Showing posts with label Macro Demystified. Show all posts

Thursday, October 19, 2017

Aggregate Uncertainty Shocks and Sectoral Productivity

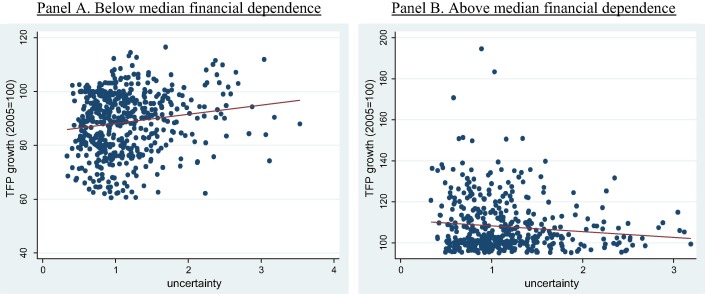

My paper with Sangyup Choi, Davide Furceri, and Yi Huang on the effects of effect of aggregate uncertainty shocks on sectoral productivity is now forthcoming in the Journal of International Money and Finance and is available (link) at the JIMF website. First, we find that an increase in aggregate uncertainty reduces productivity growth more in industries that depend heavily on external finance. Second, the mechanism at play is that during periods of high uncertainty, firms that are credit constrained switch the composition of investment by reducing productivity-enhancing investment that is more subject to liquidity risks. Third, the mechanism is stronger during recessions, when credit constraints bind more. For those without access to JIMF, an earlier working paper (link) version is available.

My paper with Sangyup Choi, Davide Furceri, and Yi Huang on the effects of effect of aggregate uncertainty shocks on sectoral productivity is now forthcoming in the Journal of International Money and Finance and is available (link) at the JIMF website. First, we find that an increase in aggregate uncertainty reduces productivity growth more in industries that depend heavily on external finance. Second, the mechanism at play is that during periods of high uncertainty,

Posted by at 9:47 AM

Labels: Macro Demystified

Wednesday, June 28, 2017

Cross-Country Spillovers of Fiscal Consolidations in the Euro Area

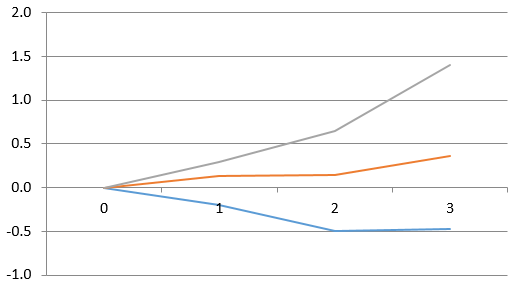

An IMF working paper finds: “This paper assesses spillovers from fiscal consolidations in 10 euro area countries using an innovative empirical methodology. The analysis lends support to the existence of fiscal spillovers, with fiscal consolidation in one country reducing not only the domestic output but also the output of other member states. Spillover effects are larger for: (i) more closely located and economically integrated countries, and (ii) for fiscal shocks originating from relatively larger countries. Most of the impact comes from revenue measures, while the impact of expenditure measures is relatively weaker. The latter result is consistent with the distortionary effects of taxation and empirical literature on fiscal multipliers using the narrative approach (Leigh and others 2010; Abiad and others 2011).

Our results have important policy implications. They suggest that fiscal consolidations in individual euro area countries, especially the larger ones, can reduce aggregate demand in others. The magnitude of cross-country spillovers has strengthened with the economic integration and introduction of a single currency. Also, spillovers can be larger if fiscal consolidations are implemented in downturns. Therefore, individual euro area countries should consider fiscal measures implemented in other members as well as the state of the economy when implementing domestic policies.”

For previous IMF work on negative demand spillovers in the euro area, see my VoxEU blog and Larry Elliott’s column.

Figure 1. Impact on Eurozone output from wage moderation, quantitative easing and structural

An IMF working paper finds: “This paper assesses spillovers from fiscal consolidations in 10 euro area countries using an innovative empirical methodology. The analysis lends support to the existence of fiscal spillovers, with fiscal consolidation in one country reducing not only the domestic output but also the output of other member states. Spillover effects are larger for: (i) more closely located and economically integrated countries, and (ii) for fiscal shocks originating from relatively larger countries.

Posted by at 4:19 PM

Labels: Inclusive Growth, Macro Demystified

Thursday, June 15, 2017

Dani Rodrik on the populist backlash against globalization

From a new paper by Dani Rodrik:

“The resulting system — variably called the Bretton Woods compromise or embedded liberalism was a great success. It fostered a large increase in global trade and investment and saw rapid economic development in both the advanced and developing economies. Perhaps it was too successful for its own good. By the late 1980s, policy makers and economists thought they could make it work even better by pushing for deeper economic integration. Trade agreements became more ambitious and reached beyond the border into domestic regulations. The removal of restrictions on capital mobility became the norm rather than the exception. In the process, the “embedding” or “compromise” that had made the earlier regime such a success was overlooked.

