Showing posts with label Macro Demystified. Show all posts

Wednesday, April 6, 2022

Globalisation and the effective taxation of capital versus labour

From VoxEU post by Pierre Bachas, Matthew Fisher-Post, Anders Jensen, and Gabriel Zucman:

“Globalisation has wide-ranging effects on tax systems. This column uses a new dataset of taxes on capital and labour across countries and time to assess these dynamics. The authors document a global convergence of average effective labour and capital taxes over time, as labour taxes have increased and capital taxes fallen. However, the large fall in capital taxation in developed economies contrasts its gradual rise in developing economies, albeit from a low base. This trend is consistent with evidence suggesting the causal effect of trade integration on the tax capacity of developing economies.

Social scientists have for a long time been cognisant that globalisation may have deep impacts on tax systems. In particular, economists have conjectured that increased openness pushes governments to reduce taxes on mobile factors of production and recover the revenue shortfalls by increasing taxes on immobile factors (Bates et al. 1985, Rodrik 1997). In this view, globalisation erodes the taxes effectively paid by capital owners, shifting the tax burden towards workers. The fall of statutory tax rates on corporate income worldwide (IMF 2019), and evidence that globalisation reduces income tax rates on mobile high-income earners at the expense of median-income workers (Egger et al. 2019) support this hypothesis. Prior work has focused on the recent experience of high-income countries, but how has cross-border integration affected the relative taxation of labour and capital historically and globally? And which countries have been most affected by the erosion of effective capital taxation, and why? Answering these questions is critical to shed light on the macroeconomic effects and long-run social sustainability of globalisation.

A new dataset to measure the effective taxation of capital and labour globally since the 1960s

Assessing the extent to which globalisation has affected tax systems requires a global and long-run dataset on the taxation of capital and labour. In Bachas et al. (2022), we assemble data on effective tax rates (ETRs) on labour and capital covering 150 countries and half a century. Constructed following a common methodology, these series offer a worldwide, historical, and comparative perspective on the evolution of tax structures.1

ETRs capture all taxes paid: on corporate income, individual income, payroll, property, inheritance, and consumption. They then assign each type of tax revenue to capital, labour or a mix of the two and divide these by their respective capital and labour flows in national accounts (Mendoza et al. 1994).2 ETRs thus make it possible to estimate total tax wedges – for instance, the gap between what it costs to employ a worker and what the worker receives – and how these wedges vary internationally and over time. Since capital income is always more concentrated than labour income, the relative taxation of the two factors of production is closely linked to the overall progressivity of the tax system.”

Continue reading here.

From VoxEU post by Pierre Bachas, Matthew Fisher-Post, Anders Jensen, and Gabriel Zucman:

“Globalisation has wide-ranging effects on tax systems. This column uses a new dataset of taxes on capital and labour across countries and time to assess these dynamics. The authors document a global convergence of average effective labour and capital taxes over time, as labour taxes have increased and capital taxes fallen. However, the large fall in capital taxation in developed economies contrasts its gradual rise in developing economies,

Posted by at 8:01 AM

Labels: Macro Demystified

Wednesday, March 23, 2022

Ukraine’s economic future

From Noahpinion:

“Some people are going to see this post as premature. Though the Ukrainians have turned the tide against the Russian invaders, the outcome is still in doubt, and much destruction still lies in the future. But at this point it seems likely that a country called Ukraine will survive this conflict, with most or all of the territory it possessed before Putin invaded. So it’s time to start thinking about reconstruction and growth after the war’s end.

Certainly after the shooting stops, the first order of business — and the task of several years — will be to rebuild the parts of the country torn down by Putin’s assault. Cities like Mariupol and Kharkiv are being reduced to rubble, much of the country’s infrastructure is being torn up, and about a quarter of the entire population has been displaced. It took Japan and Germany both slightly over a decade after the end of WW2 to reach the level of income they had enjoyed before the war. Ukraine hopefully won’t be in quite such bad shape after this conflict, but this isn’t going to be the kind of thing a country bounces back from in 1 or 2 years.

