Showing posts with label Macro Demystified. Show all posts

Tuesday, December 11, 2018

Media Sentiment and International Asset Prices

From a new IMF working paper by Samuel P. Fraiberger, ; Do Lee, Damien Puy, and Romain Ranciere:

“We assess the impact of media sentiment on international equity prices using more than 4.5 million Reuters articles published across the globe between 1991 and 2015. News sentiment robustly predicts daily returns in both advanced and emerging markets, even after controlling for known determinants of stock prices. But not all news-sentiment is alike. A local (country-specific) increase in news optimism (pessimism) predicts a small and transitory increase (decrease) in local returns. By contrast, changes in global news sentiment have a larger impact on equity returns around the world, which does not reverse in the short run. We also find evidence that news sentiment affects mainly foreign – rather than local – investors: although local news optimism attracts international equity flows for a few days, global news optimism generates a permanent foreign equity inflow. Our results confirm the value of media content in capturing investor sentiment.”

From a new IMF working paper by Samuel P. Fraiberger, ; Do Lee, Damien Puy, and Romain Ranciere:

“We assess the impact of media sentiment on international equity prices using more than 4.5 million Reuters articles published across the globe between 1991 and 2015. News sentiment robustly predicts daily returns in both advanced and emerging markets, even after controlling for known determinants of stock prices. But not all news-sentiment is alike.

Posted by at 10:01 AM

Labels: Macro Demystified

Friday, November 30, 2018

Finding Success

From the IMF’s Finance & Development magazine:

“Assaf Razin’s Israel and the World Economy shows that globalization can be a powerful force for economic progress in the case of a country with the institutions and policies to take advantage of the possibilities of an open economy. As depicted in this comprehensive and accessible book, Israel’s strong growth since its stabilization from high inflation in 1985 owes much to an international economy in which capital, labor, and ideas are mobile and in which trade and investment flow readily across far-flung international borders.

Razin explains that where other countries have experienced problems with globalization, Israel has found success. Large capital inflows are understandably viewed as dangerous in emerging markets living with memories of recent currency crises: in Israel foreign capital provided crucial funding for investment in the country’s showcase technology sector. Israel is now solidly established as a high-tech powerhouse—a place where budding venture capitalists from emerging market countries flock to learn how to develop an innovation ecosystem. But the domestic market alone is far too small and homegrown capital formation insufficient to foster that innovation. Globalization has been essential.

Similarly, immigration is a hot-button issue in the United States and in some countries in Europe but a source of growth in Israel. This is because a massive influx of skilled immigrants from the former Soviet Union starting in 1989 led to a surge in productivity, propelling Israel to medium- to high-income status, capped by membership in the Organisation for Economic Co-operation and Development in 2010. And Razin shows that this productivity boom translated into higher wages even for domestic workers who might otherwise have been harmed by the increased labor supply.

There is a sense in which this is three books in one. First, Razin explains the intuition and policy implications of a more globalized world across a range of topics, including migration, inequality, capital flows, currency crises, international trade, and more. The book then connects each topic to developments in the Israeli economy, portraying both successes and challenges in light of the underlying theory. Last, each chapter includes self-contained technical expositions of key models with which to analyze these economic phenomena, making this a text to be considered for a rigorous course on international economic policy.

It is not that Razin thinks Israel has done everything right—far from it. He covers rising inequality within Israeli society, the low participation rates and levels of skills among the fastest-growing segments of the population, the problem of brain drain as highly educated Israelis move abroad, and the costs associated with Israel’s security challenges, including a chapter on the “Rising Cost of Occupation.”

Still, even with Razin’s frankness about the potential pitfalls, his book is an ode to the potential benefits of good economic policy, to economic models through which to examine policy, and to Israel’s astonishing economic success.”

