Showing posts with label Macro Demystified. Show all posts

Monday, June 25, 2018

Six unconventional introductions to economics

From Tim Harford:

“My list of five of the best introductions to economics wasn’t exactly the usual suspects, but I wanted to stray a little further off the obvious territory and recommend six books you might want to read to give you an unusual introduction to economics.

A couple of years after the financial crisis I came across Charles Perrow’s Normal Accidents (UK) (US). Perrow is a sociologist who became fascinated by particular kinds of system, ones which were “complex” (meaning that consequences of error are unpredictable) and “tightly coupled” (meaning that the consequences unfold quickly and irreversibly). His case studies include terrible accidents such as the Challenger disaster and Chernobyl – hauntingly described – but I increasingly came to realise that economic and financial systems could and should be studied with the same eye. (For the same reason, I’d also recommend anything by James Reason. (UK) (US).)

Yoram Bauman and Grady Klein’s Cartoon Introduction To Economics (UK) (US) is perfectly conventional in many ways – except that it’s a cartoon, and also pretty funny, as you might expect from Bauman, a stand-up comedian. Good stuff.”

Continue reading here.

From Tim Harford:

“My list of five of the best introductions to economics wasn’t exactly the usual suspects, but I wanted to stray a little further off the obvious territory and recommend six books you might want to read to give you an unusual introduction to economics.

A couple of years after the financial crisis I came across Charles Perrow’s Normal Accidents (UK) (US).

Posted by at 1:29 PM

Labels: Macro Demystified

Wednesday, June 6, 2018

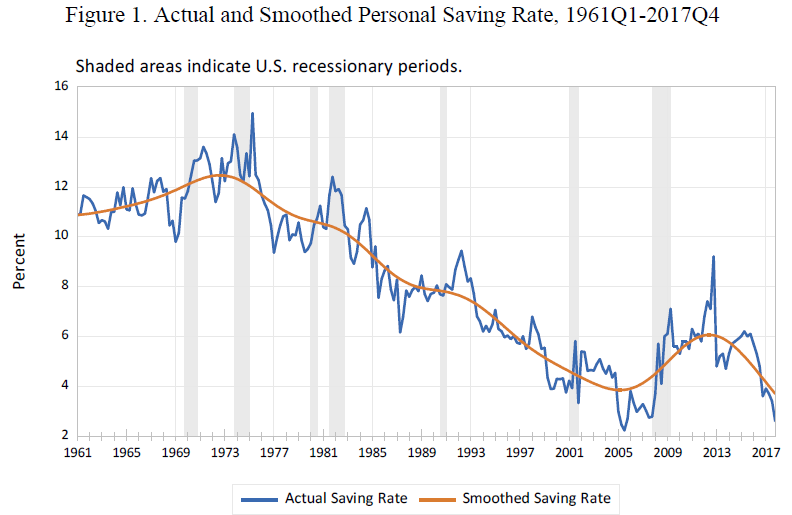

The U.S. Personal Saving Rate

A new IMF paper shows that “Before the crisis, the personal saving rate was trending downwards. However, in 2008 there was a significant rise in the saving rate that continued until the end of 2012, suggesting a permanent change in household behavior. […] the rise in the saving rate during 2008-2012 was caused by the negative shocks to income, employment and wealth. This result explains why the saving rate resumed its decline in 2013, as real disposable income, employment

and net worth recovered. Assuming that the real growth in these determinants remains strong, the estimated model predicts continued negative pressures on the current account deficit and further external imbalances attributable to the U.S. household sector.”

A new IMF paper shows that “Before the crisis, the personal saving rate was trending downwards. However, in 2008 there was a significant rise in the saving rate that continued until the end of 2012, suggesting a permanent change in household behavior. […] the rise in the saving rate during 2008-2012 was caused by the negative shocks to income, employment and wealth. This result explains why the saving rate resumed its decline in 2013, as real disposable income,

Posted by at 1:35 PM

Labels: Inclusive Growth, Macro Demystified

Thursday, May 31, 2018

Finance, the state and innovation

From the Enlightened Economist:

“Yesterday brought the launch of a new and revised edition of Doing Capitalism in the Innovation Economy by William Janeway. Anybody who read the first (2012) edition will recall the theme of the ‘three player game’ – market innovators, speculators and the state – informed by Keynes and Minsky as well as Janeway’s own experience combining an economics PhD with his experience shaping the world of venture capital investment.

The term refers to how the complicated interactions between government, providers of finance and capitalists drive technological innovation and economic growth. The overlapping institutions create an inherently fragile system, the book argues – and also a contingent one. Things can easily turn out differently.

The book starts with a more descriptive first half, including Janeway’s “Cash and Control” approach to investing in new technologies, and also an account of how the three players in the US shaped the computer revolution. This is an admirably clear but nuanced history emphasising the important role of the state – through defense spending in particular – but also the equally vital private sector involvement. I find this sense of the complicated and path dependent interplay far more persuasive than simplistic accounts emphasising either the government or the market.”

Continue reading here.

From the Enlightened Economist:

“Yesterday brought the launch of a new and revised edition of Doing Capitalism in the Innovation Economy by William Janeway. Anybody who read the first (2012) edition will recall the theme of the ‘three player game’ – market innovators, speculators and the state – informed by Keynes and Minsky as well as Janeway’s own experience combining an economics PhD with his experience shaping the world of venture capital investment.

Posted by at 11:33 AM

Labels: Macro Demystified

Wednesday, May 30, 2018

Exchange rate forecasting on a napkin

From a new ECB working paper:

“The international finance literature has documented two important regularities in foreign exchange markets. First, there is ample evidence that, for developed countries, real exchange rates are reverting to the level implied by the Purchasing Power Parity (PPP) theory. Second, for flexible currency regimes the adjustment process is mainly driven by the nominal exchange rate. At the same time most of the recent articles remain skeptical that one can outperform the random walk (RW) in nominal exchange rate forecasting.

