Showing posts with label Inclusive Growth. Show all posts

Wednesday, April 1, 2020

The Economic Consequences of the Virus: Views of Top Macroeconomists

- Several macroeconomists—using evidence from previous pandemics or calculations based on economic models—have provided estimates of the likely impact of the coronavirus on the economy. They agree that the economic policies announced by governments, plus the containment and lockdowns, are a small price to pay to limit the deaths from COVID-19.

- In recent articles, Joseph Stiglitz, Robert Barro and the IMF all stress the importance of extending unemployment insurance benefits, maintaining the connections between companies and workers, providing cash to those with low incomes—which is broadly the focus of policies announced by governments.

- These views by mainstream macroeconomists stand in stark contrast to the views of people such as Richard Epstein at the Hoover Institute so argued on March 30 that “the only solution that has a prayer of working [in the United States] is to ease restrictions as quickly as possible in those areas where the risks are lower” and that a “fortress America approach … may turn out to be more deadly than the coronavirus itself.”

Views on economic policies:

Joseph Stiglitz: The U.S. $2 trillion stimulus package is “remarkably good” and has several provisions that “are really important to ordinary Americans.” These include: (i) strengthening the unemployment insurance system; (ii) encouraging firms not to simply lay off or to get rid of their workers, leaving them without health insurance, but keeping the connection between the workers and the workplace alive by providing money to corporations to pay for the furloughed workers so they’re not left on their own; (iii) providing cash for those with very limited income that are not in one of the other two previous programs; (iv) providing loans to small businesses provided that they maintain their employment levels.

Robert Barro writes that policies should “prevent individuals who lose jobs from having little income to use for basic purchases [by] strengthening the existing social safety net” by increasing “accessibility and benefit levels for programs such as unemployment insurance, food stamps, and Medicaid. These program expansions, some of which are in the massive relief package that just passed Congress, are much more targeted to the needy than the policy of passing out $1,200 checks to everyone.” He continues that “it also makes sense that the recent package includes various policies aimed at limiting the permanent disappearance of businesses that would be productive absent the ongoing crisis. And it’s critical for the Federal Reserve to prevent major disruptions of financial markets, which it is already aggressively attempting to do.” If mortality from the current virus turns out to be similar to that of the Great Influenza Pandemic of 1918–1920, there could be 150 million deaths across the world: saving lives even at the expense of cutting world GDP by 20 percent through containment measures and lockdowns “is more than worth the cost.”

The IMF: “Households who lose their income directly or indirectly because of containment measures will need government support. Support should help people stay at home while keeping their jobs. Unemployment benefits should be expanded and extended. Cash transfers are needed to reach the self-employed and those without jobs. … Policies need to safeguard the web of relations among workers and employers, producers and consumers, lenders and borrowers, so that business can resume in earnest when the medical emergency abates. Company closures would cause loss of organizational know-how and termination of productive long-term projects. Disruptions in the financial sector would also amplify economic distress. Governments need to provide exceptional support to private firms, including wage subsidies, with appropriate conditions.”

Estimates of economic impacts of COVID-19:

Robert Barro and co-authors: “The implications of our findings from the Great Influenza Epidemic [of 1918-20] for the ongoing coronavirus epidemic are unsettling. … The flu death rate of 2.0 percent translates into 150 million deaths worldwide when applied to the world’s population of around 7.5 billion in 2020. Further, this death rate corresponds … to declines in the typical country by 6 percent for GDP and 8 percent for consumption. These economic declines are comparable to those last seen during the global Great Recession of 2008-2009 … Although these outcomes for the coronavirus are only possibilities, corresponding to plausible worst-case scenarios, the large potential losses in lives and economic activity justify substantial outlays to attempt to limit the damage.”

Martin Eichenbaum, Sergio Rebelo, and Mathias Trabandt write that “decisions to cut back on consumption and work reduce the severity of the epidemic as measured by total deaths. These same decisions exacerbate the size of the recession caused by the epidemic. An epidemic has both aggregate demand and aggregate supply effects. The supply effect arises because the epidemic exposes people who are working to the virus. People react to that risk by reducing their labor supply. The demand effect arises because the epidemic exposes people who are purchasing consumption goods to the virus. People react to that risk by reducing their consumption. The supply and demand effects work together to generate a large, persistent recession.

What policies should the government pursue? The authors write that “containment policies that reduce consumption and hours worked … exacerbate the recession but raise welfare by reducing the death toll caused by the epidemic. We find that it is optimal to introduce large-scale containment measures that result in a sharp, sustained drop in aggregate output. This optimal containment policy saves roughly half a million lives in the United States.”