From the IMF’s Finance & Development magazine:

“Assaf Razin’s Israel and the World Economy shows that globalization can be a powerful force for economic progress in the case of a country with the institutions and policies to take advantage of the possibilities of an open economy. As depicted in this comprehensive and accessible book, Israel’s strong growth since its stabilization from high inflation in 1985 owes much to an international economy in which capital,

Posted by at 3:59 PM

Labels: Macro Demystified

Thursday, November 29, 2018

Global uncertainty is rising, and that is a bad omen for growth

From VoxEU:

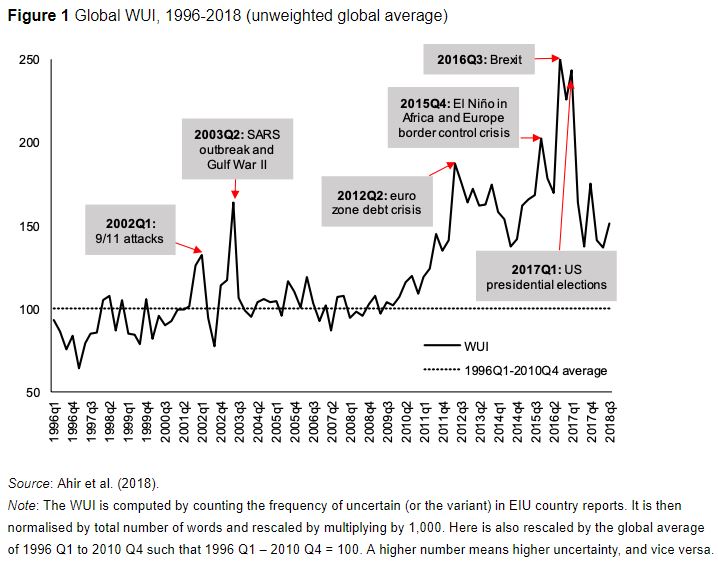

“The global economy is growing, but so is uncertainty. This column presents a new quarterly index of uncertainty for 143 countries. The World Uncertainty Index reveals how uncertainty in the world has evolved over time, whether it is synchronised across countries, and how it compares across income groups and political regimes.

The October 2018 edition of the World Economic Outlook predicts that global economic growth will remain steady between 2018 and 2020 at the 2017 growth rate of 3.7% (IMF 2018). This exceeds the growth rate in any year between 2012 and 2016.

So, the global economy is growing, but so is uncertainty. Headlines that have appeared in the Financial Times in 2018 include: “Stocks unsettled by global trade uncertainty”, “Counting the costs of Brexit uncertainty”, “Latin America faces up to growing uncertainties”, “Italian bonds under pressure from budget uncertainty”, and “Boeing deal with Embraer faces political uncertainty”.

A Google news search for “uncertainty” gives about 0.6 million results for the whole of 2017, but 2.5 million results for the first ten months of 2018. Can we measure ‘uncertainty’ more precisely? Or compare the amount of ‘uncertainty’ in the US to that in China, the UK, or Ireland?

Measurements of economic and political uncertainty have been made only for a set of mostly advanced economies (Baker et al. 2016). We have constructed a new index of uncertainty for 143 countries using Economist Intelligence Unit (EIU) country reports. To the best of our knowledge, this is the first effort to construct a panel index of uncertainty for a large set of developed and developing countries.

Constructing the World Uncertainty Index

We constructed the World Uncertainty Index (WUI) – a quarterly index of uncertainty – for 143 individual countries from 1996 onwards. The WUI is defined using the frequency of the word ‘uncertainty’ (and its variants) in the quarterly EIU country reports. To make the WUI comparable across countries, the raw count is scaled by the total number of words in each report.

In contrast to existing measure of economic policy uncertainty, two factors help improve the comparability of the WUI across countries:

- The WUI is based on a single source. This source has specific topic coverage – economic and political developments.

- Reports follow a standardised process and structure.

The process through which the EIU country reports are produced helps to mitigate concerns about the accuracy, ideological bias, and consistency of the WUI. But we only have one EIU report per country per quarter, meaning there is potentially quite large sampling noise.

Stylised facts

This dataset allows us to establish five key facts:

1. Global uncertainty has increased significantly since 2012. Figure 1 shows that average uncertainty has increased since 2012, well above its historical average (computed between 1996 Q1 and 2010 Q4). The index spikes near the 9/11 attacks, the SARS outbreak, the second Gulf War, the euro area debt crisis, El Niño, the Europe border-control crisis, the UK referendum vote for Brexit, and the US presidential elections.

Interestingly, while text-based measures of uncertainty have been rising since the early 2000s, financial market measures rose until about 2010, but have fallen back to low levels (Pastor and Veronesi 2017).

