Showing posts with label Macro Demystified. Show all posts

Friday, October 19, 2018

When the Market Drives you Crazy: Stock Market Returns and Fatal Car Accidents

From a new CESifo working paper:

“The stock market influences some of the most fundamental economic decisions of investors, such as consumption, saving, and labor supply, through the financial wealth channel. This paper provides evidence that daily fluctuations in the stock market have important – and hitherto neglected – spillover effects in another, unrelated domain, namely driving. Using the universe of fatal road car accidents in the United States from 1990 to 2015, we find that a one standard deviation reduction in daily stock market returns is associated with a 0.5% increase in the number of fatal accidents. A battery of falsification tests support a causal interpretation of this finding. Our results are consistent with immediate emotions stirred by a negative stock market performance influencing the number of fatal accidents, in particular among inexperienced investors, thus highlighting the broader economic and social consequences of stock market fluctuations.”

From a new CESifo working paper:

“The stock market influences some of the most fundamental economic decisions of investors, such as consumption, saving, and labor supply, through the financial wealth channel. This paper provides evidence that daily fluctuations in the stock market have important – and hitherto neglected – spillover effects in another, unrelated domain, namely driving. Using the universe of fatal road car accidents in the United States from 1990 to 2015,

Posted by at 10:41 AM

Labels: Macro Demystified

More evidence that it’s really hard to ‘beat the market’

According to Mark Perry of Carpe Diem: “over the last 15 years from June 30, 2003 to June 30, 2018, only one in 13 large-cap managers, only one in 21 mid-cap managers, and one in 43 small-cap managers were able to outperform their benchmark index. So it is possible for some active fund managers to “beat the market” over various time horizons, although there’s no guarantee that they will continue to do so in the future. And the percentage of active managers who do beat the market is usually pretty small – fewer than 8% in most of the cases above over the last 15 years; and they may not sustain that performance in the future.”

Read the full story here, which gives a link to the underlying study.

According to Mark Perry of Carpe Diem: “over the last 15 years from June 30, 2003 to June 30, 2018, only one in 13 large-cap managers, only one in 21 mid-cap managers, and one in 43 small-cap managers were able to outperform their benchmark index. So it is possible for some active fund managers to “beat the market” over various time horizons, although there’s no guarantee that they will continue to do so in the future.

Posted by at 10:36 AM

Labels: Macro Demystified

Wednesday, October 10, 2018

Why Has the Stock Market Risen So Much Since the US Presidential Election?

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends. A general improvement in economic activity and a decrease in economic policy uncertainty around the world were the main factors behind the stock market increase. The prospect and the eventual passage of the corporate tax bill nevertheless played a role. And while part of the rise in stock returns came from a decrease in the equity risk premium, this decrease was relatively limited and returned the premium to the levels of the first half of the 2000s.”

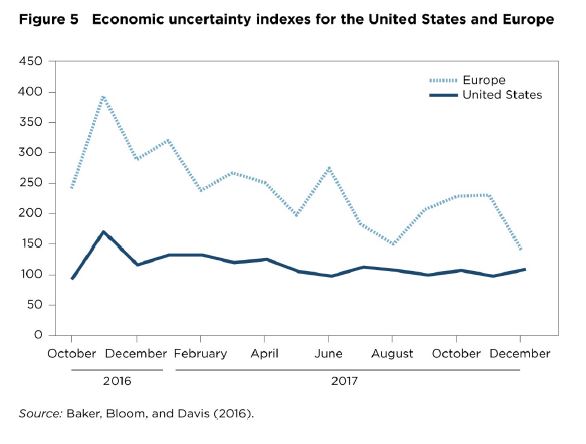

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends.

Posted by at 4:11 PM

Labels: Macro Demystified

Thursday, October 4, 2018

Why economy watchers obsess over the U.S. monthly jobs report

From an new LSE Business Review article by Ken Fireman:

“It is an ingrained monthly ritual for U.S. economy mavens: staring intently at a computer screen or smartphone on the first Friday of the month as the clock ticks down to 8:30 a.m. Eastern time, the moment when the Labor Department releases its jobs report for the previous month.

The two numbers that draw the headlines are those that report how many jobs the U.S. economy created (or lost) and what percentage of the workforce is unemployed. The results can shape perceptions of the world’s largest economy, influence policymakers’ choices and drive investment decisions, SAGE Business Researcher freelance correspondent Victoria Finkle writes. The report is considered so market-sensitive that journalists covering it are literally locked in a room and cut off from communicating with the outside world until the instant of the release time.

“What’s codified into a couple of small numbers is a lot of knowledge about where the economy is and where the economy is going,” Michael Farren, a research fellow at George Mason University’s Mercatus Center, told Business Researcher.