John Rogers and co-authors find that in previous pandemics and epidemics in the 21st

Century real GDP was about 2½ % lower on average across 210 countries in the year the outbreak is officially declared and remained almost 3% below pre-shock level five years later. Fiscal policy responds aggressively to disease outbreaks, with initial year declines of 2% of GDP in the primary surplus on average. Countries that respond more aggressively through higher government expenditures suffer smaller declines in output growth compared to countries with less of a fiscal expenditures response.

They state that “it is difficult to translate these estimated historical effects to forecast the economic and financial effects of COVID-19. Although there are many parallels between these 21st century disease episodes and COVID-19, there is a lot to suggest that this pandemic will have a much larger toll on human lives. The unprecedented scale of lock downs in several countries will hamper economic activity even for countries that have lower caseloads and deaths and/or who thwart the virus more quickly … Thus, we consider our estimates to be a lower bound for the case of COVID-19.”

- Several macroeconomists—using evidence from previous pandemics or calculations based on economic models—have provided estimates of the likely impact of the coronavirus on the economy. They agree that the economic policies announced by governments, plus the containment and lockdowns, are a small price to pay to limit the deaths from COVID-19.

- In recent articles, Joseph Stiglitz, Robert Barro and the IMF all stress the importance of extending unemployment insurance benefits, maintaining the connections between companies and workers,

Posted by at 5:53 PM

Labels: Inclusive Growth

Sunday, March 15, 2020

Flattening the Pandemic and Recession Curves

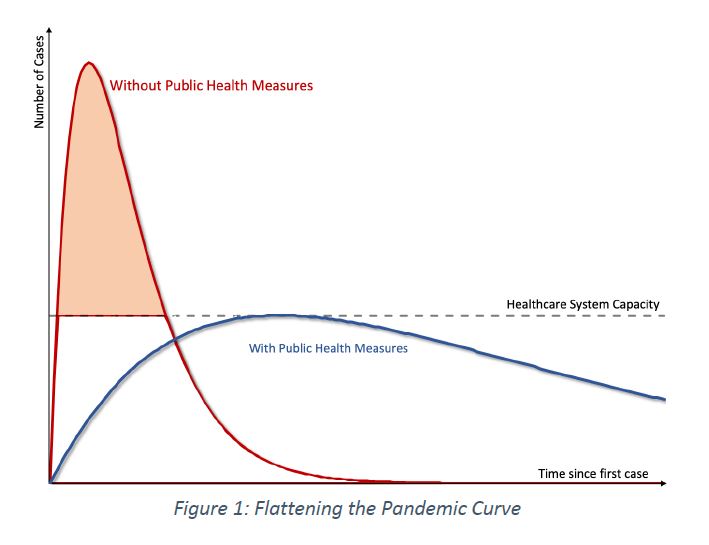

From an article by Pierre-Olivier Gourinchas (UC Berkeley):

“We are facing a joint health and economic crisis of unprecedented proportions in recent

history.I want to start by acknowledging that containment of the pandemic is the utmost priority.

Figure 1 summarizes how public health experts approach the problem.

In the short run, the capacity of any country’s health system is finite (capacity of Intensive Care Units, number of hospital beds, number of skilled health professionals, ventilators….). This puts an upper bound on the number of patients that can be properly treated, at any given point in time and is represented by the flat line in the Figure.

Unchecked, and given what we know of the transmission rate of the coronavirus, the pandemic would quickly overwhelm any health system, leaving many infected patients with deteriorating pulmonary conditions without any treatment. The fatality rate would surge. The threat is almost beyond comprehension. With a 2% case fatality rate baseline for overwhelmed health systems, and 50% of the world population infected, 1% of the world population -76 million people- would die. This scenario corresponds to the red curve in Figure 1. The part of the curve above the capacity of the health care system faces a sharply higher mortality risk (shaded red area).

Instead, public health policy, at least in all semi-decently run countries, aims to “flatten the

curve” by imposing drastic social distancing measures and promoting health practices to reduce the transmission rate. This ‘flattening of the curve’ would spread the pandemic over time, enabling more people to receive proper health treatment – ultimately lowering the fatality rate. This is the blue curve in Figure 1.”Continue reading here.

From an article by Pierre-Olivier Gourinchas (UC Berkeley):

“We are facing a joint health and economic crisis of unprecedented proportions in recent

history.

I want to start by acknowledging that containment of the pandemic is the utmost priority.

