Showing posts with label Inclusive Growth. Show all posts

Wednesday, January 5, 2022

Global services value chains: A new path to development

Source: VoxEU CEPR

“The role of global value chains for development is often told from a manufacturing or agriculture perspective. This column discusses how the rise of global services value chains offers developing countries with new opportunities by providing jobs, revenue, and productivity growth. In addition, they do so in a more inclusive way than manufacturing. Policymakers need to invest in human capital and address regulatory barriers to services trade to make the most of this development.”

It draws examples of the Indian software services industry and business process outsourcing services in Philippines to expand on the idea of countries joining service GVCs. They find insights about themes like spillover benefits from trade in services and evidence about the relationship between trade and employment in the sector.

Click here to read the full blog.

Related Reads:

Source: VoxEU CEPR

“The role of global value chains for development is often told from a manufacturing or agriculture perspective. This column discusses how the rise of global services value chains offers developing countries with new opportunities by providing jobs, revenue, and productivity growth. In addition, they do so in a more inclusive way than manufacturing. Policymakers need to invest in human capital and address regulatory barriers to services trade to make the most of this development.

Posted by at 10:09 AM

Labels: Inclusive Growth

Monday, January 3, 2022

Correlates of declining income inequality in emerging and developing nations

In an upcoming publication for World Development titled, ‘The correlates of declining income inequality among emerging and developing economies during the 2000s’ (2022), author Edward Anderson of the University of East Anglia discusses patterns that were frequently observed in countries that experienced declining levels of income inequality.

Among the most significant results of the paper, one states that “the tendency toward declining inequality in the 2000s was stronger in countries with higher initial levels of inequality and larger increases in relative agricultural productivity, country-specific primary commodity prices, and remittance inflows.” (Furceri and Loungani, 2018) “The results suggest that the challenge now facing many emerging and developing countries is how to sustain the reductions in inequality achieved since the early 2000s, given the decline in commodity prices since 2015, and the social and economic repercussions of the COVID-19 pandemic”, the paper adds.

Click here to read the full paper.

In an upcoming publication for World Development titled, ‘The correlates of declining income inequality among emerging and developing economies during the 2000s’ (2022), author Edward Anderson of the University of East Anglia discusses patterns that were frequently observed in countries that experienced declining levels of income inequality.

Among the most significant results of the paper, one states that “the tendency toward declining inequality in the 2000s was stronger in countries with higher initial levels of inequality and larger increases in relative agricultural productivity,

Posted by at 12:16 PM

Labels: Inclusive Growth

Sunday, January 2, 2022

The new consensus of economists is further to the left

They say economists rarely agree on one thing.

However, now this statement may not hold true as before. Based on a survey of members of the American Economic Association, a paper by Doris Geide-Stevenson and Alvaro La Parra Perez of the Weber State University compares the academic positions of economists over four decades.

“The main result is an increased consensus on many economic propositions, specifically the appropriate role of fiscal policy in macroeconomics and issues surrounding income distribution. Economists now embrace the role of fiscal policy in a way not obvious in previous surveys and are largely supportive of government policies that mitigate income inequality. Another area of consensus is concern with climate change and the use of appropriate policy tools to address climate change.”

Click here to download the paper and here to be a part of the discussion on it.

They say economists rarely agree on one thing.

However, now this statement may not hold true as before. Based on a survey of members of the American Economic Association, a paper by Doris Geide-Stevenson and Alvaro La Parra Perez of the Weber State University compares the academic positions of economists over four decades.

“The main result is an increased consensus on many economic propositions, specifically the appropriate role of fiscal policy in macroeconomics and issues surrounding income distribution.

