Showing posts with label Macro Demystified. Show all posts

Wednesday, April 20, 2022

Figuring out efficient unemployment

From a VoxEU post by Pascal Michaillat and Emmanuel Saez:

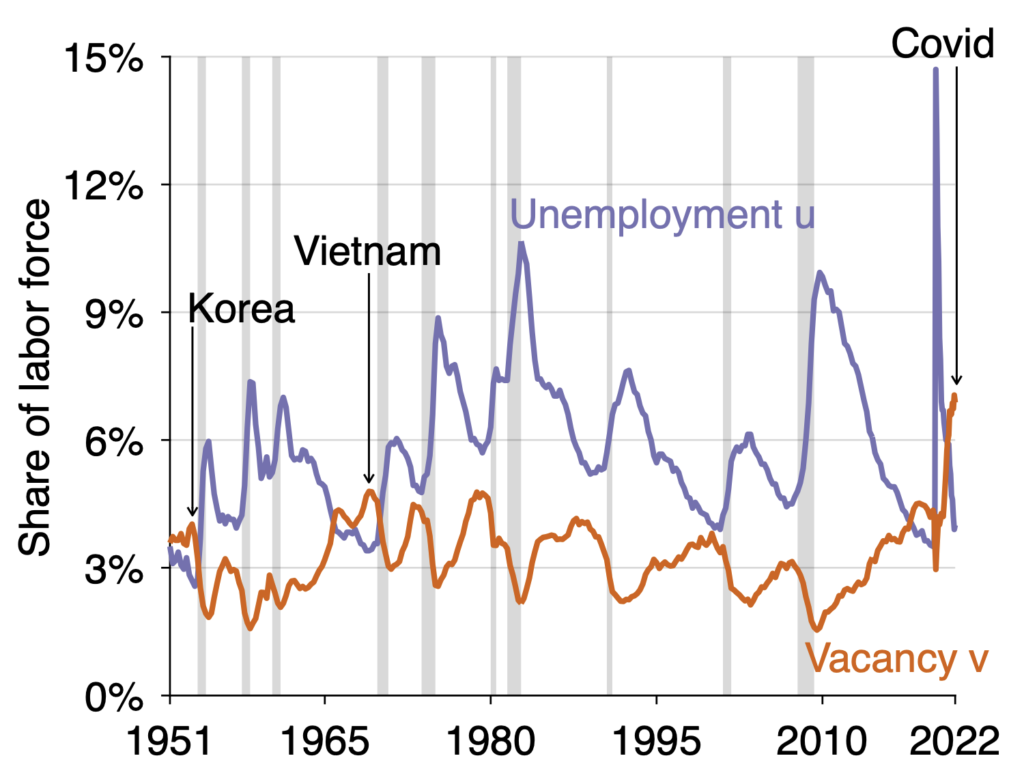

“Empirically, the unemployment rate is inversely related to the vacancy rate. Furthermore, servicing a job opening costs about as much as one job in terms of resources. This column shows that the labour market minimises waste when the unemployment rate equals the vacancy rate. It is too slack when the unemployment rate is higher and too tight when it is lower. Consequently, the efficient unemployment rate is simply given by the geometric average of the current unemployment and vacancy rates. At the beginning of 2022, the US labour market is excessively tight, and tighter than at any point since 1951.

Knowing whether an economy is too slack or at risk of overheating is crucial for macroeconomic policy. Economists generally look at price inflation, GDP level relative to potential, and the unemployment rate to assess, this but each measure has issues as can be seen when looking at the current US economy coming out of the Covid-19 crisis.1 An increase in inflation, as experienced in 2021, can be a marker of an overheating economy, but inflation can also increase due to temporary disruptions such as supply chain issues. Assessing whether GDP is below or above potential is challenging as a crisis like Covid-19 also affects the productive potential of the economy. The unemployment rate is 3.6% as of March 2022, not yet lower than just before Covid-19 when the economy did not show signs of overheating.