The rise of populism forces a necessary reality check. Today the big challenge facing policy makers is to rebalance globalization so to maintain a reasonably open world economy while curbing its excesses.”

Continue reading here.

From a new paper by Dani Rodrik:

“The resulting system — variably called the Bretton Woods compromise or embedded liberalism was a great success. It fostered a large increase in global trade and investment and saw rapid economic development in both the advanced and developing economies. Perhaps it was too successful for its own good. By the late 1980s, policy makers and economists thought they could make it work even better by pushing for deeper economic integration.

Posted by at 9:05 AM

Labels: Macro Demystified

Monday, June 5, 2017

Understanding Today’s Stagnation

From a new post by Robert Shiller:

“My own theory about today’s stagnation focuses on growing angst about rapid advances in technologies that could eventually replace many or most of our jobs, possibly fueling massive economic inequality. People might be increasingly reluctant to spend today because they have vague fears about their long-term employability – fears that may not be uppermost in their minds when they answer consumer-confidence surveys. If that is the case, they might increasingly need stimulus in the form of low interest rates to keep them spending. ”

Continue reading here.

From a new post by Robert Shiller:

“My own theory about today’s stagnation focuses on growing angst about rapid advances in technologies that could eventually replace many or most of our jobs, possibly fueling massive economic inequality. People might be increasingly reluctant to spend today because they have vague fears about their long-term employability – fears that may not be uppermost in their minds when they answer consumer-confidence surveys. If that is the case,

Posted by at 9:49 AM

Labels: Inclusive Growth, Macro Demystified

Wednesday, May 24, 2017

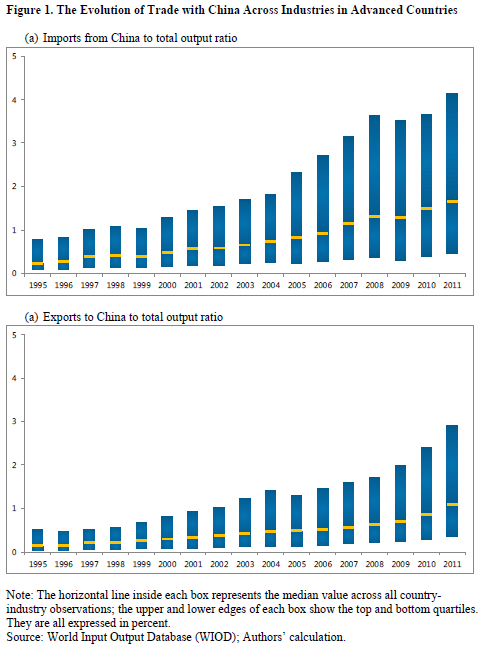

Trading with China : Productivity Gains, Job Losses

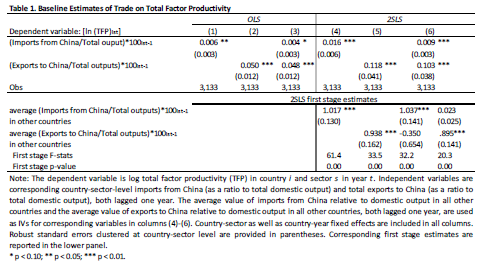

From a new IMF working paper by JaeBin Ahn and Romain Duval:

“We analyze the impact on productivity in advanced economies of fast-growing trade with China between the mid-1990s and late-2000s, separately identifying the export and import channels. We use country-sector-level data for 18 advanced economies and, similar to Autor, Dorn, and Hanson (2013), exploit exogenous variation in trade with China in a given country-sector by instrumenting imports from (exports to) China in a given country-sector with the average imports from (exports to) China in the same sector in other advanced economies. Our estimates point to large productivity gains from trading with China—the (exogenous) rise of China in global trade may have increased the level of total factor productivity by about 1.9 percent, or 12.3 percent of the overall increase over the sample period, in the median country-sector. By contrast, using a similar empirical strategy, we find adverse employment effects of Chinese imports in exposed country-industries, consistent with previous studies. Taken together, these findings point to large gains from free trade, while underscoring the scope for a more active policy role in redistributing them, particularly by easing workers’ transition between jobs and industries.”

Continue reading here.

From a new IMF working paper by JaeBin Ahn and Romain Duval:

“We analyze the impact on productivity in advanced economies of fast-growing trade with China between the mid-1990s and late-2000s, separately identifying the export and import channels. We use country-sector-level data for 18 advanced economies and, similar to Autor, Dorn, and Hanson (2013), exploit exogenous variation in trade with China in a given country-sector by instrumenting imports from (exports to) China in a given country-sector with the average imports from (exports to) China in the same sector in other advanced economies.

Posted by at 4:24 PM

Labels: Inclusive Growth, Macro Demystified

Subscribe to: Posts