Showing posts with label Macro Demystified. Show all posts

Wednesday, March 8, 2023

Income and emotional well-being: A conflict resolved

Matthew A. Killingsworth, Daniel Kahneman, and Barbara Mellers explore the relationship between income and emotional well-being.

“Using dichotomous questions about the preceding day, [Kahneman and Deaton, Proc. Natl. Acad. Sci. U.S.A. 107, 16489–16493 (2010)] reported a flattening pattern: happiness increased steadily with log(income) up to a threshold and then plateaued. Using experience sampling with a continuous scale, [Killingsworth, Proc. Natl. Acad. Sci. U.S.A. 118, e2016976118 (2021)] reported a linear-log pattern in which average happiness rose consistently with log(income).”

Read more here.

Matthew A. Killingsworth, Daniel Kahneman, and Barbara Mellers explore the relationship between income and emotional well-being.

“Using dichotomous questions about the preceding day, [Kahneman and Deaton, Proc. Natl. Acad. Sci. U.S.A. 107, 16489–16493 (2010)] reported a flattening pattern: happiness increased steadily with log(income) up to a threshold and then plateaued. Using experience sampling with a continuous scale, [Killingsworth, Proc. Natl. Acad. Sci. U.S.A. 118, e2016976118 (2021)] reported a linear-log pattern in which average happiness rose consistently with log(income).”

Posted by at 9:43 AM

Labels: Inclusive Growth, Macro Demystified

Tuesday, December 27, 2022

Repost: Why immigration doesn’t reduce wages

From Noah Smith:

“With the return of the border crisis and Biden’s plans for a big new immigration reform, it looks like the immigration issue is heating up again. In the coming year we’re probably going to hear lots of very heated arguments from a lot of different angles, and I’m inevitably going to be blogging about some of these. But one aspect of the immigration debate that I feel like I’ve already dealt with pretty well is the question of wages.

A lot of people think immigration lowers wages for native-born Americans. This is true of both immigration opponents, but also of some supporters, who think an influx of workers will help restrain inflation. This is a natural thing to think, since everyone knows that immigration increases labor supply. But what fewer people realize is that immigration also raises labor demand, which tends to cancel out the downward pressure on wages. In late 2020 I wrote a post called “Why immigration doesn’t reduce wages”, in which I explained how this works and listed a bunch of the relevant evidence. I wanted it to be a useful and comprehensive guide that people could come back to again and again.

In this post, I’m going to explain why immigration doesn’t lower wages for native-born people (except possibly a little bit, in a few special circumstances). But before I do that, there’s one thing you really have to understand: No one is going to be persuaded by this post. There are two reasons for this.

First, people don’t really believe social science evidence. It took years and years of empirical research — solid results, almost all pointing in the same direction — just to shift academic economists’ opinions on the effects of minimum wage. The average person, not being an academic economist, has even less of an idea of how reliable social science research is.

Second, in my experience, anti-immigration people are completely set in their belief that immigration should be restricted. It’s their fixed north star. The justifications change — Lower wages! Environmental destruction! Brain drain! Rule of law! Cultural change! — but the policy conclusion never wavers. They know what they want to do.

So this post isn’t going to persuade anti-immigration people to change their stance, and it’s probably not going to persuade many normies to be up in arms about the need to let in more immigrants, either. But it’s still important to write, and not just because I’m a stubborn S.O.B. who will die face-down in the muck fighting for The Empirical Evidence. It’s because in another 20 years or so, when America’s current freakout over identity and nationhood has passed, we’re hopefully going to be ready to let in a bunch of immigrants again. And when that time finally comes, these arguments will matter.”

Continue reading here.

From Noah Smith:

“With the return of the border crisis and Biden’s plans for a big new immigration reform, it looks like the immigration issue is heating up again. In the coming year we’re probably going to hear lots of very heated arguments from a lot of different angles, and I’m inevitably going to be blogging about some of these. But one aspect of the immigration debate that I feel like I’ve already dealt with pretty well is the question of wages.

Posted by at 5:15 PM

Labels: Macro Demystified

Tuesday, November 8, 2022

Macroeconomics is still in its infancy

From Noah Smith:

“Ed Prescott, who was in some ways the father of modern macroeconomics, passed away recently at the age of 81. I thought this would be a good idea to write about the state of macro as a science. I used to write about this a lot when I first started blogging, so it’s a fun topic to revisit.