Ukrainians will work very hard to rebuild their country, but they’re going to need help. And given the U.S. and Europe’s copious military assistance, it seems likely that they’ll offer rebuilding assistance as well. In fact, the EU has just started setting up a postwar reconstruction fund, and the U.S. has already spent $13 billion helping the Ukrainians. Both the U.S. and EU leadership know that they can’t afford to have a weak, economically backward Ukraine as the first line of defense against a newly malevolent Russia, and the Ukrainians’ cause has resonated deeply with the U.S. and EU populations alike. So expect copious economic aid to flow for at least a decade.

But aid alone doesn’t build a country into an economic powerhouse. We Americans tend to think that the Marshall Plan was how Germany rebuilt its economy after WW2, but in fact this only provided a small initial kick — most of West Germany’s economic rise in the mid and late 20th century happened via its own investment and industrialization, helped by favorable trade treaties with allied countries. Ditto for Japan.

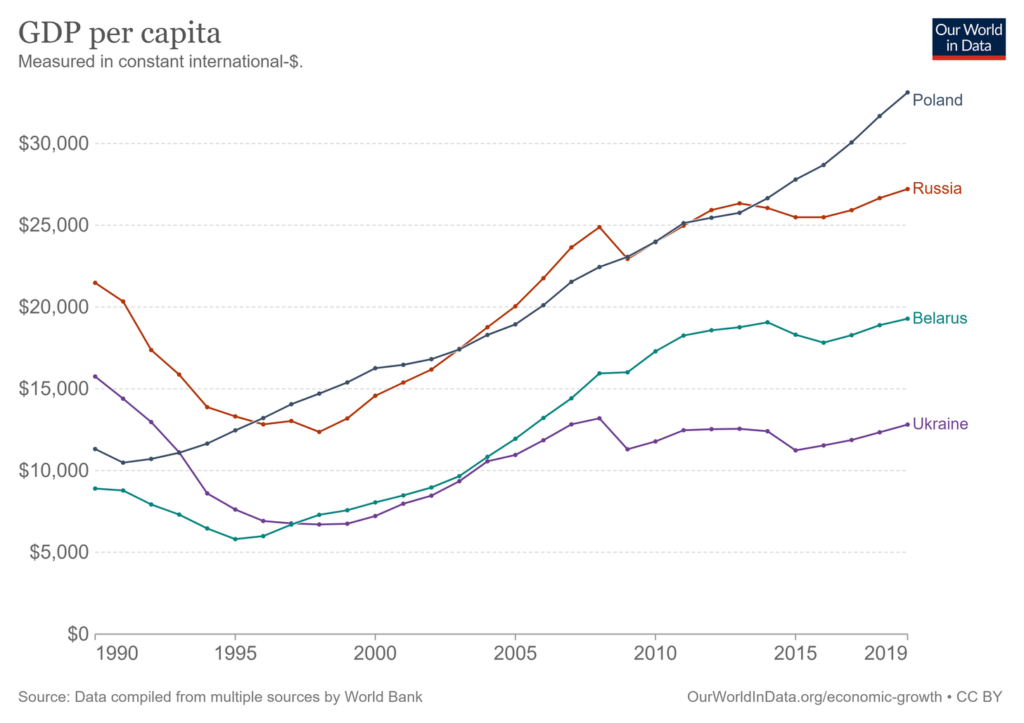

And Ukraine really needs to build itself into an economic powerhouse. Russia has four times Ukraine’s population; having a higher GDP than a sanctions-stricken postwar Russia would help Ukraine even up the balance of power a bit. Remember that before the war, Ukraine’s economy had languished for three decades, with living standards well below those of Poland, Russia, or even Belarus:”

Continue reading here.

From Noahpinion:

“Some people are going to see this post as premature. Though the Ukrainians have turned the tide against the Russian invaders, the outcome is still in doubt, and much destruction still lies in the future. But at this point it seems likely that a country called Ukraine will survive this conflict, with most or all of the territory it possessed before Putin invaded. So it’s time to start thinking about reconstruction and growth after the war’s end.

