Showing posts with label Macro Demystified. Show all posts

Monday, January 10, 2022

Clubs and Networks in Economics Reviewing

Source: NBER Working Paper (2022)

“Results show that clubs and networks play a large role in influencing both editor and reviewer decisions. Authors who attended the same PhD program, were ever colleagues with, are affiliates of the same NBER program(s), or are more closely linked via coauthorship networks as the handling editor are significantly more likely to avoid a desk rejection. Likewise, authors from the same PhD program or who previously worked with the reviewer are significantly more likely to receive a positive evaluation. We also find that sharing “signals” of ability, such as publishing in “top five”, attending a high ranked PhD program, or being employed by a similarly ranked economics department significantly influences editor decisions and/or reviewer recommendations.”

Source: NBER Working Paper (2022)

“Results show that clubs and networks play a large role in influencing both editor and reviewer decisions. Authors who attended the same PhD program, were ever colleagues with, are affiliates of the same NBER program(s), or are more closely linked via coauthorship networks as the handling editor are significantly more likely to avoid a desk rejection. Likewise, authors from the same PhD program or who previously worked with the reviewer are significantly more likely to receive a positive evaluation.

Posted by at 11:37 AM

Labels: Macro Demystified

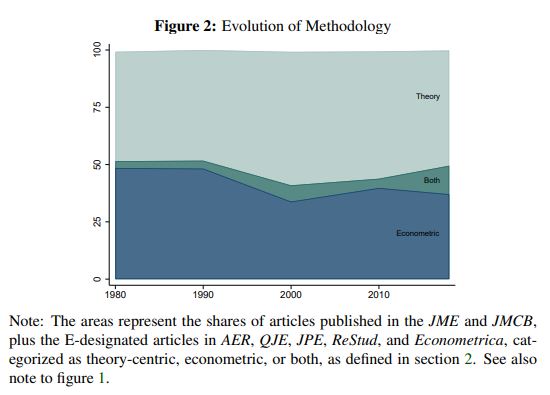

Macroeconomic Research, Present and Past

From a new NBER paper by Philip J. Glandon, Kenneth Kuttner, Sandeep Mazumder & Caleb Stroup:

“How is macroeconomic research conducted and what is it trying to accomplish? We explore these questions using information gleaned from 1,894 articles published in ten leading journals. We find that over the past 40 years there has been a growing emphasis on increasingly sophisticated quantitative theory, such as DSGE modeling, and papers employing these methods now account for the majority of articles in macro journals. The shift towards quantitative theory is mirrored by a decline in the use of econometric methods to test economic hypotheses. Econometric techniques borrowed from applied microeconomics have to a large extent displaced time series methods, and empirical papers increasingly rely on micro and proprietary data sources. Market imperfections are pervasive, and the amount of research involving financial frictions has increased significantly in the past ten years. The frequency with which non-macro JEL codes appear in macro articles indicates a great deal of overlap between macroeconomics and other fields.”

From a new NBER paper by Philip J. Glandon, Kenneth Kuttner, Sandeep Mazumder & Caleb Stroup:

“How is macroeconomic research conducted and what is it trying to accomplish? We explore these questions using information gleaned from 1,894 articles published in ten leading journals. We find that over the past 40 years there has been a growing emphasis on increasingly sophisticated quantitative theory, such as DSGE modeling, and papers employing these methods now account for the majority of articles in macro journals.