But those top-line numbers are just the tip of a mountain of valuable statistical material contained in the 40-page report, Finkle writes in her account of the monthly exercise. And the data that lurk in the recesses of the report can lend texture and detail to our understanding of the economy and provide deep insights into how policymakers at the Federal Reserve and other institutions will move in the future.

Take, for example, the unemployment rate. The headline number, known as the U-3 rate from its Labor Department code, measures the percentage of the total labour force that is jobless and actively seeking work. It’s closely watched because it is tied to both halves of the Fed’s so-called dual mandate of maximising employment while maintaining price stability, Finkle writes.

But U-3 is just one way to view unemployment. It captures only those who are jobless but still looking for work; people who are so discouraged by their job prospects that they’ve simply given up searching are not counted among the unemployed in this measure. So the quants in the department’s Bureau of Labor Statistics calculate two more rates. One, known as U-5, captures those jobless and looking, plus “marginally attached” workers – those who have looked for work sometime in the past year, but not recently. U-5 is a favourite of Treasury Secretary Steven Mnuchin, who has said U-3 doesn’t provide a complete picture of the labour market. “Currently, excessive influence appears to be placed by U.S. policymakers on one metric,” he said last year, referring to the headline unemployment rate.

A second alternative measure, known as U-6, encompasses everyone unemployed and looking, plus the marginally attached – and those who are working, but in a part-time job when they would rather work full-time. This metric, sometimes known as the underemployment rate, also has its fans; it was often cited by former Fed Chair Janet Yellen during her tenure at the helm of the central bank.

Finally, the report contains data on the percentage of those unemployed who have been out of work for 27 weeks or more. Economists watch this measure, known as the long-term jobless rate, because the longer people remain out of work, the harder it becomes for them to become re-employed, Finkle writes.

No matter which unemployment rate one prefers, a constant factor in the equation is the size of the labour force, the sum of all employed and unemployed workers. And economists pay close attention to another measure in the monthly jobs report that bears directly upon the size of the labour force: the rate of participation. It has been declining in recent years – more than 3 percentage points in the past decade – as the large baby boomer generation edges into retirement, a “skills gap” widens between available workers and available jobs and opioid addiction and higher prison rates take their toll.

The monthly report also tracks a number that has been an enduring puzzle: workers’ earnings. As the economy recovered from the 2007-09 recession and the various unemployment rates fell, standard economic theory suggested that wages should rise more or less in tandem, as a stronger economy generated more demand for workers. The fact that this hasn’t happened has left many economists scratching their heads.

Each measure in the jobs report offers one piece of a puzzle that economists, money managers and other decision-makers use to better understand where the economy is headed, Finkle writes.

“If you see that employment grows by 200,000 or wages are growing by 2.5 percent year-over-year, what does that mean?” the Mercatus Center’s Farren told Business Researcher. “When you aggregate [survey data] across all businesses, that’s telling you something about the state of the economy in general. There’s a lot that’s influenced downstream by these relatively limited numbers.”

From an new LSE Business Review article by Ken Fireman:

“It is an ingrained monthly ritual for U.S. economy mavens: staring intently at a computer screen or smartphone on the first Friday of the month as the clock ticks down to 8:30 a.m. Eastern time, the moment when the Labor Department releases its jobs report for the previous month.

The two numbers that draw the headlines are those that report how many jobs the U.S.

Posted by at 9:29 AM

Labels: Macro Demystified

Friday, September 14, 2018

Systemic Banking Crises Revisited

From a new IMF working paper by Luc Laeven and Fabian Valencia:

“This paper updates the database on systemic banking crises presented in Laeven and Valencia (2008, 2013). Drawing on 151 systemic banking crises episodes around the globe during 1970-2017, the database includes information on crisis dates, policy responses to resolve banking crises, and the fiscal and output costs of crises. We provide new evidence that crises in high-income countries tend to last longer and be associated with higher output losses, lower fiscal costs, and more extensive use of bank guarantees and expansionary macro policies than crises in low- and middle-income countries. We complement the banking crises dates with sovereign debt and currency crises dates to find that sovereign debt and currency crises tend to coincide or follow banking crises.”

From a new IMF working paper by Luc Laeven and Fabian Valencia:

“This paper updates the database on systemic banking crises presented in Laeven and Valencia (2008, 2013). Drawing on 151 systemic banking crises episodes around the globe during 1970-2017, the database includes information on crisis dates, policy responses to resolve banking crises, and the fiscal and output costs of crises. We provide new evidence that crises in high-income countries tend to last longer and be associated with higher output losses,

Posted by at 4:26 PM

Labels: Macro Demystified

Subscribe to: Posts