Showing posts with label Inclusive Growth. Show all posts

Thursday, August 2, 2012

Is Long-Term Unemployment Pushing Up Structural Unemployment?

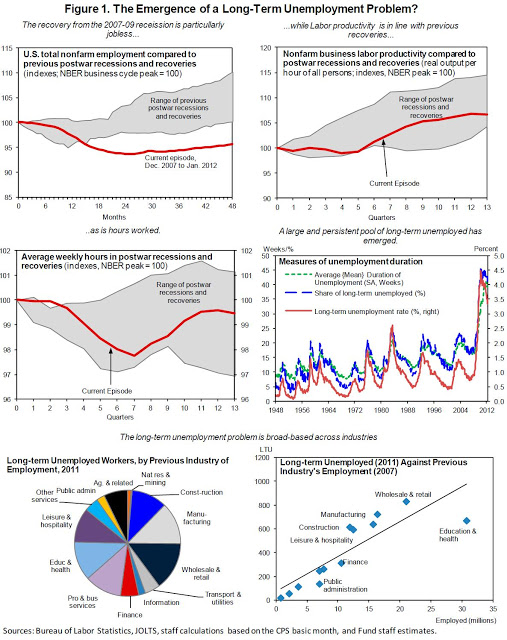

A new IMF report on US structural unemployment says that

while high long-term unemployment has not yet morphed into a permanent structural problem, it does pose an upward risk to the structural rate of unemployment. We have found that long-term unemployed are significantly less likely to find a job now than before the crisis, and that the loss in labor market matching efficiency observed since the recession is entirely due to a worsening of the labor matching of the long-term unemployed. Together, these results point to a risk that the structural rate of unemployment might be greater now than before the crisis.

Hence, forceful measures should be introduced that reduce long-term unemployment and address the risks associated with long spells of unemployment, namely skills erosion and a weaker attachment to the labor force. These measures include policies to increase demand for the long-term unemployed in the short run (active labor market policies, ALMP). When appropriately designed, such policies have been shown to be effective in improving employment and earnings prospects of long-term unemployed workers (Card et al, 2010; Card and Levine, 2000; Heinrich et al., 2008; Hotz et al., 2006). In particular, as discussed in the Staff report, a significant increase in ALMP resources is warranted given the persistently large pool of long-term unemployed and the risk that, as duration lengthens, their skills and attachment to the workforce might erode. Indeed, in terms of resources per long-term unemployed, the United States spends relatively little on active labor market policies, both compared to other OECD countries, and relative to its own pre-recession levels.

A new IMF report on US structural unemployment says that

while high long-term unemployment has not yet morphed into a permanent structural problem, it does pose an upward risk to the structural rate of unemployment. We have found that long-term unemployed are significantly less likely to find a job now than before the crisis, and that the loss in labor market matching efficiency observed since the recession is entirely due to a worsening of the labor matching of the long-term unemployed.

Posted by at 3:34 PM

Labels: Inclusive Growth

Thursday, July 26, 2012

Successful Austerity in the United States, Europe and Japan

According to a new IMF working paper:

The large fiscal legacies of the global financial crisis have reignited the debate around the impact of fiscal policy onto economic activity during fiscal consolidations. The analysis in this paper shows that withdrawing fiscal stimuli too quickly in economies where output is already contracting can prolong their recessions without generating the expected fiscal saving. This is particularly true if the consolidation is centred around cuts to public expenditure—likely reflecting the fact that reductions in public spending have powerful effects on the consumption of financially-constrained agents in the economy—and if the size of the consolidation is large. Large consolidations make recessions more likely even when made at an expansion time. From a policy perspective this is especially relevant for periods of positive, though low growth. Accordingly, frontloading consolidations during a recession seems to aggravate the costs of fiscal adjustment in terms of output loss, while it seems to greatly delay the reduction in the debt-to-GDP ratio—which, in turn, can exacerbate market sentiment in a sovereign at times of low confidence, defying fiscal austerity efforts altogether. Again this is even truer in the case of consolidations based prominently on cuts to public spending.

Thus, a gradual fiscal adjustment, with a balanced composition of cuts to expenditure and tax increases boosts the chances that the consolidation will successfully (and rapidly) translate into lower debt-to-GDP ratios. Monetary policy can likely help alleviate further the pain of fiscal withdrawal if it is used proactively via reduction in the real interest rate.