Posted by at 6:30 AM

Labels: Macro Demystified

Saturday, March 19, 2022

Sanctions, energy prices, and the world economy

From Econbrowser:

Posted by at 7:43 AM

Labels: Energy & Climate Change, Macro Demystified

Tuesday, March 15, 2022

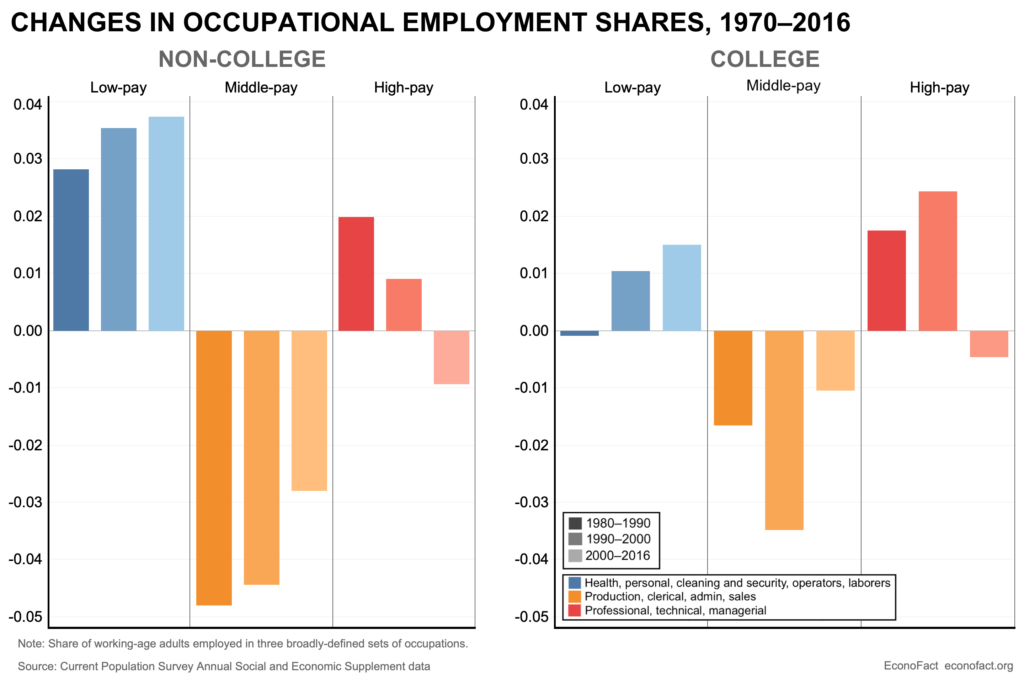

The Shrinking Share of Middle-Income Jobs

From EconoFact:

“The Issue:

Over the past four decades, less-educated workers, particularly non-college men, have experienced an actual fall in their real earnings (that is, after adjusting for inflation). An important reason for this decline in the earnings among low-income workers is the shifting structure of occupations, with a hollowing-out of what had been middle-income jobs. This is especially true in urban and metropolitan areas, places where there had been good job opportunities for those without a college education but, increasingly, the jobs available to those with a high school education in these places are in low-paid occupations with little opportunity for upward mobility.

The Facts:

- Rising wage inequality is a well-documented characteristic of the U.S. labor market over the past 40 years; but such divergence in earnings was not a feature of the preceding decades. The post-World War II period can be divided into three eras with respect to the distribution of wages. The period from immediately after World War II until 1972 was a time when wages were rising evenly for people with all levels of education. In contrast, the period that began with the first oil shock in 1973 through the end of the 1970s saw inflation-adjusted earnings stagnate across the board. Subsequently, beginning in 1980 and continuing to the present there has been rising wage inequality, with wages rising robustly for the most educated and falling, in real terms, for the least educated. This is especially striking because the supply of highly-educated workers has increased while that of less-educated workers has declined; the share of hours worked by those without a college degree fell from 75 percent in 1963 to less than 40 percent in 2017 while over the same period the share of hours worked by those with a bachelor’s or post-college degree rose from less than 15 percent to more than 35 percent.