Posted by at 11:14 AM

Labels: Macro Demystified

Saturday, January 8, 2022

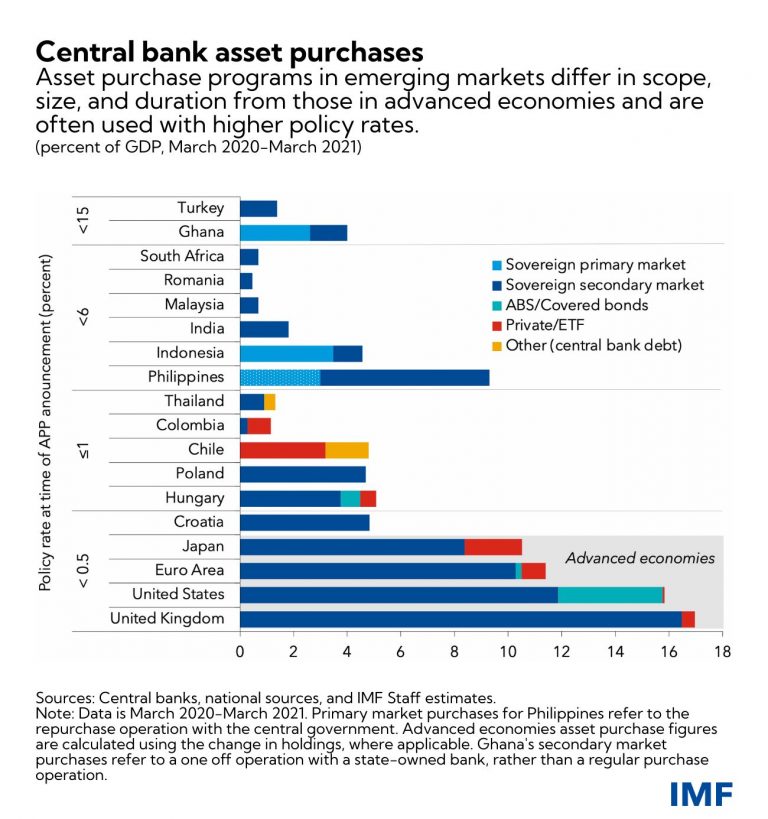

Emerging-Market Central Bank Purchases Can be Effective but Carry Risks

In a new IMF blog (2022), Tobias Adrian et al write about the effectiveness and risks of counter-cyclical monetary policy measures taken by central banks in emerging markets, specifically asset purchases.

‘Targeted asset purchases helped emerging markets manage financial distress during the COVID-19 crisis without noticeable capital outflow and exchange rate pressures but also pose significant risks, including the risk to central banks’ own balance sheets and governments pressuring central banks to act in a certain way’. It then goes on to discuss some principles for asset purchases and direct financing that may help central banks override this problem.

Click here to read the full blog.

In a new IMF blog (2022), Tobias Adrian et al write about the effectiveness and risks of counter-cyclical monetary policy measures taken by central banks in emerging markets, specifically asset purchases.

‘Targeted asset purchases helped emerging markets manage financial distress during the COVID-19 crisis without noticeable capital outflow and exchange rate pressures but also pose significant risks, including the risk to central banks’ own balance sheets and governments pressuring central banks to act in a certain way’.

Posted by at 9:29 AM

Labels: Macro Demystified

Friday, January 7, 2022

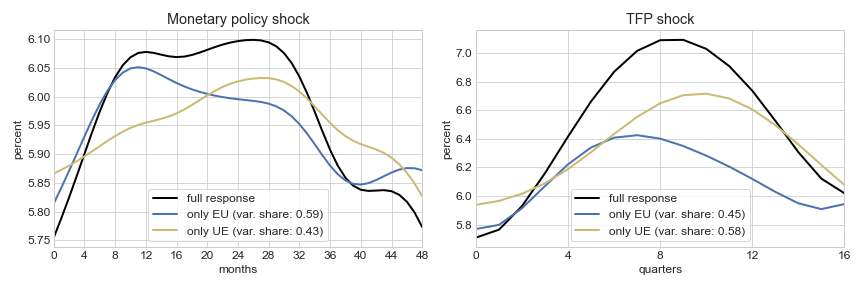

The unemployment-risk channel in business cycle fluctuations

Source: VoxEU CEPR

“Early signs of a recession can lead to a negative feedback loop, with workers’ concerns about unemployment dampening demand and thus deepening the recession. This column uses a heterogeneous agent model to quantify the importance of the ‘unemployment-risk’ channel for business cycle fluctuations in the US economy. It shows that the channel accounts for around one-third of observed unemployment fluctuations. As the demand amplification through precautionary savings is inefficient, this finding provides an additional rationale for stabilisation policies by policymakers. “

Figure: Estimated response of unemployment to monetary policy and total factor productivity (TFP) shocks

Click here to read the full article.