Figure 1 summarizes how public health experts approach the problem.

In the short run, the capacity of any country’s health system is finite (capacity of Intensive Care Units,

Posted by at 6:59 PM

Labels: Inclusive Growth

Coronavirus Response Should Include Urgent Fiscal Policy Measures to Address Financial Hardship, Stave Off a Severe Recession

From an article by Chye-Ching Huang and Chad Stone (both at Center on Budget and Policy Priorities):

“The COVID-19 pandemic demands an aggressive direct public health response to contain and treat the virus and strengthen health system capacity. Once policymakers enact legislation that House leaders are now negotiating with the Administration, Congress should move quickly to take further bold steps to achieve the dual and related aims of lessening the threat of a major recession and cushioning the financial blow for millions of Americans, including measures to shore up consumer purchasing power by addressing the loss of income that millions of workers likely will face in the period ahead.

With events involving large numbers of people being canceled and people increasingly avoiding travel, hotels, restaurants, and much more — and with the stock market’s rapid descent — recession looks extremely likely. Indeed, some economists have said that we likely are entering into recession now, and that substantial layoffs and business closures lie ahead. This makes it essential that policymakers act rapidly to take strong fiscal measures to lessen the damage, both to millions of Americans and to the overall economy.

The fiscal policy response should be both aggressive and quick-acting. Since even the fastestacting fiscal stimulus can still take some time to work its way into the economy, policymakers should act very swiftly. There is far more danger in doing too little, too late than too much, too soon.

Among the key sets of measures to institute are measures that can get resources into the hands of tens of millions of low and middle-income households, many of whom will be hit financially by the economic fallout of the pandemic. Doing that is one of the most effective and efficient ways to bolster the economy, as these households spend virtually all income they receive. But it’s only one of a number of steps that should be taken.”

Continue reading here.

From an article by Chye-Ching Huang and Chad Stone (both at Center on Budget and Policy Priorities):

“The COVID-19 pandemic demands an aggressive direct public health response to contain and treat the virus and strengthen health system capacity. Once policymakers enact legislation that House leaders are now negotiating with the Administration, Congress should move quickly to take further bold steps to achieve the dual and related aims of lessening the threat of a major recession and cushioning the financial blow for millions of Americans,

Posted by at 6:54 PM

Labels: Inclusive Growth

Friday, March 6, 2020

Operationalizing Inclusive Growth: Per-Percentile Diagnostics to Inform Redistribution Policies

A new IMF working paper by Alexei Kireyev and Andrei Leonidov;

“Inclusive growth, narrowly defined in this paper as growth that helps reduce inequality, is achieved if consumption of the poor increases faster than consumption of the rich. The paper presents a simple accounting framework for a per-percentile consumption diagnostics that could inform redistribution policies. The proposed framework is illustrated in application to Iraq and Tunisia.”

A new IMF working paper by Alexei Kireyev and Andrei Leonidov;

“Inclusive growth, narrowly defined in this paper as growth that helps reduce inequality, is achieved if consumption of the poor increases faster than consumption of the rich. The paper presents a simple accounting framework for a per-percentile consumption diagnostics that could inform redistribution policies. The proposed framework is illustrated in application to Iraq and Tunisia.”

Posted by at 4:52 PM

Labels: Inclusive Growth

Thursday, February 27, 2020

Mobility and Political Upheaval in an Age of Inequality

From a paper by Danny Quah:

“Appropriate public policy on inequality hinges critically on understanding inequality’s e ects on the living conditions of the poor, on social mobility, and on nationalist populism. This paper describes two empirical regularities. First, an increase in inequality typically does not coincide with immiserisation of the poor and lower middle class. Over 80% of economies where inequality has risen since 2000 have also increased the average incomes of their populations’ bottom 50%. Second, for political upheaval, individual well-being and expectations on its trajectory matter more than inequality. When these causal factors diverge, the role of inequality is, thus, diminished. Public policy needs to counter misinterpretation and misinformation on inequality with rigorous analysis and empirical evidence.”

From a paper by Danny Quah:

“Appropriate public policy on inequality hinges critically on understanding inequality’s e ects on the living conditions of the poor, on social mobility, and on nationalist populism. This paper describes two empirical regularities. First, an increase in inequality typically does not coincide with immiserisation of the poor and lower middle class. Over 80% of economies where inequality has risen since 2000 have also increased the average incomes of their populations’

Posted by at 8:52 AM

Labels: Inclusive Growth

Subscribe to: Posts