- An important source of these shifts in wages and hours is the hollowing out of middle-income jobs. While there are a range of reasons for the decline in wages and hours worked for those with less than a college education (including eroding union power, rising trade in manufacturing goods from low-labor-cost countries, and falling real values of minimum wages), an important reason that has not had as much attention is the decline in jobs that had provided middle-class wages for those with less than a college education. The shrinking share of these middle-income jobs appears as a “barbell effect” with the decline of middle-paid jobs contrasted by the rise in the employment share for both lower- and higher-paid jobs (see chart). Employment can be sorted into three broadly defined sets of occupations: those with typically low pay and education requirements that require little specialized skills or training (health aids and personal services, cleaning and security, and operators and laborers); middle-paid occupations that do not necessarily demand a four-year college degree but do require specialized skills (production workers, office/administrative workers, and sales workers); and high-paid occupations that typically require a four-year degree (technicians, professionals, and managers). In 1980, non-college workers were evenly split between low- and medium-paid occupations (at 42 percent and 43 percent, respectively) and the remaining one-seventh of workers without college degrees were in traditionally high-paid occupations. By 2016, the share of non-college educated workers in mid-pay occupations had fallen to 29 percent, with about 12 of the overall 14 percentage point decline representing a shift to the low-paid category and less than a 1.5 percentage point increase in the high-pay category. Over this same period, there was a more modest barbell effect for college-educated workers, with those in the mid-pay occupations declining from 27 to 20 percent, those in high-pay occupations rising from 57 to 61 percent, and those in low-paying occupations rising from 16 to 19 percent.

- There are technological, global and institutional reasons why this “barbell effect” was concentrated among workers in urban and metropolitan areas. In the 1950s and 1960s, workers in urban areas who did not have college degrees disproportionately held middle-education, middle-income, blue-collar production jobs and white-collar office, administrative and clerical jobs as compared to workers in suburban and rural areas. These jobs involved close collaboration with more highly-educated professional, managerial and technical workers who oversaw factories and offices. This collaboration benefited workers holding these middle-income jobs since their value to their companies was enhanced by high-education coworkers. But starting in the 1970s, the demand for mid-education urban workers declined due to rising automation in factories, greater use of computers and information technology in offices, and greater pressure from international trade. Workers without a college degree moved from middle-income occupations to those that traditionally require less education and offer lower wages – and because middle-income jobs for those without a college degree were more prevalent in urban and metropolitan areas, this had a proportionally bigger effect in those places. “

Continue reading here.

From EconoFact:

“The Issue:

Over the past four decades, less-educated workers, particularly non-college men, have experienced an actual fall in their real earnings (that is, after adjusting for inflation). An important reason for this decline in the earnings among low-income workers is the shifting structure of occupations, with a hollowing-out of what had been middle-income jobs. This is especially true in urban and metropolitan areas, places where there had been good job opportunities for those without a college education but,

Posted by at 7:22 PM

Labels: Macro Demystified

Sunday, March 13, 2022

The Wobbly Economy: Global Dynamics with Phase and State Transitions

Source: NBER Working Paper

Standard macroeconomic models that explain business cycles in the economy, like the real business cycle or Solow model, usually propound the existence of a momentary economy-wide equilibrium, a long-run steady-state equilibrium, and a unique convergent path to arrive at that steady-state equilibrium. However, in this paper for NBER, economists Tomohiro Hirano and Joseph Stiglitz demonstrate using the life cycle model with production a situation where multiple equilibria can exist. They suggest that this multiplicity of equilibria can give rise to “wobbly macro-dynamics”, i.e. a dynamic situation for the economy wherein it can bounce around infinitely without converging, all the time doing so in ways perfectly consistent with rational expectations. They further go on to add, “this wobbly macro-dynamics is driven by people’s beliefs or sentiments, and doesn’t even have regular periodicity”. “As a result, laissez-faire market economies can be plagued by repeated periods of instabilities, dynamic inefficiencies, and unemployment.”

Source: NBER Working Paper

Standard macroeconomic models that explain business cycles in the economy, like the real business cycle or Solow model, usually propound the existence of a momentary economy-wide equilibrium, a long-run steady-state equilibrium, and a unique convergent path to arrive at that steady-state equilibrium. However, in this paper for NBER, economists Tomohiro Hirano and Joseph Stiglitz demonstrate using the life cycle model with production a situation where multiple equilibria can exist.

Posted by at 1:57 PM

Labels: Macro Demystified

Subscribe to: Posts