Showing posts with label Inclusive Growth. Show all posts

Tuesday, January 21, 2020

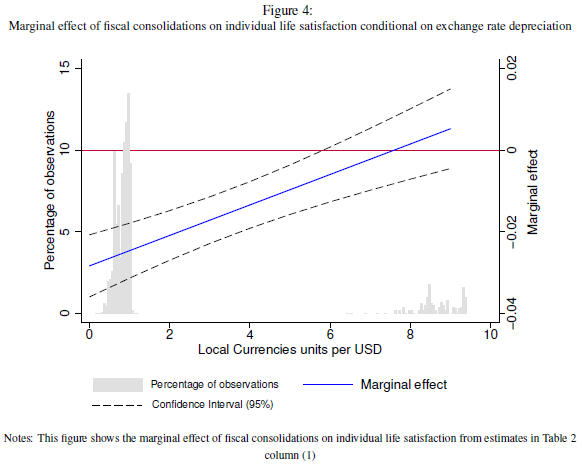

The (Subjective) Well-Being Cost of Fiscal Policy Shocks

From a new paper by IMF colleagues Kodjovi M. Eklou and Mamour Fall:

“Do discretionary spending cuts and tax increases hurt social well-being? To answer this question, we combine subjective well-being data covering over half a million of individuals across 13 European countries, with macroeconomic data on fiscal consolidations. We find that fiscal consolidations reduce individual well-being in the short run, especially when they are based on spending cuts. In addition, we show that accompanying monetary and exchange rate policies (disinflation, depreciations and the liberalization of capital flows) mitigate the well-being cost of fiscal consolidations. Finally, we investigate the well-being consequences of the two well-knowns expansionary fiscal consolidations episodes taking place in the 80s (in Denmark and Ireland). We find that even expansionary fiscal consolidations can have well-being costs. Our results may therefore shed some light on why some governments may choose to consolidate through taxes even at the cost of economic growth. Indeed, if spending cuts are to generate a large well-being loss, they can trigger an opposition and protest against a fiscal consolidation plan and hence making it politically costly.”

“Figure 4 depicts the effect of a 1 percentage point of GDP increase in the size of a fiscal consolidation conditional on being accompanied by different level of depreciation in the sample. Figure 4 shows that for higher levels of depreciation, that is for ratios of at least 6 units of local currencies per USD, fiscal consolidations do not have any statistically significant effect on well-being.”

From a new paper by IMF colleagues Kodjovi M. Eklou and Mamour Fall:

“Do discretionary spending cuts and tax increases hurt social well-being? To answer this question, we combine subjective well-being data covering over half a million of individuals across 13 European countries, with macroeconomic data on fiscal consolidations. We find that fiscal consolidations reduce individual well-being in the short run, especially when they are based on spending cuts. In addition,

Posted by at 9:55 AM

Labels: Inclusive Growth

Friday, January 17, 2020

Finance and Inequality

From a new paper by IMF colleagues–Martin Cihak and Ratna Sahay:

“Global income inequality has fallen in the past two decades, in large part due to major strides in emerging market and developing economies to raise economic growth rates and reduce poverty. Financial sector policies and advances in financial technology are enabling financial inclusion, particularly in large economies such as China and India, allowing an increasing number of low-income households and small businesses to participate productively in the formal economy.

At the same time, we observe rising or high disparities in income and wealth within many countries. New data also show that economic mobility—the ability of the less well-off to improve their economic status—has stalled in recent decades. No wonder then that inequality of income, wealth, and opportunities is giving rise to populism and anti-globalization sentiments in some countries.

Can the financial sector play a role in reducing inequality? This study makes the case that it can, complementing redistributive fiscal policy in mitigating inequality. By expanding the provision of financial services to low-income households and small businesses, it can serve as a powerful lever in helping create a more inclusive society but—if not well managed—it can also amplify inequalities.

Our study examines empirical relationships between income inequality and three features of finance: depth (financial sector size relative to the economy), inclusion (access to and use of financial services by individuals and firms), and stability (absence of financial distress). We ask three questions.

First, does greater financial depth mean lower or higher inequality within countries? Building on new data sets, our analysis suggests that initially financial depth is associated with lower inequality, but only up to a point, after which inequality rises.

Second, does greater financial inclusion mean lower inequality within countries? We find that greater financial inclusion is associated with reductions in inequality. For payment services, we find evidence that benefits from inclusion are greater for those at the low end of the income distribution, reducing inequality. Both men and women benefit from financial inclusion, but inequality falls more when women have greater access. As regards access to and use of credit, the results are mixed.

Third, is there a relationship between stability and inequality within countries? Our study finds that higher inequality is associated with greater financial risks. Increases in inequality tend to be accompanied by higher growth in credit. For example, in the United States, too much credit, including to lower-income households, contributed to the 2008 crisis. Crises, in turn, lead to higher default rates, making lower-income households worse off and increasing inequality after a crisis.

Our key takeaway is that finance can help reduce inequality but is also associated with greater inequality if the financial system is not well managed. Our findings have five policy implications. First, financial inclusion policies help reduce inequality. Second, there is a case for promoting women’s financial inclusion, as inequality falls even more when policies are inclusive of women. Third, regulatory policies have a role to play in reining in excessive growth of the financial sector. Fourth, provided quality of regulation and supervision is high, financial inclusion and stability can be pursued simultaneously. Fifth, financial sector policies are a complement, not a substitute, for other policy tools—fiscal and macro-structural policies are still needed to help address inequality.”