In this column, we propose a very simple rule to assess whether the economy, or more precisely the labour market, is too tight or too slack: are there more job openings than there are unemployed workers? This simple rule has intuitive appeal. If somehow job seekers were to be matched to job openings, would there be excess job openings, suggesting an economy with a shortage of willing workers (i.e. an overly tight labour market), or would there be excess job seekers left, suggesting an economy with too few jobs (i.e. an overly slack labour market)? It turns out that this simple intuitive rule can also be justified using the modern matching model that economists use.2 This reconciles economic theory with the widely scrutinised job-seeker-per-job-opening statistic.3

The Beveridge curve

William Beveridge first noted in 1944 that the number of job openings and the number of job seekers in the UK move in opposite directions: When the economy is depressed, there are lots of job seekers and few job openings. Conversely, when the economy is booming, there are few job seekers and many job openings. This relationship has therefore been dubbed the ‘Beveridge curve’ and holds remarkably well in the US as well.4 Figure 1 depicts the time series of the unemployment rate u (all job seekers divided by the labour force which includes all workers and job seekers) and the vacancy rate v (all job openings divided by the same labour force) since 1951. The figure shows clearly that u and v move in opposite directions.”

Figure 1 The US unemployment and vacancy rates since 1951

Continue reading here.

From a VoxEU post by Pascal Michaillat and Emmanuel Saez:

“Empirically, the unemployment rate is inversely related to the vacancy rate. Furthermore, servicing a job opening costs about as much as one job in terms of resources. This column shows that the labour market minimises waste when the unemployment rate equals the vacancy rate. It is too slack when the unemployment rate is higher and too tight when it is lower.

Posted by at 11:28 AM

Labels: Macro Demystified

Thursday, April 14, 2022

World Wealth: Human, Physical, and Natural

From the Conversable Economist:

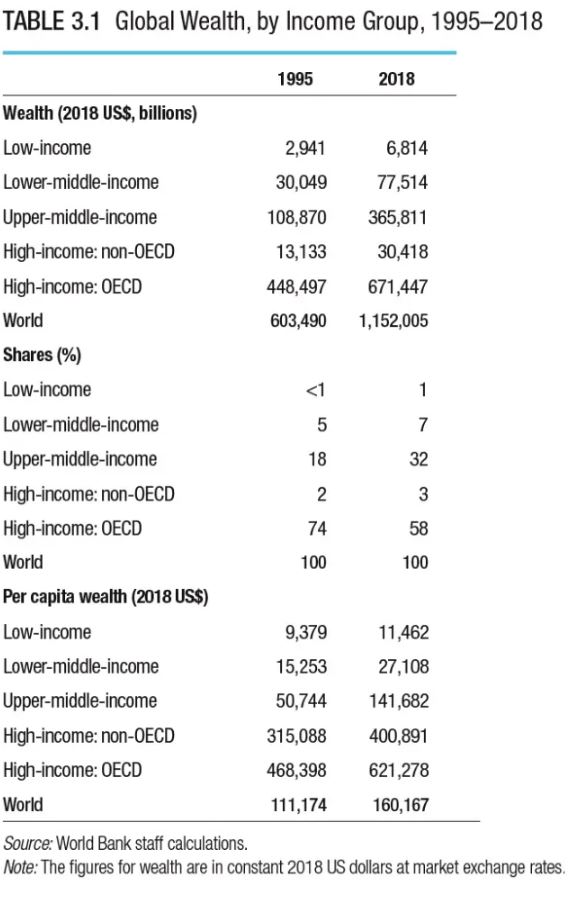

“The wealth of a society is so much more than the value of houses, or the stock market, or retirement accounts. Wealth broadly understood should also include endowments of nature, ranging from wilderness to oil wells, as well as the human capital embodied in the education and skills of its people. Every few years, the World Bank takes on the task of measuring the world’s wealth in these broader ways. The most recent set of estimates appear in The Changing Wealth of Nations 2021 : Managing Assets for the Future.

Just to be clear, wealth represents an accumulation over time. This is different from GDP, which is the amount produced in a given year. Thus, world GDP in 2018 was about $86 trillion, but world wealth as estimated in this report was 13 times bigger at $1,152 trillion. Here are some estimates from “Chapter 3: Global and Regional Trends in

Wealth, 1995–2018,” by Glenn-Marie Lange, Diego Herrera, and Esther Naikal.

Here is how wealth was distributed around the world between countries of different income levels (I have left out some intermediate years in the table):”

From the Conversable Economist:

“The wealth of a society is so much more than the value of houses, or the stock market, or retirement accounts. Wealth broadly understood should also include endowments of nature, ranging from wilderness to oil wells, as well as the human capital embodied in the education and skills of its people. Every few years, the World Bank takes on the task of measuring the world’s wealth in these broader ways.