Continue reading here.

From VoxEU:

“The global economy is growing, but so is uncertainty. This column presents a new quarterly index of uncertainty for 143 countries. The World Uncertainty Index reveals how uncertainty in the world has evolved over time, whether it is synchronised across countries, and how it compares across income groups and political regimes.

The October 2018 edition of the World Economic Outlook predicts that global economic growth will remain steady between 2018 and 2020 at the 2017 growth rate of 3.7% (IMF 2018).

Posted by at 10:46 AM

Labels: Macro Demystified

Sunday, November 25, 2018

A New Canadian Macroeconomic Database

From a new post by Dave Giles:

“Anyone who’s undertaken empirical macroeconomic research relating to Canada will know that there are some serious data challenges that have to be surmounted.

In particular, getting access to long-term, continuous, time series isn’t as easy as you might expect.

Statistics Canada has been criticized frequently over the years by researchers who find that crucial economic series are suddenly “discontinued”, or are re-defined in ways that make it extremely difficult to splice the pieces together into one meaningful time-series.

In recognition of these issues, a number of efforts have been made to provide Canadian economic data in forms that researchers need. These include, for instance, Boivin et al. (2010), Bedock and Stevanovic (2107), and Stephen Gordon’s on-going “Project Link“.

Thanks to Olivier Fortin-Gagnon, Maxime Leroux, Dalibor Stevanovic, &and Stéphane Suprenant we now have an impressive addition to the available long-term Canadian time-series data. Their 2018 working paper, “A Large Canadian Database for Macroeconomic Analysis“, discusses their new database and illustrates its usefulness in a variety of ways.”

From a new post by Dave Giles:

“Anyone who’s undertaken empirical macroeconomic research relating to Canada will know that there are some serious data challenges that have to be surmounted.

In particular, getting access to long-term, continuous, time series isn’t as easy as you might expect.

Statistics Canada has been criticized frequently over the years by researchers who find that crucial economic series are suddenly “discontinued”,

Posted by at 1:08 PM

Labels: Macro Demystified

Saturday, November 24, 2018

Solow on Friedman’s 1968 Presidential Address and the Medium Run

From a new post by Timothy Taylor:

“Robert Solow is a notable player in these disputes: in particular, in his 1960 paper with Paul Samuelson, “Analytical Aspects of Anti-Inflation Policy” (American Economic Review, 50:2, pp. 177-194). In an essay in the Winter 2000 issue of the Journal of Economic Perspectives, “Toward a Macroeconomics of the Medium Run,” Solow addressed this question of thinking about macroeconomic policy in the short- and the long-run. He wrote:

I can easily imagine that there is a “true” macrodynamics, valid at every time scale. But it is fearfully complicated, and nobody has a very good grip on it. At short time scales, I think, something sort of “Keynesian” is a good approximation, and surely better than anything straight “neoclassical.” At very long time scales, the interesting questions are best studied in a neoclassical framework, and attention to the Keynesian side of things would be a minor distraction. At the five-to-ten-year time scale, we have to piece things together as best we can, and look for a hybrid model that will do the job.

In this most recent essay, “A Theory is a Sometime Thing,” Solow pushes this idea of medium-run thinking harder. He acknowledges that if a central bank can only cause the interest rate and unemployment rate to shift for a year or two, in the short-run before a rebound to what is determined in the long run, then when problems of lags in timing are included, macroeconomic policy might be dysfunctional. But if a central bank can affect the interest rate and the unemployment rate for a medium-run period of, say 5-7 years, then even with some uncertainty and lags, macroeocnomic policy may be quite relevant and possible. At one point, Solow writes: “The medium run is where we live.””

From a new post by Timothy Taylor:

“Robert Solow is a notable player in these disputes: in particular, in his 1960 paper with Paul Samuelson, “Analytical Aspects of Anti-Inflation Policy” (American Economic Review, 50:2, pp. 177-194). In an essay in the Winter 2000 issue of the Journal of Economic Perspectives, “Toward a Macroeconomics of the Medium Run,” Solow addressed this question of thinking about macroeconomic policy in the short- and the long-run.

Posted by at 7:30 PM

Labels: Macro Demystified

Subscribe to: Posts