Showing posts with label Macro Demystified. Show all posts

Monday, November 5, 2018

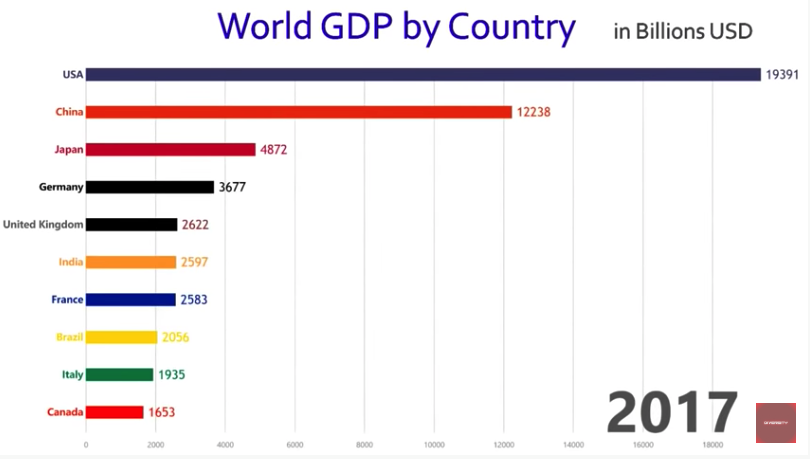

Dynamic chart: World’s ten largest economies, 1961 to 2017

From a new AEI post:

“Watch the top ten largest economies in the world based on GDP, year-by-year from 1961 to 2017. A few interesting observations:

1. The global slowdown in the early 1980s.

2. China’s ranking in the world’s ten largest economies has sure bounced around a lot. It was the world’s fifth largest economy in 1962 and remained in the top ten economies until it dropped out in 1978 and 1979, before returning in 1980, dropping out again for a few years and returning to the top ten in 1982. In 1987, China fell out for a year, came back in 1988, dropped out again in 1989 before returning to the top ten for good in 1992. By 2000, China rose to the No. 6 position by passing Italy, then to No. 5 in 2005 when it surpassed France, to No. 4 in 2006 when it surpassed the UK, No. 3 in 2007 surpassing Germany, and finally rising to No. 2 in 2010 by surpassing Japan.

3. As of 2017, the US economy at $19.4 trillion was 58.4% larger than China’s GDP of $12.2 trillion.”

Watch the dynamic chart here.

From a new AEI post:

“Watch the top ten largest economies in the world based on GDP, year-by-year from 1961 to 2017. A few interesting observations:

1. The global slowdown in the early 1980s.

2. China’s ranking in the world’s ten largest economies has sure bounced around a lot. It was the world’s fifth largest economy in 1962 and remained in the top ten economies until it dropped out in 1978 and 1979,

Posted by at 9:42 PM

Labels: Macro Demystified

Sunday, November 4, 2018

Fall 2018 Journal of Economic Perspectives Available On-line

From a new post by Timothy Taylor:

“I was hired back in 1986 to be the Managing Editor for a new academic economics journal, at the time unnamed, but which soon launched as the Journal of Economic Perspectives. The JEP is published by the American Economic Association, which back in 2011 decided–to my delight–that it would be freely available on-line, from the current issue back to the first issue. Here, I’ll start with Table of Contents for the just-released Fall 2018 issue, which in the Taylor household is known as issue #126. Below that are abstracts and direct links for all of the papers. I may blog more specifically about some of the papers in the next week or two, as well.”

From a new post by Timothy Taylor:

“I was hired back in 1986 to be the Managing Editor for a new academic economics journal, at the time unnamed, but which soon launched as the Journal of Economic Perspectives. The JEP is published by the American Economic Association, which back in 2011 decided–to my delight–that it would be freely available on-line, from the current issue back to the first issue.