According to a new IMF working paper:

The large fiscal legacies of the global financial crisis have reignited the debate around the impact of fiscal policy onto economic activity during fiscal consolidations. The analysis in this paper shows that withdrawing fiscal stimuli too quickly in economies where output is already contracting can prolong their recessions without generating the expected fiscal saving. This is particularly true if the consolidation is centred around cuts to public expenditure—likely reflecting the fact that reductions in public spending have powerful effects on the consumption of financially-constrained agents in the economy—and if the size of the consolidation is large.

Posted by at 7:45 PM

Labels: Inclusive Growth

Monday, June 11, 2012

Unemployment: Cyclical or Structural?

Eric Swanson reports on the San Francisco Fed macro conference:

“Breaking down changes in output or employment into structural and cyclical components is very difficult, since these elements are not directly observable. Two papers at the conference applied cutting-edge methods to this question, providing estimates of the structural and cyclical components of the 2007–09 recession’s large employment and output declines.

Chen, Kannan, Loungani, and Trehan use differences in stock market returns across industries to help identify the magnitudes of cyclical and structural shocks to the economy … Chen and coauthors collected cross-industry stock return data from 1962 to 2011, which they use to construct an index of stock return dispersion across industries. The authors then estimate the typical response of output and employment to sudden changes in this index, providing an approximation to the effects of structural shifts on the economy. The authors find that such structural shifts account for about 25% of U.S. output and employment fluctuations since 1962. The remaining 75% is due to cyclical factors.”

Read the rest of Swanson’s excellent summary here. The Chen, Kannan, Loungani and Trehan paper is available here.

Eric Swanson reports on the San Francisco Fed macro conference:

“Breaking down changes in output or employment into structural and cyclical components is very difficult, since these elements are not directly observable. Two papers at the conference applied cutting-edge methods to this question, providing estimates of the structural and cyclical components of the 2007–09 recession’s large employment and output declines.

Chen, Kannan, Loungani, and Trehan use differences in stock market returns across industries to help identify the magnitudes of cyclical and structural shocks to the economy … Chen and coauthors collected cross-industry stock return data from 1962 to 2011,

Posted by at 6:47 PM

Labels: Inclusive Growth

Wednesday, June 6, 2012

Seven Questions about Income Inequality

A recent flurry of media and academic attention toward rising inequality across the world has generated a tremendous amount of research on inequality trends and their causes and consequences. While some of the hype on the topic is warranted, the large and expanding literature has made it difficult to sift out the main facts. These seven questions attempt to highlight the basic points made by the recent literature.

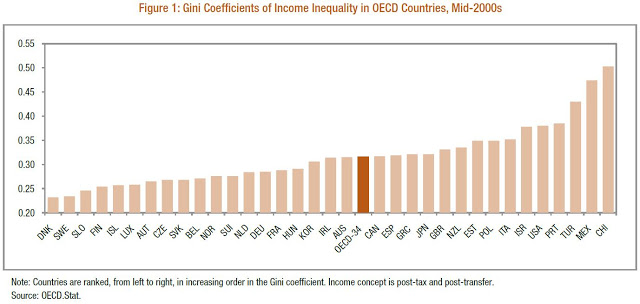

Question 1: What is the basic measurement of income inequality?

The most common way to measure inequality is the Gini coefficient, which is an index that ranges from zero to one, with a value of zero corresponding to equal incomes across all recipients and a value of one corresponding to a situation in which one household receives all of the income in the economy. As Figure 1 shows, the Gini coefficient varies substantially across countries.

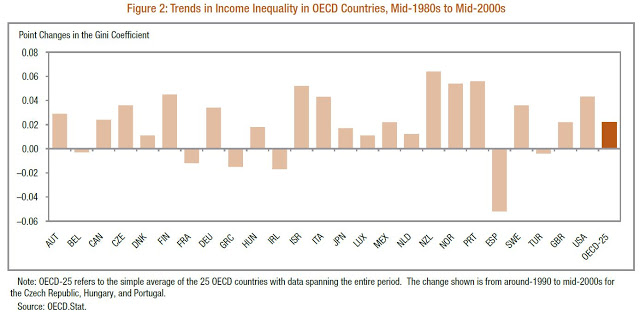

Question 2: How much has income inequality increased over the past few decades?