Macroeconomics has a bad reputation. I often see people whom I like and respect say stuff like this about the field of economics:

When they say this, I’m pretty sure they aren’t talking about the auction theorists whose models allowed Google to generate almost all of its ad revenue. And I’m pretty sure they aren’t talking about the matching theorists whose models improved kidney donation and saved countless lives. When people say “economists are still struggling to predict the last recession”, they’re talking about macroeconomists — the branch of econ that deals with big things like recessions, inflation, and growth.

It isn’t just pundits and commentators who are annoyed with the state of macro; economists in other fields often join in the criticism. For example, here’s Dan Hamermesh in 2011:

The economics profession is not in disrepute. Macroeconomics is in disrepute. The micro stuff that people like myself and most of us do has contributed tremendously and continues to contribute. Our thoughts have had enormous influence. It just happens that macroeconomics, firstly, has been done terribly and, secondly, in terms of academic macroeconomics, these guys are absolutely useless, most of them. Ask your brother-in-law. I’m sure he thinks, as do 90% of us, that most of what the macro guys do in academia is just worthless rubbish.

This is much harsher than I would put it, but it hints at some of the vicious internal battles being waged in the ivory tower. And even top macroeconomists are often quite upset at their field — see Paul Romer’s (extremely nerdy) 2015 broadside, “Mathiness in the Theory of Economic Growth”.

Ed Prescott’s generation of macroeconomists came into the field intent on fixing this situation.”

Continue reading here.

From Noah Smith:

“Ed Prescott, who was in some ways the father of modern macroeconomics, passed away recently at the age of 81. I thought this would be a good idea to write about the state of macro as a science. I used to write about this a lot when I first started blogging, so it’s a fun topic to revisit.

Macroeconomics has a bad reputation.

Posted by at 3:53 PM

Labels: Macro Demystified

Monday, August 22, 2022

Four reasons why GDP is a useful number

From Noah Smith:

“A lot of people like to criticize GDP as a measure of living standards. Among many intellectuals, particularly in the UK and some parts of North Europe, talking about the limitations of GDP and trying to think of better measures is something of a cottage industry:

Now, there are important senses in which these critics are right. GDP leaves out some things that are very important to human well-being — for example, leisure time, baseline health, inequality, natural habitats, and the value of unpaid housework and child care. And there are things it includes that some people might not want to include — the amount that government spends on tanks and bombs, for instance, or the fees people pay to lose their money in DeFi scams. There are even a few economists who say we shouldn’t even pay attention to GDP and that we should only care about consumption.

For this reason and others, it’s important not to get too obsessed with one single measure of the economy — GDP or anything else. You have to look at a bunch of measures to get a clear picture of what’s happening (in a 2018 Bloomberg post, I suggested also looking at real median personal income, prime-age employment rate, median real weekly earnings, and the Supplemental Poverty Measure). And in fact, I think policymakers and media figures all over the world already look at lots of different numbers.

But today I just want to focus on GDP, because the critics have sorely overstated their case. In fact, GDP is an incredibly useful and important number, for a variety of reasons.

GDP is actually just a measure of income

First, I think that understanding what GDP actually is helps us understand why it’s important. Critics of the concept sometimes seem to lack a basic understanding of what the number even means.

GDP is a measure of the total amount of economic value produced in a country. We measure economic value by how much people pay for stuff. If you pay $100 for a new toaster, GDP goes up by $100. If the government pays $1M for a tank, GDP goes up by $1M.

Now, it can be hard to understand why we’d care about measuring things this way. Just because people pay $100 for something, does that mean it was really worth $100? And on top of that, it can get a little complicated, because there are some things we buy that aren’t included in GDP — intermediate goods (like parts to make a car), used goods, financial assets like stocks and bonds, etc. Explaining these things would take a whole economics lesson.

But instead, there’s an easier way to think about GDP and what it means. Really, it’s just a measure of people’s incomes.”

Continue reading here.