Posted by at 9:18 PM

Labels: Macro Demystified

Monday, October 29, 2018

Expansions Don’t Die of Old Age

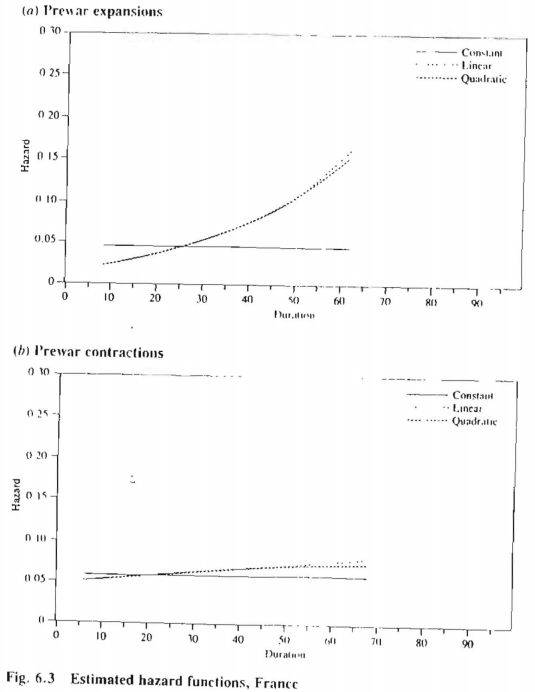

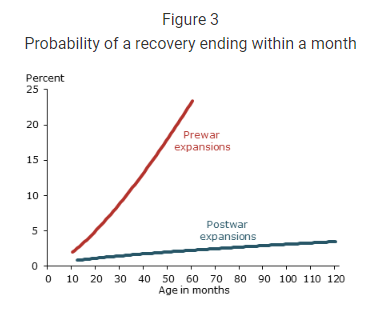

From a new post by Francis Diebold:

“As the expansion ages, there’s progressively more discussion of whether its advanced age makes it more likely to end. The answer is no. More formally, postwar U.S. expansion hazards are basically flat, in contrast to contraction hazards, which are sharply increasing. Of course the present expansion will eventually end, and it may even end soon, but its age it unrelated to its probability of ending.

All of this is very clear in Diebold, Rudebusch and Sichel (1992). See Figure 6.2 on p. 271. (Sorry for the poor photocopy quality.) ”

“The flat expansion hazard result has held up well (e.g., Rudebusch (2016)), and moreover it would only be strengthened by the current long expansion.”

From a new post by Francis Diebold:

“As the expansion ages, there’s progressively more discussion of whether its advanced age makes it more likely to end. The answer is no. More formally, postwar U.S. expansion hazards are basically flat, in contrast to contraction hazards, which are sharply increasing. Of course the present expansion will eventually end, and it may even end soon, but its age it unrelated to its probability of ending.

Posted by at 9:49 AM

Labels: Macro Demystified

Saturday, October 27, 2018

Timothy Taylor on Rent Control Returns

A new post by Timothy Taylor shares some thoughts on rent control returns:

“1) Rent control is typically justified by pointing to low-income people who have difficulty paying the market rents. I’m sympathetic to this groups, and favor various policies like income support and rent vouchers to help them. But as I have argued in other contexts, invoking poverty and necessity as the basis for rent control is a ruse. The poor are not helped in any direct way by controlling rental prices for all income groups, including the rich and the the middle-class.

One response I have heard to this argument is that if rent control only applied to those with low-incomes, there would be an incentive to avoid renting to those with low incomes and not to build any more low-income housing. Of course, this argument is of course an admission that rent control discourages the growth and maintenance of rental properties. Expanding rent control to cover all income groups will expand those negative incentives to the entire rental housing stock, rather than just part of it.

2) Many of those who favor rent control also favor higher minimum wages. Thus, it is useful to remember that rent control is fundamentally different from minimum wage rules, because prices for physical objects like buildings are fundamentally different from wages paid to workers. When the price of an hour of work changes, workers can have higher or lower incentives, or higher or lower morale, or can search more or less for jobs, or consider different kinds of jobs, or look for jobs in other jurisdictions or in the underground economy, or even withdraw from the labor market. Buildings are not flexible in these ways, and so the implications of rent control are easier to predict with confidence than the implications of minimum wage laws.

3) Before you own a house, there can be a tendency (which I certainly had) to think of the housing stock as immutable, rather like the pyramids. When you own a house, you instead come to think of it as a large machine that requires continual maintenance on all its separate parts. Many arguments in favor of rent control implicitly view the housing stock like the pyramids, and underestimate both the short-run costs of maintenance and repair and the longer-run costs of property upgrades and new construction.

4) Rent control offers a tradeoff between present benefits for one group and future costs for another. The present benefits go to those already living in apartments that are rent-controlled–whether they are low-income or not. Rent control benefits the well-settled. The future costs are imposed on those who are unable to find a place. In addition, rent control discourages building additional rental housing, which means that the possibility of mutual gains for future builders and future renters are foreclosed.

