Showing posts with label Inclusive Growth. Show all posts

Tuesday, November 9, 2021

Modern Discourse on Inequality

“Today, wherever people live, they don’t have to look far to confront inequalities. Inequality in its various forms is an issue that will define our time.“

As the United Nations puts it, inequality of income, opportunity, and a variety of other factors is among matters of utmost importance to governments, multilateral institutions, and people at large today. Modern-day discussions on the theme seek to understand inequality by analyzing it through multiple lenses, discussing conflicting opinions, and contrasting approaches to tackle it.

In one such discussion presented underneath, economists David Green of the University of British Columbia and Parikshit Ghosh of Delhi School of Economics deliberate on factors influencing the state of inequality today such as trade and globalization, the gradual ideological shift to the ‘right’, changing nature of work – the role of technological advancements, hierarchies created by higher education, and ‘rents’ rather than returns to skill, and the new role of social protection that goes beyond income support.

The entire video can be accessed here.

On the other hand in their latest blog economists, Rohini Pande and Nils Enevoldsen discuss the salience of redistribution policies in poverty and inequality eradication. They contend that country-level catch-up in incomes will not be sufficient to eradicate extreme poverty, as the blessings of this ‘growth’ are not reaching the poor. Inclusive prosperity requires a political solution – redistribution.

Click here to read the full blog.

“Today, wherever people live, they don’t have to look far to confront inequalities. Inequality in its various forms is an issue that will define our time.“

As the United Nations puts it, inequality of income, opportunity, and a variety of other factors is among matters of utmost importance to governments, multilateral institutions, and people at large today. Modern-day discussions on the theme seek to understand inequality by analyzing it through multiple lenses,

Posted by at 1:40 PM

Labels: Inclusive Growth

Monday, November 8, 2021

Early Childhood Development, Human Capital Formation, and Poverty

” Children’s experiences during early childhood are critical for their cognitive and socio-emotional development, two key dimensions of human capital. However, children from low-income backgrounds often grow up lacking stimulation and basic investments, leading to developmental deficits that are difficult, if not impossible, to reverse later in life without intervention. The existence of these deficits are a key driver of inequality and contribute to the intergenerational transmission of poverty.”

This paper by Attanasio, Cattan, and Meghir for the NBER (2021), discusses models of parental investments and early childhood development and uses them as an organizing tool to review some of the empirical evidence on early childhood research. Among other things, results demonstrate that addressing development deficits doesn’t always have to be a costly policy affair. Incorporating conversations, playtimes, and reading into the pedagogy does wonders for cognitive development. Policies that are designed to target development delays must ensure scalability even in terms of cultural acceptability of interventions, rather than just cost minimization.

Click here to read the full paper.

” Children’s experiences during early childhood are critical for their cognitive and socio-emotional development, two key dimensions of human capital. However, children from low-income backgrounds often grow up lacking stimulation and basic investments, leading to developmental deficits that are difficult, if not impossible, to reverse later in life without intervention. The existence of these deficits are a key driver of inequality and contribute to the intergenerational transmission of poverty.”

This paper by Attanasio,

Posted by at 8:54 AM

Labels: Inclusive Growth

Saturday, November 6, 2021

Who Paid Los Angeles’ Minimum Wage? A Side-by-Side Minimum Wage Experiment in Los Angeles County

Who pays when minimum wage hikes come through the drawn-out demand-supply legislative processes?

This is precisely the question taken up by researchers Christopher Esposito of the University of Chicago and Edward Leamer and Jerry Nickelsburg of UCLA in an interesting working paper series. Drawing on a unique set of mandated wage hikes in the Los Angeles area, they present evidence that minimum wage changes led area restaurants to raise prices, change menu items, obtain lower rents in the high wage areas and, in some cases, caused eateries to shut down.