Question 3: What has caused this rise in income inequality?

Skilled-based technological change is thought to be one of the leading causes driving the increase in inequality in advanced economies over the past four decades. The middle class has been “hollowed out” as machines have replaced medium-skilled labor (Acemoglu and Autor, 2011). More recently, another economic change that has contributed to the decline of middle-income jobs in developed countries is the increase of globalization. As medium-skilled jobs move off-shore, the replaced workers must face a decision of increasing their education to obtain higher-paying jobs or to move to lower-paying jobs. This effect has become more prominent in the 2000s than it had been in the preceding decades (Autor, Dorn, Hansen, 2011). Two other possible contributors to the increase in income inequality are the decline of unions and the decline of the real minimum wage in many advanced economies. Historically, unions have affected the wage structure by boosting the wages of lower middle class workers (Card, 2001). In the United States, the percent of private sector workers covered by unions has decreased from more than 20 percent in the mid-1970s to less than 10 percent in 2010. At the same time, since the nominal minimum wage has not increased in step with inflation, the real minimum wage has decreased in many countries, contributing to the decline of real wages of the lowest income quintile. Furthermore, the increase of immigration and the use of illegal immigrant labor have weakened unions and the application of the minimum wage. Finally, an important factor in the rise in inequality has been the emergence of a powerful financial sector. A substantial portion of the rise in income inequality has been due to the increase in the share of income accruing to the top 1 percent of the income distribution (Atkinson, Piketty, and Saez, 2011). This rise is at least partially due to a dramatic increase in salaries in the financial sector which, in turn, can be attributed to the structure of the financial system and its associated incentives.

Question 4: What are the possible negative consequences of the rise in income inequality?

Recent research has shown that societies with high inequality tend to adopt policies that hinder long-term growth potential, due to conflicts between the holders of economic power and political power (Berg and Ostry, 2011). In addition, these societies face short-term destabilizing influences. High levels of inequality may increase the competition between income earners. Lower earners feel social pressure to borrow, if possible, in order to maintain a consumption level that approaches that of their wealthier neighbors. The overleveraging that might follow can lead to macroeconomic instability and is thought to be one of the causes of the recent recession (Rajan, 2010). The welfare considerations of high inequality extend past the effect on growth and macroeconomic stability. One broad negative consequence of a rise in inequality is an increased stratification of society. The emergence of a class society is bad for social and health outcomes as people are faced with the pressures associated with dramatically different living situations (Pickett and Wilkinson, 2009). High inequality tends to be associated with lower intergenerational mobility, implying

that these pressures and their negative consequences mayhave lasting effects on future generations (Corak, 1993).

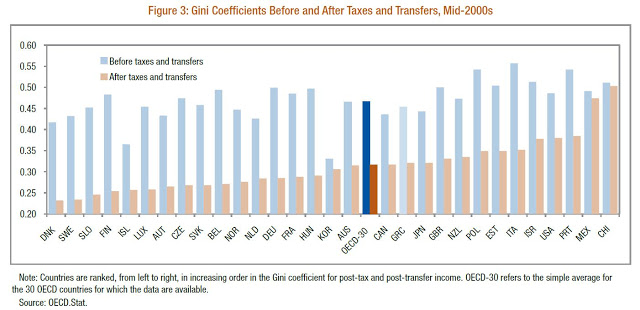

Question 5: How can governments intervene in order to stem inequality?

The most direct way for governments to intervene is to implement progressive tax and transfer policies. As Figure 3 shows, governments in OECD countries vary substantially in how successful their policies are in reducing inequality. In addition to the direct monetary redistribution programs, a government’s involvement in equalizing the access to services, such as education, health care, and technology, can have medium- to long-run success in narrowing the income distribution. Furthermore, regulation of the minimum wage and low-income labor policies can help to boost the earnings of the workers on the low end of the distribution. Lastly, the government may have a role in regulating the financial sector, as mentioned in Question 3.

Question 6: Why the focus on income inequality? Are there other measures that are more meaningful?