Posted by at 1:17 PM

Labels: Macro Demystified

Wednesday, April 13, 2022

GDP vs. GNP

From Marginal Revolution:

“As a metric of how well economes are doing, gdp is underrated, as I argue in my latest Bloomberg column. Here is one bit:

If a nation has a lot of foreign direct investment, as does Ireland, GDP will exceed GNP by a considerable amount. According to the Irish government, the country’s GDP is about 370 billion euros. Its GNP is less than 300 billion euros. The difference in GDP and GNP is largely accounted for by the outflow of profits to foreign-owned multinationals.

This isn’t just a story about Ireland. Many other nations have had significant differences between their GDP and GNP, including many developing nations and, at times, Singapore.

The conventional wisdom is that GNP is the proper measure of living standards, because domestic citizens do not have claims on the profits of foreign multinationals. That isn’t wrong, but it is also an incomplete answer. When it comes to the future prospects of a country, GDP is a better indicator. Countries that have a high ratio of GDP to GNP are especially promising, though there are some caveats.

A relatively high GDP is a sign that a large number of foreign companies view the future of the domestic economy as bright. They are “putting their money where their mouth is.”

In the case of Ireland, the country is now the only member of the European Union in which English is the main language not only for business but also for schools and public life. Foreign investors are drawn by that fact. They also see that Ireland is relatively underpopulated, and appears to be receptive to absorbing talented foreign immigrants. Furthermore, Ireland is ruled by mainstream parties and seems largely unaffected by the populism and nativism that are creating problems elsewhere in Europe.

All these realities are reason to be bullish. It is also reasonable to expect that the Irish government will be relatively friendly to business looking forward.”

From Marginal Revolution:

“As a metric of how well economes are doing, gdp is underrated, as I argue in my latest Bloomberg column. Here is one bit:

If a nation has a lot of foreign direct investment, as does Ireland, GDP will exceed GNP by a considerable amount. According to the Irish government, the country’s GDP is about 370 billion euros. Its GNP is less than 300 billion euros.

Posted by at 2:25 PM

Labels: Macro Demystified

Sunday, April 10, 2022

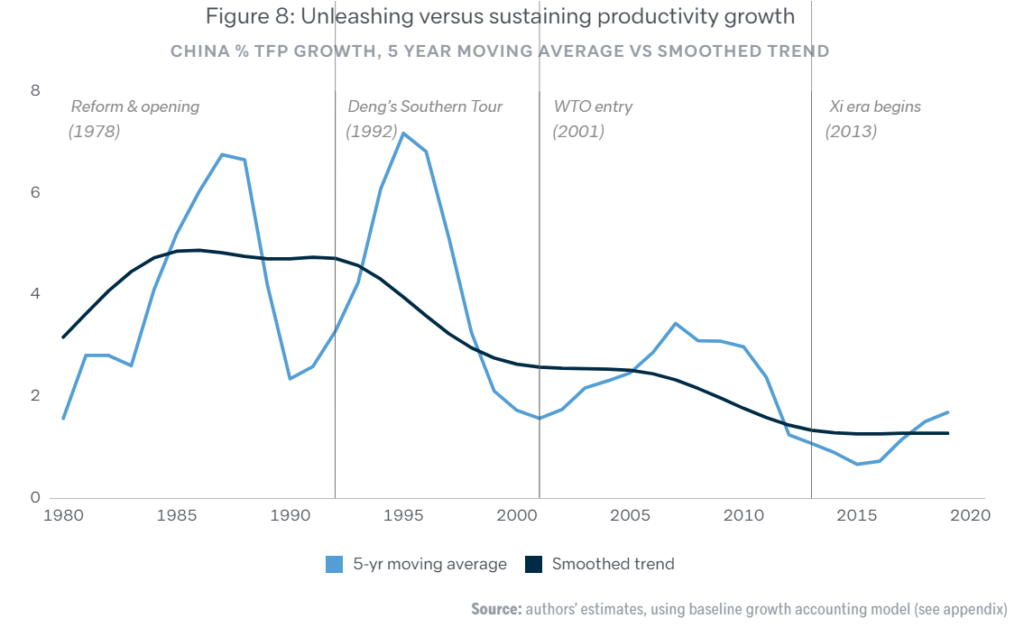

Five reasons China’s productivity slowed down

From Noahpinion:

“It’s always an interesting experience to read books about China’s economy from before 2018 or so. So many world-shaking events have changed the story since then — Trump’s trade war, Covid, Xi’s industrial crackdowns, the real estate bust, lockdowns, Russia’s invasion of Ukraine. Reading predictions of China’s evolution from before these events occurred is a little like reading sci-fi from 1962.