Results from the paper suggest that policymakers face an important dilemma when designing minimum wage policies to redistribute income while minimizing job loss. So, on one hand, restaurants in high-income neighborhoods studied by the authors passed on the full incidence of the minimum wage differential to their customers suggesting that minimum wages should be set relative to local income levels. The price passthrough channel for income redistribution is optimized when minimum wages are set uniquely for fine-grained spatial units, such as neighborhoods, within which the elasticity of demand for restaurant meals is homogenous. However, on the other hand, their findings also indicate that customers’ demand for restaurant meals can spill across jurisdictional borders with different minimum wages. Therefore, different minimum wages across fine-grained spatial units have the potential to move customer demand, jobs, and tax revenue out of jurisdictions that enact higher minimum wages. A universal minimum wage increase is not sensitive to this heterogeneity in the elasticity of demand, while minimum wage increases enacted at the neighborhood scale may cause restaurants to relocate out of higher-wage areas. The optimal spatial scale for setting minimum wages must balance these two offsetting forces.

In addition to these policy considerations, the study also raises the possibility that some of the incidence of minimum wage increases falls on landlords. The theoretical model predicts that land rents in regions subject to larger minimum wages will decrease, particularly at locations close to areas with lower minimum wages. This proposition is further strengthened because restaurant properties have specific use characteristics which are costly to change.

Click here to read the full explainer article/ full paper.

Source: Esposito et al. (2021). NBER. Who Paid Los Angeles’ Minimum Wage? A Side-by-Side Minimum Wage Experiment in Los Angeles County.

Who pays when minimum wage hikes come through the drawn-out demand-supply legislative processes?

This is precisely the question taken up by researchers Christopher Esposito of the University of Chicago and Edward Leamer and Jerry Nickelsburg of UCLA in an interesting working paper series. Drawing on a unique set of mandated wage hikes in the Los Angeles area, they present evidence that minimum wage changes led area restaurants to raise prices, change menu items,

Posted by at 11:00 AM

Labels: Inclusive Growth

Friday, November 5, 2021

Examining the role of Social Identity, Skills, and Personality in determining Labor Market Mobility in India

This study, by Michiels, Nordman, and Seetahul, combines behaviorist and structuralist views to understand the extent to which individual skills and personality traits facilitate labor market mobility of disadvantaged groups in the presence of constraining social structures.

Based on a rural India case study, results from this paper show that personality traits are important determinants of labor market mobility but also emphasize a strong rigidity of the socioeconomic structure of the Indian labor market in terms of gender and caste, and its relative stillness over time. While for women, literacy, emotional stability, and openness to new experiences appear to allow income gains, these benefits are limited by the labor market structure, maintaining them in low-skilled and casual occupations. For Dalits, emotional stability and agreeableness seem to play an important role in relative income mobility. These interesting findings highlight the segmented nature of the Indian labor market, which is still strongly organized by diverse forms of domination.

Source: Michiels et al. (2021). Many Rivers to Cross: Social Identity, Cognition, and Labour Mobility in Rural India. Institute of Labor Economics.

Click here to read the full paper.

This study, by Michiels, Nordman, and Seetahul, combines behaviorist and structuralist views to understand the extent to which individual skills and personality traits facilitate labor market mobility of disadvantaged groups in the presence of constraining social structures.

Based on a rural India case study, results from this paper show that personality traits are important determinants of labor market mobility but also emphasize a strong rigidity of the socioeconomic structure of the Indian labor market in terms of gender and caste,

