Showing posts with label Macro Demystified. Show all posts

Friday, September 7, 2018

Understanding the Decline of U.S. Manufacturing Employment

From a new working paper by Susan N. Houseman:

“Two stylized facts underlie the prevailing view that automation largely caused the relative decline and, in the 2000s, the large absolute decline in U.S. manufacturing employment: first, manufacturing real output growth has largely kept pace with that of the aggregate economy for decades, and second, manufacturing labor productivity growth has been considerably higher. These statistics appear to provide a compelling case that domestic manufacturing is strong, and that, as in agriculture, productivity growth, assumed to reflect automation, is largely responsible for the relative and absolute decline in manufacturing employment. Although the size and scope of the decline in employment manufacturing industries in the 2000s was unprecedented, many

see it as part of a long-term trend and deem the role of trade small.”

“That view, I have argued, reflects a misinterpretation of the numbers. First, aggregate manufacturing output and productivity statistics are dominated by the computer industry and mask considerable weakness in most manufacturing industries, where real output growth has been much slower than average private sector growth since the 1980s and has been anemic or declining since 2000. Second, labor productivity growth is not synonymous with, and is often a poor indicator of, automation. Measures of labor productivity growth may capture many forces besides automation—including improvements in product quality, outsourcing and offshoring, and a changing industry composition owing to international competition. Indeed, the rapid productivity growth in the computer and electronics products industry, and by extension in the manufacturing sector, largely reflects improvements in product quality, not automation. In short, the stylized facts, when properly interpreted, do not provide prima facie evidence that automation drove the relative and absolute decline in manufacturing employment.”

“It is difficult to parse out the effects of various factors on manufacturing employment, and research does not provide simple decompositions of the total contribution that trade and the broader forces of globalization make to manufacturing’s recent employment decline. Nevertheless, the research evidence points to trade and globalization as the major factor behind the large and swift decline of manufacturing employment in the 2000s. Although manufacturing processes continue to be automated, there is no evidence that the pace of automation in the sector accelerated in the 2000s; if anything, research comes to the opposite conclusion.”

“Manufacturing still matters, and its decline has serious economic consequences. Reflecting the sector’s deep supply chains, manufacturing’s plight contributed to the weak employment growth and poor labor market outcomes prevailing during much of the 2000s. Research shows that such large-scale shocks have persistent adverse effects on affected communities and their residents, though these costs rarely are fully considered in policy making (Klein, Schuh, and Triest 2003). In addition, because manufacturing accounts for a disproportionate share of R&D, the health of manufacturing industries has important implications for innovation in the economy. The widespread denial of domestic manufacturing’s weakness and globalization’s role in its employment collapse has inhibited much-needed, informed debate over trade policies.”

From a new working paper by Susan N. Houseman:

“Two stylized facts underlie the prevailing view that automation largely caused the relative decline and, in the 2000s, the large absolute decline in U.S. manufacturing employment: first, manufacturing real output growth has largely kept pace with that of the aggregate economy for decades, and second, manufacturing labor productivity growth has been considerably higher. These statistics appear to provide a compelling case that domestic manufacturing is strong,

Posted by at 10:56 AM

Labels: Inclusive Growth, Macro Demystified

Saturday, August 4, 2018

Twin Deficits in Developing Economies

A new IMF working paper by Davide Furceri and Aleksandra Zdzienicka provides “new evidence on the existence and magnitude of the “twin deficits” in developing economies. It finds that a one percent of GDP unanticipated increase in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than that obtained using standard measures of fiscal impulse, such as the cyclically-adjusted budget balance. The results point to heterogeneity across countries and over time. The effect tends to be larger: (i) during recessions; in countries (ii) that are more open to trade; (iii) that have less flexible exchange rate regimes; and (iv) with lower initial public debt-to-GDP ratios.”

A new IMF working paper by Davide Furceri and Aleksandra Zdzienicka provides “new evidence on the existence and magnitude of the “twin deficits” in developing economies. It finds that a one percent of GDP unanticipated increase in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than that obtained using standard measures of fiscal impulse, such as the cyclically-adjusted budget balance.

Posted by at 5:47 PM

Labels: Macro Demystified

Monday, July 30, 2018

Twin Deficits in Developing Economies

From a new IMF working paper by Davide Furceri and Aleksandra Zdzienicka:

“We provide new evidence of the existence of the “twin deficits” in developing economies. Using unanticipated government spending shocks for an unbalanced panel of 114 developing economies from 1990 to 2015, we find that a one percent of GDP unanticipated improvement in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than usually found in the literature using standard measures of fiscal policy changes such as the CAB. This finding has important policy implications as for a given target of external adjustment less fiscal consolidation is required than normally assumed.

Beyond this average effect lies some heterogeneity, both across states of the business cycle and across countries. The effect tends to be larger: (i) during recessions; (ii) in countries that are more open to trade; (iii) that have less flexible exchange rate regimes; and (iv) with lower initial public debt-to-GDP ratios. This heterogeneity has far-reaching implications for policymakers in deciding the magnitude of the fiscal adjustment needed to address external imbalances.”

From a new IMF working paper by Davide Furceri and Aleksandra Zdzienicka:

“We provide new evidence of the existence of the “twin deficits” in developing economies. Using unanticipated government spending shocks for an unbalanced panel of 114 developing economies from 1990 to 2015, we find that a one percent of GDP unanticipated improvement in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP.