Source: VoxEU CEPR

“Early signs of a recession can lead to a negative feedback loop, with workers’ concerns about unemployment dampening demand and thus deepening the recession. This column uses a heterogeneous agent model to quantify the importance of the ‘unemployment-risk’ channel for business cycle fluctuations in the US economy. It shows that the channel accounts for around one-third of observed unemployment fluctuations. As the demand amplification through precautionary savings is inefficient, this finding provides an additional rationale for stabilisation policies by policymakers.

Posted by at 11:08 AM

Labels: Inclusive Growth, Macro Demystified

Wednesday, January 5, 2022

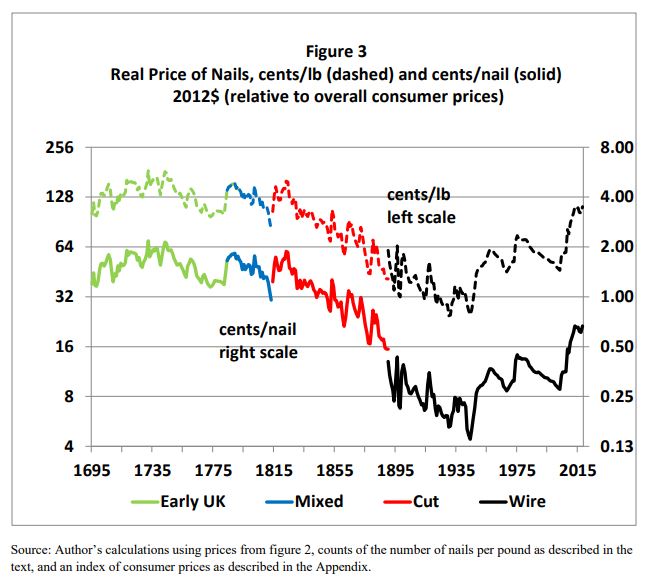

The Price of Nails since 1695: A Window into Economic Change

From a NBER paper by Daniel E. Sichel:

“This paper focuses on the price of nails since 1695 and the proximate source of changes in those prices. Why nails? They are a basic manufactured product whose form and quality have changed relatively little over the last three centuries, yet the process for producing them has changed dramatically. Accordingly, nails provide a useful prism through which to examine a wide range of economic and technological developments that touch on multiple areas of both micro- and macroeconomics. Several conclusions emerge. First, from the late 1700s to the mid 20th century real nail prices fell by a factor of about 10 relative to overall consumer prices. These declines had important effects on downstream industries, most notably construction. Second, while declining materials prices contribute to reductions in nail prices, the largest proximate source of the decline during this period was multifactor productivity growth in nail manufacturing, highlighting the role of the specialization of labor and re-organization of production processes. Third, the share of nails in GDP dropped back from 0.4 percent of GDP in 1810—comparable to today’s share of household purchases of personal computers—to a de minimis share more recently; accordingly, nails played a bigger role in American life in that earlier period. Finally, real nail prices have increased since the mid 20th century, reflecting in part an upturn in materials prices and a shift toward specialty nails in the wake of import competition, though the introduction of nail guns partly offset these increases for the price of installed nails.”

From a NBER paper by Daniel E. Sichel:

“This paper focuses on the price of nails since 1695 and the proximate source of changes in those prices. Why nails? They are a basic manufactured product whose form and quality have changed relatively little over the last three centuries, yet the process for producing them has changed dramatically. Accordingly, nails provide a useful prism through which to examine a wide range of economic and technological developments that touch on multiple areas of both micro- and macroeconomics.

Posted by at 8:56 AM

Labels: Macro Demystified

Subscribe to: Posts