Posted by at 10:33 AM

Labels: Inclusive Growth, Macro Demystified

Friday, December 31, 2021

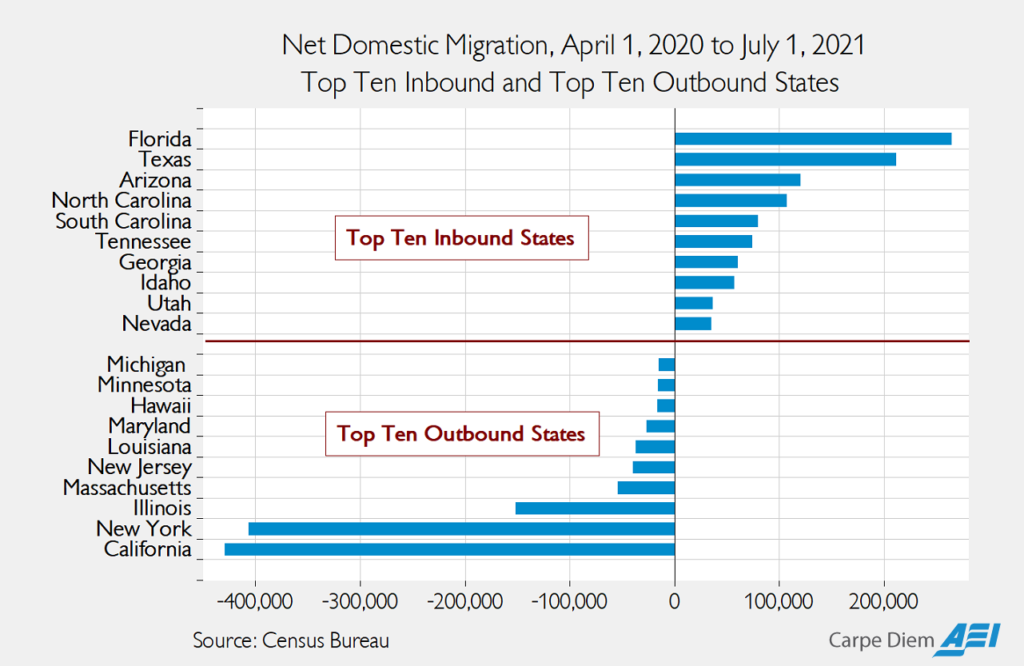

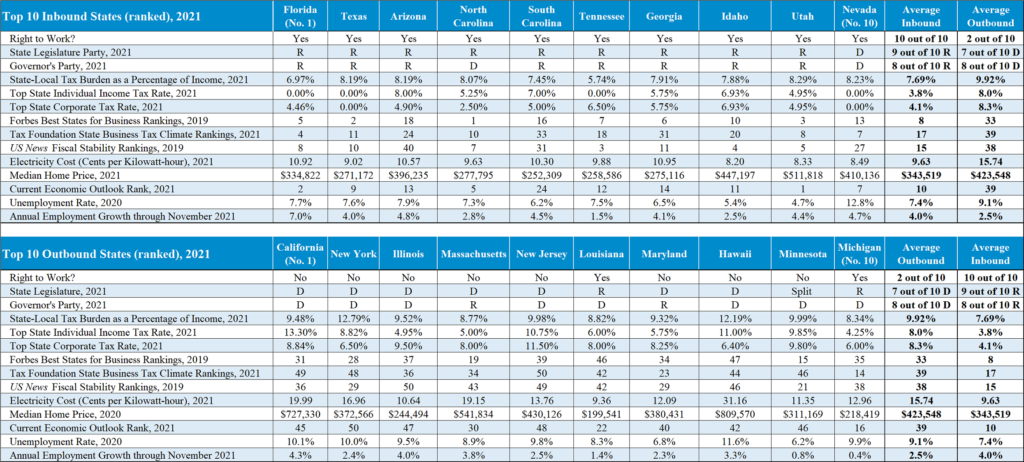

Moving on up? Understanding migration to red states in 2021

In a column for the public policy think tank, American Enterprise Institute, the top ten inbound and top ten outbound US states for the year 2021 have been compared using new data on net domestic migration data from the US Census Bureau.

Click here to read the full report.

In a column for the public policy think tank, American Enterprise Institute, the top ten inbound and top ten outbound US states for the year 2021 have been compared using new data on net domestic migration data from the US Census Bureau.

Source: American Enterprise Institute

Source: American Enterprise Institute

Click here to read the full report.

Posted by at 1:08 PM

Labels: Inclusive Growth

Wednesday, December 29, 2021

Inequality in India Declined during COVID

In a paper for the National Bureau of Economic Research, authors Arpit Gupta of NYU Stern School of Business, and Anup Malani and Bartosz Woda of the University of Chicago Law School write about inequality in India during the COVID-19 pandemic. The abstract of the paper is as follows:

“We use a large, representative panel data set from India with monthly data on household finances to examine the incidence of economic harms during the COVID pandemic. We observe a sharp spike in poverty, peaking during India’s sharp but short lockdown. However, there was a striking decrease in income inequality outside the lockdown. There was a smaller decrease in consumption inequality, likely due to consumption smoothing. Evidence supports two mechanisms for the decline in income inequality: the capital income of top-quartile earners covaries more with aggregate income, and demand for labor fell more for higher quartiles.”

Click here to read the full paper.

In a paper for the National Bureau of Economic Research, authors Arpit Gupta of NYU Stern School of Business, and Anup Malani and Bartosz Woda of the University of Chicago Law School write about inequality in India during the COVID-19 pandemic. The abstract of the paper is as follows:

“We use a large, representative panel data set from India with monthly data on household finances to examine the incidence of economic harms during the COVID pandemic.

Posted by at 9:41 AM

Labels: Inclusive Growth

Subscribe to: Posts