countries, on average, had relatively mild recessions. Even when housing busts do not have a large financial stability impact, they can affect the real economy. Recessions in OECD countries are more likely given a house-price bust. Such recessions also tend to be much deeper and generate more unemployment than normal recessions.

In sum, there is abundant evidence that housing cycles can be a threat to financial and macroeconomic stability. The cost of resolving housing crises can be very high—in the case of Ireland, for instance, government bailouts of banks from the housing collapse amounted to 40 percent of the country’s GDP. Hence it is crucial to keep an eye on current housing market developments to keep them from going through another boom-bust cycle.

Question 5. What policies can be used to manage housing booms?

Regulation of the housing sector involves a complex set of policies. The noted economist Avinash Dixit suggested we use the acronyms MiP, MaP, MoP to remind ourselves of the set of policies. MiP stands for microprudential policies, which aim to ensure the resilience of individual financial institutions. Such policies are necessary for a sound financial system but may not be sufficient. Sometimes, actions suitable at the level of individual institutions can destabilize the system as a whole. Hence we need not just MiP but also MaP, that is, macroprudential policies aimed at increasing the resilience of the system as a whole. Along with micro and macroprudential policies, we need MoP—monetary policy. Using policy interest rates is usually considered a blunt tool for containing house price booms. But as noted earlier, housing booms have often coincided with a generalized private credit boom. This suggests that monetary policy could be an important tool in many cases in support of macroprudential policies. However, at the moment, policy interest rates in many countries have to remain low to support economic recovery.

Question 6. What are the main macroprudential tools to manage housing booms?

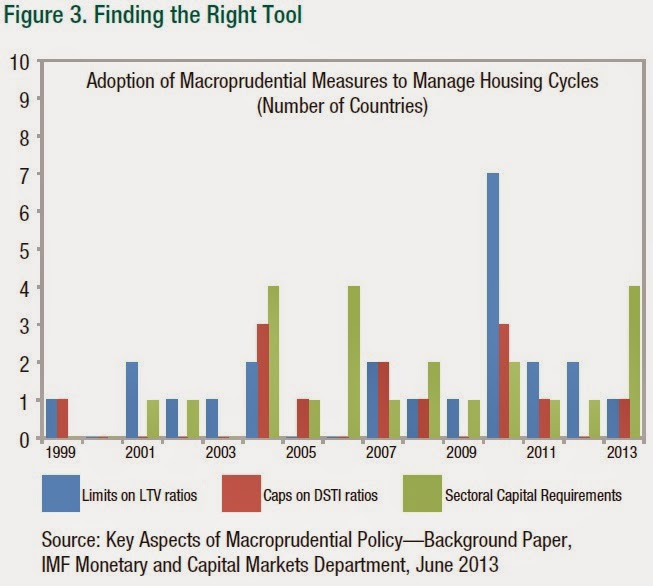

The main macroprudential tools that have been used to contain housing booms are limits on loan-to-value (LTV) ratios and debt-service-to-income (DSTI) ratios and sectoral capital requirements (Figure 3). Limits on LTV ratios cap the size of a mortgage loan relative to the value of a property, in essence imposing a minimum down payment. Limits on DSTI ratios restrict the size of a mortgage loan to a fixed multiple of household income. The hope is to thereby contain unaffordable increases in household debt.

Such limits have long been in use in some economies. For example, Hong Kong SAR has operated an LTV cap since the early 1990s and introduced a DSTI cap in 1994. In Korea, LTV limits were introduced in 2002 and DSTI limits in 2005. During and after the global financial crisis, more than twenty advanced and emerging economies all over the globe have followed the example of Hong Kong SAR and Korea.

Another macroprudential tool is to impose stricter capital requirements on loans to a specific sector such as real estate. This forces banks to hold more capital against these loans, discouraging heavy exposure to the sector. In many advanced economies such as Ireland and Norway, capital adequacy risk weights were increased on mortgage loans with high LTV ratios. Sectoral capital requirements have also been used in a number of emerging markets such as Estonia, Peru, and Thailand.

Question 7. What do we know about the effectiveness of these macroprudential policies?

Up to now, the evidence suggests that limits on LTV and DSTI rations are somewhat effective in cooling off both house prices and credit growth in the short run. They are able to break the financial accelerator mechanism that otherwise leads to a positive two-way feedback between credit booms and housing booms. But more fine tuning of these measures is needed. Macroprudential measures need to take into account the ability of market participants to circumvent some of the limits on leverage. In some countries, such as in Canada, LTV limits usefully distinguish between owner-occupied versus investor mortgages.

With regard to sectoral capital requirements, evidence suggests that while this tool increases resilience from additional buffers, its ability to curb credit growth is mixed. Some IMF research suggests that higher capital requirements on particular groups of mortgage loans have some success in curbing house-price growth in countries like Bulgaria, Croatia, Estonia, and Ukraine. There are a number of reasons why higher capital requirements may be less effective in containing credit growth. First, when banks hold capital well above the regulatory minimum, lenders may not need to make any change in response to increases in risk weights. This often happens during housing booms when policymakers hope the tool will be most effective. Second, when lenders compete intensely for market share, they may internalize the costs of higher capital requirements rather than impose higher lending rates.

Macroprudential tools may also not be effective to target housing booms that are driven by the shortage of housing or by increased housing demand from foreign cash inflows that bypass domestic credit intermediation—as noted earlier, some foreign buyers use cash rather than mortgages to finance their purchases. In such cases, other tools are needed. For instance, stamp duty has been imposed to cool down rising house prices in Hong Kong SAR and Singapore. Evidence shows that this fiscal tool did reduce demand from foreigners who were outside of the LTV and DSTI regulatory perimeters. In other instances, high house prices could reflect supply bottlenecks, and hence the effectiveness of demand-focused instruments may be limited. In such cases, the mismatches should be fundamentally addressed by measures to increase the supply of housing.

Posted by at 4:59 PM

Labels: Global Housing Watch

Subscribe to: Posts