From a new paper by IMF colleagues–Martin Cihak and Ratna Sahay:

“Global income inequality has fallen in the past two decades, in large part due to major strides in emerging market and developing economies to raise economic growth rates and reduce poverty. Financial sector policies and advances in financial technology are enabling financial inclusion, particularly in large economies such as China and India, allowing an increasing number of low-income households and small businesses to participate productively in the formal economy.

Posted by at 10:58 AM

Labels: Inclusive Growth

Tuesday, December 17, 2019

Quality Upgrading and Export Performance in the Asian Growth Miracle

Interesting paper by Chris Papageorgiou , Fidel Perez-Sebastian and Nikola Spatafora:

“We explore the contribution of product-quality upgrading to the export performance of six fast-growing Asian economies: China, India, Indonesia, Malaysia, South Korea, and Thailand. We focus on measuring the impact of quality upgrading on the changes in these countries’ sectoral export shares during 1970–2010. We build a multisector Ricardian trade model which allows for changes in product quality, and calibrate it to generate predictions about export volumes. Unlike previous literature, our approach allows estimation without employing domestic production data. Our results point to quality upgrading being a key driver of export shares.”

Interesting paper by Chris Papageorgiou , Fidel Perez-Sebastian and Nikola Spatafora:

“We explore the contribution of product-quality upgrading to the export performance of six fast-growing Asian economies: China, India, Indonesia, Malaysia, South Korea, and Thailand. We focus on measuring the impact of quality upgrading on the changes in these countries’ sectoral export shares during 1970–2010. We build a multisector Ricardian trade model which allows for changes in product quality,

Posted by at 6:19 PM

Labels: Inclusive Growth

Monday, December 16, 2019

The Old Boys’ Club: Schmoozing and the Gender Gap

From a new working paper by Zoe Cullen (Harvard University) and Ricardo Perez-Truglia (UCLA):

“The old boys’ club refers to the alleged advantage that male employees have over their female counterparts in interacting with powerful men. For example, male employees may schmooze with their managers in ways that female employees cannot. We study this phenomenon using data from a large financial institution. We use an event study analysis of manager rotation to estimate the causal effect of managers’ gender on their employees’ career progression. We find that when male employees are assigned to male managers, they are promoted faster in the following years than they would have been if they were assigned to female managers. Female employees, on the contrary, have the same career progression regardless of the manager’s gender. These differences in career progression cannot be explained by differences in effort or output. This male-to-male advantage can explain a third of the gender gap in promotions. Moreover, we provide suggestive evidence that these manager effects are due to socialization between male employees and male managers. We show that these manager effects are present only if the employee works in close proximity to the manager. We use survey data to show that, after transitioning to a male manager, male employees spend more time with their managers. Finally, we study a shock to socialization within males, based on the anecdotal evidence that employees who smoke tend to spend more time together. We find that when male employees who smoke switch to male managers who smoke, they spend more of their breaks with their managers and are promoted faster in the following years. Moreover, the effects of these smoking manager switches are similar in timing and magnitude to the effects of the gender manager switches.”

From a new working paper by Zoe Cullen (Harvard University) and Ricardo Perez-Truglia (UCLA):

“The old boys’ club refers to the alleged advantage that male employees have over their female counterparts in interacting with powerful men. For example, male employees may schmooze with their managers in ways that female employees cannot. We study this phenomenon using data from a large financial institution. We use an event study analysis of manager rotation to estimate the causal effect of managers’

Posted by at 10:19 AM

Labels: Inclusive Growth

Monday, December 9, 2019

China’s Productivity Convergence and Growth Potential—A Stocktaking and Sectoral Approach

Interesting research paper by Min Zhu , Longmei Zhang and Daoju Peng:

“China’s growth potential has become a hotly debated topic as the economy has reached an income level susceptible to the “middle-income trap” and financial vulnerabilities are mounting after years of rapid credit expansion. However, the existing literature has largely focused on macro level aggregates, which are ill suited to understanding China’s significant structural transformation and its impact on economic growth. To fill the gap, this paper takes a deep dive into China’s convergence progress in 38 industrial sectors and 11 services sectors, examines past sectoral transitions, and predicts future shifts. We find that China’s productivity convergence remains at an early stage, with the industrial sector more advanced than services. Large variations exist among subsectors, with high-tech industrial sectors, in particular the ICT sector, lagging low-tech sectors. Going forward, ample room remains for further convergence, but the shrinking distance to the frontier, the structural shift from industry to services, and demographic changes will put sustained downward pressure on growth, which could slow to 5 percent by 2025 and 4 percent by 2030. Digitalization, SOE reform, and services sector opening up could be three major forces boosting future growth, while the risks of a financial crisis and a reversal in global integration in trade and technology could slow the pace of convergence.”

Interesting research paper by Min Zhu , Longmei Zhang and Daoju Peng:

“China’s growth potential has become a hotly debated topic as the economy has reached an income level susceptible to the “middle-income trap” and financial vulnerabilities are mounting after years of rapid credit expansion. However, the existing literature has largely focused on macro level aggregates, which are ill suited to understanding China’s significant structural transformation and its impact on economic growth.

Posted by at 1:57 PM

Labels: Inclusive Growth

Subscribe to: Posts