When I started China’s Economy: What Everyone Needs to Know®, by the veteran economic consultant Arthur Kroeber, I was prepared for this surreal effect. After all, it was published in April 2016 — not the most opportune timing. So I was pleasantly surprised by how relevant the book still felt. Most of the book’s explanations of aspects of the Chinese economy — fiscal federalism, urbanization and real estate construction, corruption, Chinese firms’ position within the supply chain, etc. — are either still highly relevant, or provide important explanations of what Xi’s policies were reacting against. Dan Wang was not wrong to recommend that I read it.

But China’s Economy is still a book from 2016, and through it all runs a strain of stubborn optimism that seems a lot less justifiable six years later. Most crucially, while Kroeber acknowledged many of China’s economic challenges — an unsustainable pace of real estate construction, low efficiency of capital, an imbalance between investment and consumption, and so on — he argued that China would eventually overcome these challenges by shifting from an extensive growth model based on resource mobilization to one based on greater efficiency and productivity improvements. This was despite his acknowledgement of the fact that productivity growth had already slowed well before 2016, and that Xi’s policies so far didn’t seem up to the challenge of reviving it.

In many ways, productivity growth is the thread that ties together the entire story of the Chinese economy since 2008. Basic economic theory says that eventually the growth benefits of capital accumulation hit a wall, and you have to improve technology and/or efficiency to keep growth going. Some countries, like Japan, South Korea, Singapore, and Taiwan, have done this successfully, and are now rich; other, like Thailand, failed to do it and are now languishing at the middle income level. For several decades, Chinese productivity growth looked like Japan’s or Korea’s did. But slightly before Xi came to power, it downshifted to look a bit more like Thailand. Here’s a graph from the Lowy Institute’s recent report:”

From Noahpinion:

“It’s always an interesting experience to read books about China’s economy from before 2018 or so. So many world-shaking events have changed the story since then — Trump’s trade war, Covid, Xi’s industrial crackdowns, the real estate bust, lockdowns, Russia’s invasion of Ukraine. Reading predictions of China’s evolution from before these events occurred is a little like reading sci-fi from 1962.

When I started China’s Economy: What Everyone Needs to Know®,

Posted by at 7:58 AM

Labels: Macro Demystified

Friday, April 8, 2022

Regional Differences in Okun’s Law and Explanatory Factors: Some Insights From Europe

From a new paper by Adolfo Maza:

“Okun’s law is one of the best-known stylized facts in the economic literature, as well as one of the most widely used policy tools. The aim of this paper, which utilizes a comprehensive sample of 265 European regions by using annual observations covering the period from 2000 to 2019, is to deepen our knowledge of Okun’s law from two perspectives: on one hand, by checking the existence and intensity of regional differences, and on the other hand, by assessing the factors that explain them. To this end, in the first part, we apply a heterogeneous panel approach that deals with cross-sectional dependence, which allows us to obtain an average coefficient as well as region-specific coefficients. In the second part, a cross-sectional spatial model is used to uncover explanatory factors. Our findings reveal quite remarkable regional differences, as well as a somewhat geographical pattern in them. Moreover, they point out the importance of demographic factors (such as gender and age), labor market variables (share of employment in industry and construction, as well as self-employment and part-time employment and the severity of long-term unemployment), R&D expenditure, and some national institutional factors when it comes to explaining differences across regions.”

From a new paper by Adolfo Maza:

“Okun’s law is one of the best-known stylized facts in the economic literature, as well as one of the most widely used policy tools. The aim of this paper, which utilizes a comprehensive sample of 265 European regions by using annual observations covering the period from 2000 to 2019, is to deepen our knowledge of Okun’s law from two perspectives: on one hand, by checking the existence and intensity of regional differences,

Posted by at 11:29 AM

Labels: Macro Demystified

Subscribe to: Posts