In this paper we claim that the two above in-sample regularities of foreign exchange markets can be exploited to infer out-of-sample movements of major currency pairs. To prove this thesis we proceed as follows:

- We begin by presenting robust (in-sample) evidence that, for major currency pairs, long-run PPP holds and that the nominal exchange rate is the main driver of this adjustment process.

- We then evaluate a battery of models that aim to exploit these in-sample regularities for forecasting purposes. The winner of the forecasting race is a calibrated PPP model, which just assumes that the real exchange rate gradually returns to its sample mean, completing half of the adjustment in 3 years, and that the adjustment is only driven by the nominal exchange rate. This approach is so simple that it can be implemented even on the back of a napkin in two steps. Step 1 consists in calculating the initial real exchange rate misalignment with an eyeball estimate of what is the distance from the sample mean. Step 2 consists in recalling that, according to this model, one tenth of the required adjustment is achieved by the nominal exchange rate in the first 6 months, one fifth in one year, just over a third in two years and exactly half after 3 years.

- We highlight that severe problems arise when attempting to carry out more sophisticated approaches, such as estimating the pace of mean reversion of the real exchange rate or forecasting relative inflation. Among the estimated approaches, we find that it is strongly preferable to rely on direct rather than multi-step iterative forecasting methods. We also find that models estimated with panel data techniques perform only marginally better than those based on individual currency pairs. This finding has bittersweet implications. On the negative side, estimated models encounter a second formidable competitor that, like the RW, bypasses the estimation error problem. On the positive side, the HL model is more acceptable than the RW from the perspective of economic theory.

- This analysis highlights also that equilibrium exchange rate analysis matters. Simple measures of exchange rate disequilibria, not only signal economic imbalances, but also provide hints in which direction the exchange rate will go.

Our paper has an important message for policymakers. For advanced countries, it is better to rely on the concept of long-run PPP rather than on the RW.”

From a new ECB working paper:

“The international finance literature has documented two important regularities in foreign exchange markets. First, there is ample evidence that, for developed countries, real exchange rates are reverting to the level implied by the Purchasing Power Parity (PPP) theory. Second, for flexible currency regimes the adjustment process is mainly driven by the nominal exchange rate. At the same time most of the recent articles remain skeptical that one can outperform the random walk (RW) in nominal exchange rate forecasting.

Posted by at 9:32 AM

Labels: Forecasting Forum, Macro Demystified

Tuesday, May 29, 2018

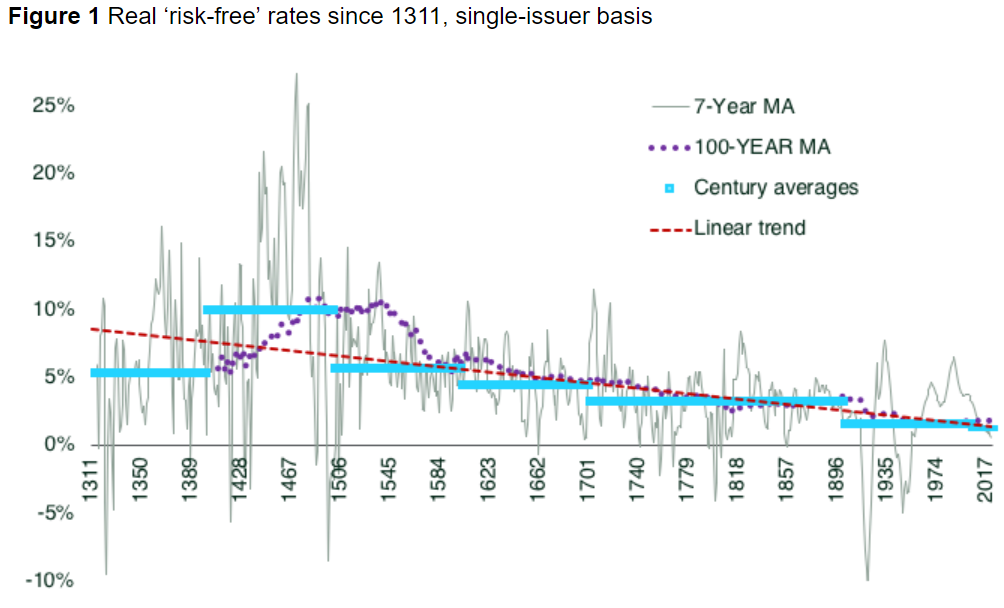

The ‘suprasecular’ stagnation

A new VOXEU post by Paul Schmelzing says that “Trends over recent decades are generally in line with a long-term ‘suprasecular’ trend of declining real rates.”

“[…] even if cyclical forces could now stabilise nominal Treasury rates beyond 3%, central bankers may find that before they have fully returned to normalised balance sheets, ‘suprasecular’ real rate trends will have caught up to them once more. Negative real rates could become a more frequent phenomenon, and indeed constitute a ‘new normal’. Absent geopolitical or natural disaster shocks – which in the past at least temporarily ‘broke’ the trend – unconventional monetary tools may (under this scenario) mature into more permanent features of the international financial system.”

A new VOXEU post by Paul Schmelzing says that “Trends over recent decades are generally in line with a long-term ‘suprasecular’ trend of declining real rates.”

“[…] even if cyclical forces could now stabilise nominal Treasury rates beyond 3%, central bankers may find that before they have fully returned to normalised balance sheets, ‘suprasecular’ real rate trends will have caught up to them once more. Negative real rates could become a more frequent phenomenon,

Posted by at 8:03 AM

Labels: Inclusive Growth, Macro Demystified

Subscribe to: Posts