The focus on income inequality largely has to do with the availability of data, even while other measures may better capture welfare concerns. Income inequality may exaggerate the disparities in actual consumption; high income individuals tend to save more and consume less of their income at the same time that public provision of education, health care and other services further narrows the consumption gap between the rich and the poor. Furthermore, higher levels of consumption lead to decreasing rates of marginal utility; with this in mind, happiness inequality may be the closest measure to capturing welfare, yet is also one of the most elusive to measure (Stevenson and Wolfers, 2008). Other types of inequality measures also have their own merits: wealth disparities, differential access to services, and the spread in lifetime earnings. Some economists argue that the percentage of the population in poverty is more relevant than any measure of inequality. Ultimately, the “correct” measure depends on the specificwelfare question of interest.

Question 7: Are any of the concerns about the rise in inequality overstated?

There are potentially dramatic welfare implications surrounding the recent increases in inequality in advanced economies. However, some of the concerns highlighted in the media are almost certainly overblown. In a world in which social media makes the emergence of celebrities and mass-marketed products possible, there is more of an opportunity for superstars to amass tremendous amounts of income than there had been earlier in the twentieth century. Furthermore, as economies get richer, more workers choose to curtail their hours in exchange for more leisure; in doing so, an income gap is automatically generated between the average “threshold” worker and those who have a taste for working longer hours for a higher monetary reward (Cowen, 2011). It is questionable whether these contributions to the spread of the income distribution have either negative welfare or growth implications. While it may be difficult to distinguish a destructive rise in income inequality from a positive rise that naturally occurs as a country gets richer, it is important to keep in mind that the goal of reducing inequality is not to hurt the rich at the expense of the poor.

A recent flurry of media and academic attention toward rising inequality across the world has generated a tremendous amount of research on inequality trends and their causes and consequences. While some of the hype on the topic is warranted, the large and expanding literature has made it difficult to sift out the main facts. These seven questions attempt to highlight the basic points made by the recent literature.

Question 1: What is the basic measurement of income inequality?

Posted by at 8:18 PM

Labels: Inclusive Growth

Labor Markets through the Lens of the Great Recession

Call for Papers

The International Monetary Fund will hold the Thirteenth Jacques Polak Annual Research Conference at its headquarters in Washington DC on November 8-9, 2012.

The conference is intended to provide a forum for discussing innovative research in economics, undertaken by both IMF staff and by outside economists, and to facilitate the exchange of views among researchers and policymakers. Peter Diamond (MIT) will deliver the Mundell-Fleming lecture.

The theme of the conference is “Labor Markets through the Lens of the Great Recession.” The Program Committee welcomes papers that investigate the lessons of the crisis for labor market dynamics, as well as short-run and long-run policy challenges concerning employment growth and structural changes in labor markets in industrial and developing economies. Possible topics include (without being exclusive):

Comparative performance of labor markets in the crisis:

- Output, participation, employment, unemployment

- Variations in Okun’s law across countries

- The age and skill distribution of unemployment

- The role of labor market institutions

- Policy measures, employment, unemployment

- Fiscal policies, output and employment

- Hysteresis in unemployment

- Informal employment and links to growth and financial frictions

Unemployment and the Arab spring

- Wage distributions, inequality, and political economy implications

- Globalization and wage distributions

- Technological progress and wage distributions

- Role and limits of redistribution

Reforms, employment, and unemployment

- Short and long-term effects of labor market reforms

- Short and long-term effects of product market reforms

Please submit a proposal (in Word or PDF format), which should be no shorter than two pages and no longer than five pages by June 8, 2012 (e-mail to ARC@imf.org). Please use the contact author’s name as the name of the file. The Program Committee will evaluate all proposals in terms of originality, analytical rigor, and policy relevance and will contact the authors whose papers have been selected by June 30, 2012. A 15-page work-in-progress draft will be required by August 15, 2012. Further information on the conference program will be posted on the IMF website (www.imf.org).

Call for Papers

The International Monetary Fund will hold the Thirteenth Jacques Polak Annual Research Conference at its headquarters in Washington DC on November 8-9, 2012.

The conference is intended to provide a forum for discussing innovative research in economics, undertaken by both IMF staff and by outside economists, and to facilitate the exchange of views among researchers and policymakers. Peter Diamond (MIT) will deliver the Mundell-Fleming lecture.

The theme of the conference is “Labor Markets through the Lens of the Great Recession.” The Program Committee welcomes papers that investigate the lessons of the crisis for labor market dynamics,

Posted by at 7:43 PM

Labels: Inclusive Growth

Subscribe to: Posts