Posted by at 9:28 AM

Labels: Inclusive Growth

Thursday, November 4, 2021

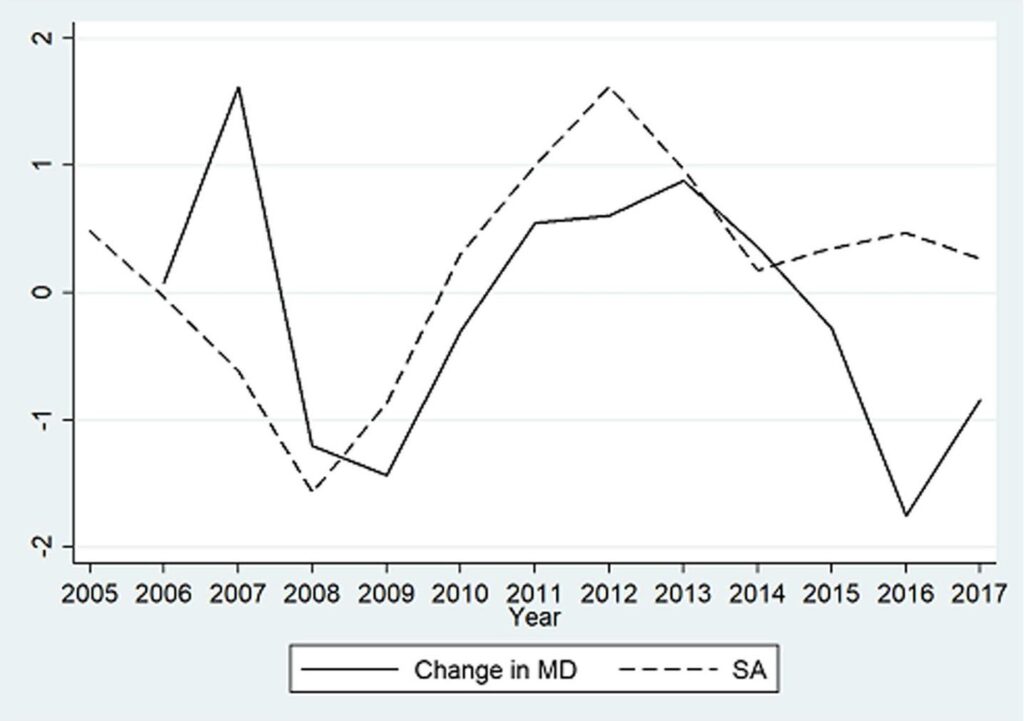

Absolute Poverty and Sound Public Finance in the Eurozone

“In this paper, the relation between structural public balance adjustment and absolute poverty in 19 Eurozone countries during the time span 2005–2017 has been investigated. Absolute poverty is becoming more and more relevant in advanced economies, and due to its non-country-specific nature, it allows for a more accurate comparison among countries with very different GDP levels, which also belong to the same economic area. Structural public balance adjustments represent the tool that individual countries must use to contain their deficit and debt within the threshold.

The empirical estimates presented in this paper allow us to support the conclusion that structural public balance adjustments have a direct relation with absolute poverty and that restrictive fiscal measures increase material deprivation, while expansive measures decrease it. In line with the recent debate on the efficacy of fiscal policy, this is the result of the effects of government expenditure on growth that the eventual presence of redistributive measures has not been able to counteract. The introduction in the estimates of other variables affecting poverty consolidates the results and indicates, as additional causes, the rate of inflation and trade openness. Further estimates were conducted on a reduced sample of 12 EMU countries for a longer period (1995–2017) and for the two subsamples of pre (1995–2008) and post (2009– 2017) crisis period using a dependent variable indicator of monetary poverty confirm the

existence of a direct relation between structural adjustments and the share of population living in awkward social conditions.

However, inside the European policy framework, national policies are constrained in their ability to implement autonomously fiscal policies. In the absence of a sustained rate of growth, the interaction among fiscal policy stance, government bonds yields and capital flows limits any kind of single states intervention in the fear of interest rates increase (Canale et al. 2018). Therefore, whatever their aims, national governments are very limitedly able to reconcile the objective of poverty alleviation with that of sound public finance. The increase in poverty is perceived as a kind of unavoidable consequence of fiscal profligacy.”

Source: Canale, R and Liotti, G. (2021). Absolute Poverty and Sound Public Finance in the Eurozone. Journal of Economic Inequality.

Click here to read the full paper.

“In this paper, the relation between structural public balance adjustment and absolute poverty in 19 Eurozone countries during the time span 2005–2017 has been investigated. Absolute poverty is becoming more and more relevant in advanced economies, and due to its non-country-specific nature, it allows for a more accurate comparison among countries with very different GDP levels, which also belong to the same economic area. Structural public balance adjustments represent the tool that individual countries must use to contain their deficit and debt within the threshold.

Posted by at 3:18 PM

Labels: Inclusive Growth

Subscribe to: Posts