From Noah Smith:

“A lot of people like to criticize GDP as a measure of living standards. Among many intellectuals, particularly in the UK and some parts of North Europe, talking about the limitations of GDP and trying to think of better measures is something of a cottage industry:

Now, there are important senses in which these critics are right. GDP leaves out some things that are very important to human well-being — for example,

Posted by at 8:15 AM

Labels: Macro Demystified

Monday, August 15, 2022

A Fertility Patterns Flip-flop

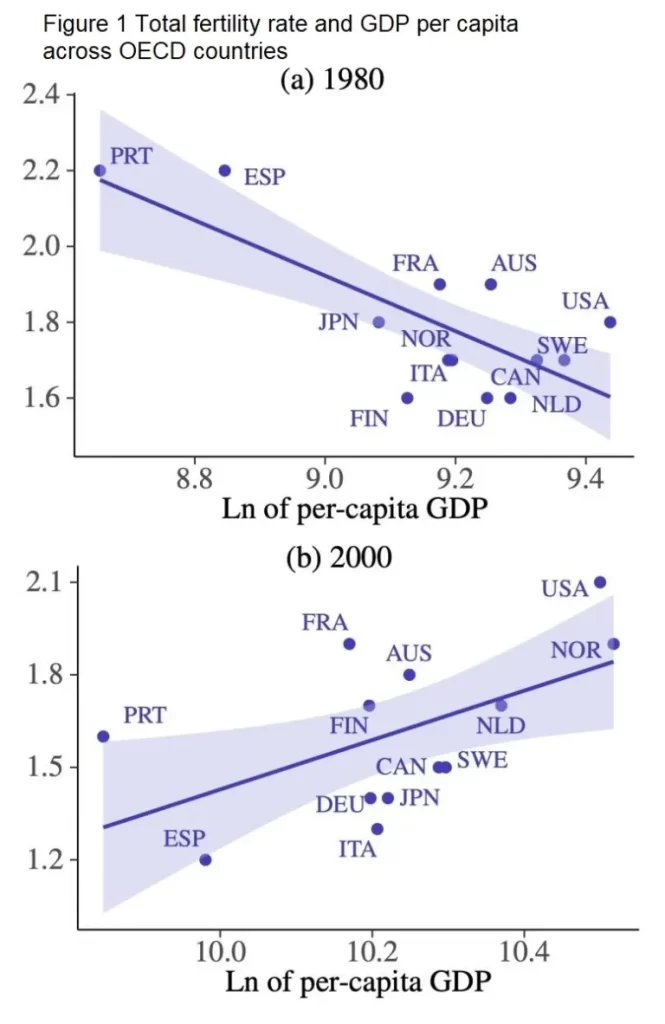

From Conversable Economist:

“For some decades now, the world has been following the patterns of a demographic transition with life expectancies rising and birth rates falling, as we head for a world where the elderly are a much larger share of the global population. However, Matthias Doepke, Anne Hannusch, Fabian Kindermann, and Michèle Tertilt argue that it’s time for “The New Economics of Fertility” (IZA Discussion Paper #15224, April 2022). For a short readable overview of the main themes, you can check their shorter discussion at the VoxEU website (June 11, 2022).

From the abstract of the academic paper, the authors write:

In this survey, we argue that the economic analysis of fertility has entered a new era. First-generation models of fertility choice were designed to account for two empirical regularities that, in the past, held both across countries and across families in a given country: a negative relationship between income and fertility, and another negative relationship between women’s labor force participation and fertility. The economics of fertility has entered a new era because these stylized facts no longer universally hold. In high-income countries, the income-fertility relationship has flattened and in some cases reversed, and the cross-country relationship between women’s labor force participation and fertility is now positive.

A couple of pictures may help, here. It used to be that countries with higher incomes had lower fertility rates, but among high-income countries, this pattern no longer holds. Here’s a figure taken from the VoxEU overview. The top panel shows that within the group of high-income countries in 1980, countries with higher per capita GDP had lower fertility, but by 2000, countries in this group with higher per capita income had higher fertility.”

Continue reading here.

From Conversable Economist:

“For some decades now, the world has been following the patterns of a demographic transition with life expectancies rising and birth rates falling, as we head for a world where the elderly are a much larger share of the global population. However, Matthias Doepke, Anne Hannusch, Fabian Kindermann, and Michèle Tertilt argue that it’s time for “The New Economics of Fertility” (IZA Discussion Paper #15224,

Posted by at 6:09 AM

Labels: Macro Demystified

Subscribe to: Posts