5) In any local housing market, the price of owned housing and rental housing is going to be closely linked, because one can be converted with relative ease into the other. If the price of housing is high, the price of rentals is also going to be high. The notion that a local housing market can make all the existing homeowners happy, with high and rising resale prices, but also make all the renters happy, with low and stable rents, is a delusion.

With rent control, as with so many other subjects, it can be tricky to sort out cause and effect. For example, say that we observe that cities which have rent control are more likely to have high housing prices. This of course would not prove whether rent control leads to high housing prices, or high housing prices make rent control more likely to be enacted, or whether some additional factors are influencing both housing prices and the political prospects for rent control. Thus, researchers often try to seek out a “natural experiment,” meaning a situation in which some change in law or circumstance affects part of a market at a certain time and place, but not another part. Then one can compare the more-affected and less-affected parts of the market.”

A new post by Timothy Taylor shares some thoughts on rent control returns:

“1) Rent control is typically justified by pointing to low-income people who have difficulty paying the market rents. I’m sympathetic to this groups, and favor various policies like income support and rent vouchers to help them. But as I have argued in other contexts, invoking poverty and necessity as the basis for rent control is a ruse. The poor are not helped in any direct way by controlling rental prices for all income groups,

Posted by at 11:00 AM

Labels: Macro Demystified

Wednesday, October 24, 2018

Global Alcohol Markets

From a new post by Timothy Taylor:

“Markets for beer, wine and spirits offer can patterns of broad cultural interest–and for the college teacher, may serve to attract the attention of students as well. Kym Anderson, Giulia Meloni, and Johan Swinnen discuss “Global Alcohol Markets: Evolving Consumption Patterns, Regulations, and Industrial Organizations” in the most recent Annual Review of Resource Economics (vol. 10, pp. 105-132, not freely available online, but many readers will have access through a library subscription). The authors take a global perspective on the evolution of alcohol markets. Here are a few points of the many that caught my eye.

1) “The global mix of recorded alcohol consumption has changed dramatically over the past half

century: Wine’s share of the volume of global alcohol consumption has fallen from 34% to 13% since the early 1960s, while beer’s share has risen from 28% to 36%, and spirits’ share has gone from 38% to 51%. In liters of alcohol per capita, global consumption of wine has halved, while that of beer and spirits has increased by 50%.”2) “As of 2010–2014, alcohol composed nearly two-thirds of the world’s recorded expenditure on beverages, with the rest being bottled water (8%), carbonated soft drinks (15%), and other soft

drinks such as fruit juices (13%).”3) There is something of inverse-U relationship between quantity consumed of alcohol and per capita GDP of countries.

4) However, when it comes to spending on alcohol as a share of income, it does not seem to drop off as income rises. The implication is that those in countries with higher per capita GDP drink smaller quantities of alcohol, but pay more for it.

5) “In early history, wine and beer consumption was mostly positively perceived from health and food security perspectives. Both wine and beer were safe to drink in moderation because fermentation kills harmful bacteria. Where available at affordable prices, they were attractive substitutes for water in those settings in which people’s access to potable water had deteriorated. Beer was also a source of calories. For both reasons, beer was used to pay workers for their labor from Egyptian times to the Middle Ages. Wine too was part of some workers’ remuneration and was included in army rations of some countries right up to World War II. Moreover, spirits such as rum and brandy were a standard part of the diet for those in European navies from the fifteenth century.”

The authors then discuss how the rise of hard spirits and income levels raised concerns about health effects of alcohol consumption, while nonalcoholic alternatives became safe to drink–factors that helped to reconfigure social attitudes about alcohol.The article also includes discussions of the evolution of alcohol taxes, shifts in market concentration and competition, the rise of smaller-scale producers in recent years, and much more. “

From a new post by Timothy Taylor:

“Markets for beer, wine and spirits offer can patterns of broad cultural interest–and for the college teacher, may serve to attract the attention of students as well. Kym Anderson, Giulia Meloni, and Johan Swinnen discuss “Global Alcohol Markets: Evolving Consumption Patterns, Regulations, and Industrial Organizations” in the most recent Annual Review of Resource Economics (vol. 10, pp. 105-132, not freely available online,

Posted by at 10:43 AM

Labels: Macro Demystified

Subscribe to: Posts