Posted by at 10:16 AM

Labels: Macro Demystified

Sunday, July 15, 2018

Football’s minnows demonstrate how poor countries can catch up

From a new post by Tim Harford:

“Prof Rodrik has found evidence that unconditional convergence does happen, not for economies as a whole but for specific manufacturing sectors in those economies, such as “macaroni and noodles” or “knitted or crocheted apparel” or “plastic sacks and bags”.

If such a sector is well behind the global cutting edge, it can expect labour productivity to grow by 4-8 per cent a year, enough to double every decade or two. This tendency holds regardless of what else might be happening in the economy. Why?

The likely answer is that such manufacturing sectors get drawn into global supply chains. They can learn quickly, and must do so to respond to the incessant threat of competition. They will be doing business with suppliers and customers who can provide swift feedback and instruction. In the modern global economy, certain kinds of know-how travel fast, small tasks are unbundled, and part-finished goods and components shuttle back and forth across borders. Any enterprise plugged into this process will improve quickly. It may be more closely integrated into global supply chains than its own local economy, which might not keep up.

All of which brings us back to football. Two economists, Melanie Krause and Stefan Szymanski, decided to examine whether the unconditional convergence hypothesis holds for international men’s football, as it does for manufacturing sectors. (Prof Szymanski is the co-author, with the Financial Times’s Simon Kuper, of Soccernomics. (UK) (US)) Football, after all, offers a long data set and some clear measures of performance. International football’s governing body, Fifa, has more members than the UN.

Sure enough, Profs Krause and Szymanski found that the strength of international football teams is converging. The minnows are acquiring bite, and the old cliché, “there are no easy games in international football”, is far truer today than it was in 1950.

Perhaps we should not be surprised. As with manufacturing, the standard of competition is fierce, performance metrics unforgiving, and the very best ideas will be copied. As an additional spur to progress, elite football offers a global labour market: a strong player from a weak national team will spend most of his time at a top club side in the company of world-class dietitians, trainers, and teammates. His home nation will enjoy the benefits.

It is tempting to draw grand conclusions from all this, about the increasing importance of knowledge in globalisation; about the bracing effects of robust international competition; about the benefits of being open to international migrants. But perhaps it is better to just watch the football. In an age of distressing reality-TV politics, here, at least, is a competitive spectacle we can all enjoy.”

Continue reading here.

From a new post by Tim Harford:

“Prof Rodrik has found evidence that unconditional convergence does happen, not for economies as a whole but for specific manufacturing sectors in those economies, such as “macaroni and noodles” or “knitted or crocheted apparel” or “plastic sacks and bags”.

If such a sector is well behind the global cutting edge, it can expect labour productivity to grow by 4-8 per cent a year,

Posted by at 11:00 AM

Labels: Inclusive Growth, Macro Demystified

Thursday, July 5, 2018

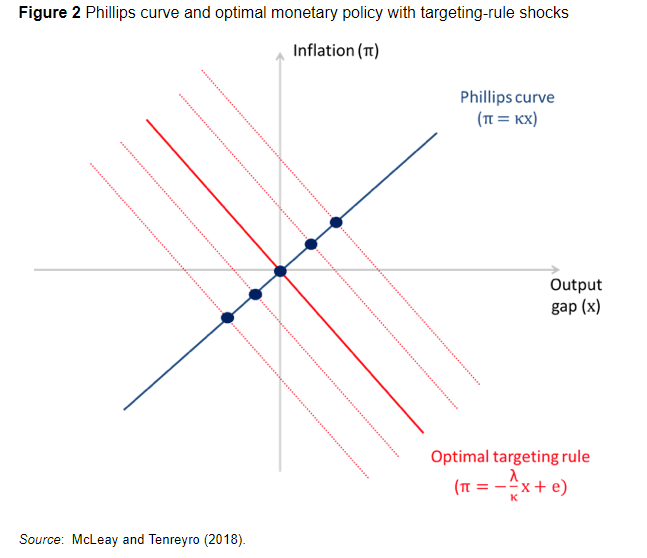

Optimal inflation and the identification of the Phillips curve

From a new VOX post by Michael McLeay and Silvana Tenreyro:

“We have long known that the empirical Phillips curve may vary with monetary policy (Lucas 1976). One common explanation for the Great Inflation of the 1970s is that policymakers mistakenly tried to exploit the prevailing reduced-form Phillips curve, and in so doing caused it to disappear (e.g. Sargent et al. 2006). In contrast, our point is that a disappearing Phillips curve is also a natural consequence of good monetary policy. If the true model of the economy involves a Phillips curve relationship, monetary policymakers aware of its existence should ensure it remains elusive in the data.”

From a new VOX post by Michael McLeay and Silvana Tenreyro:

“We have long known that the empirical Phillips curve may vary with monetary policy (Lucas 1976). One common explanation for the Great Inflation of the 1970s is that policymakers mistakenly tried to exploit the prevailing reduced-form Phillips curve, and in so doing caused it to disappear (e.g. Sargent et al. 2006). In contrast, our point is that a disappearing Phillips curve is also a natural consequence of good monetary policy.

Posted by at 1:13 PM

Labels: Macro Demystified

Subscribe to: Posts