Showing posts with label Inclusive Growth. Show all posts

Monday, July 25, 2016

Jobs and Growth: The Evolution in IMF Research

Here are links to my talk and PPT at a ETUI conference. And here’s a two-minute video summary of what I said.

Here are links to my talk and PPT at a ETUI conference. And here’s a two-minute video summary of what I said.

Posted by at 2:22 PM

Labels: Inclusive Growth

Tuesday, July 12, 2016

What Keeps France’s Unemployment High?

Structural unemployment in France has long been elevated, and appears to have edged up further since the crisis. This reflects both demand and supply factors, including: high labor taxes, wage stickiness, a growing skill gap, hysteresis effects from the crisis years, a lengthy period of elevated economic uncertainty, inactivity traps created by the unemployment and welfare benefit systems, and demographic factors that have pushed up the labor force. The cyclical recovery is projected to bring down the unemployment rate only slowly, and the NAIRU is estimated to remain above 8 percent over the medium term. We investigate the structural causes of unemployment and potential remedies.

Reducing labor tax wedges can increase both output and employment. In France, CICE, PRS and other recent reforms have reduced the labor tax wedge for the low-paid workers. The wedge remains elevated for middle and upper incomes, but further reductions would require difficult policy trade-offs given the high level of public spending.

Strictness of employment protection in France is above the EU average. Labor arbitration procedures are cumbersome and allow making an appeal for a very long time after dismissal, which adds to uncertainty for companies. Reforms easing dismissal regulations could have a sizable positive impact on output and employment when economic conditions are strong. Early studies suggest that the proposed “El Khomri” law, by reducing judicial uncertainty around dismissals, could have a moderate impact on overall unemployment, while stimulating hiring on open-ended (CDI) contracts as opposed to temporary recruitment (on CDD).

Efficiency of collective bargaining depends on flexibility at the firm level, the reach of sector-level agreements, and the effectiveness of coordination among agents. IMF research suggests that France can be classified among countries with “low trust” and “some coordination”, which entails poor unemployment outcome. In France, trade unions play a leading role in collective negotiations even though membership is low. The El Khomri law would extend the scope for firm-level collective agreements.

While the replacement rate of unemployment benefits in France is broadly in line with other countries, eligibility criteria are relatively lax, with rapid qualification and accumulation of benefit rights, and weak job search requirements. Moreover, specificities of the benefit formula create incentives for alternating between ultra-short contracts and unemployment periods.

The ratio of minimum to median wage in France is among the highest in the OECD, which may adversely affect job market chances for the young, the low-skilled, and the long-term unemployed. Its automatic annual adjustment can contribute to wage stickiness.

A detailed analysis by my IMF colleague Nicoletta Batini.

Structural unemployment in France has long been elevated, and appears to have edged up further since the crisis. This reflects both demand and supply factors, including: high labor taxes, wage stickiness, a growing skill gap, hysteresis effects from the crisis years, a lengthy period of elevated economic uncertainty, inactivity traps created by the unemployment and welfare benefit systems, and demographic factors that have pushed up the labor force.

Posted by at 12:28 PM

Labels: Inclusive Growth

Saturday, July 9, 2016

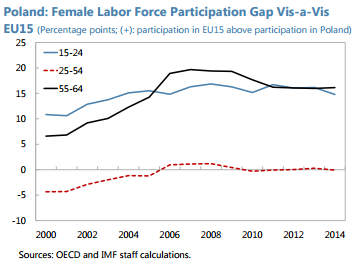

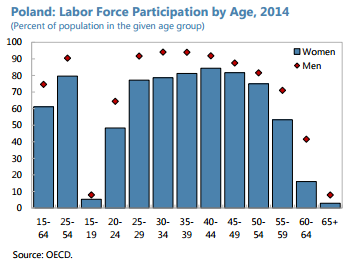

Female Labor Force Participation in Poland

An IMF report notes: “Poland is facing a rapidly aging population, which is expected to weigh on public finances and economic growth. Yet, there is an important underutilized source of qualified labor—Poland’s women. Women in Poland are on average just as educated as men and have a longer potential working lifespan. Nonetheless, female labor force participation is low relative to that for men and low relative to that in many other European countries. Unlocking this valuable source of growth would require leveling the playing field between men and women in the workplace, including by providing high quality affordable childcare for young children, removing tax disincentives for the second earner in a family, and allowing the retirement age to increase as envisaged by the 2013 reforms. For Poland to unleash its full economic potential, it needs to embrace the vital contribution that women can make to its economy.”

An IMF report notes: “Poland is facing a rapidly aging population, which is expected to weigh on public finances and economic growth. Yet, there is an important underutilized source of qualified labor—Poland’s women. Women in Poland are on average just as educated as men and have a longer potential working lifespan. Nonetheless, female labor force participation is low relative to that for men and low relative to that in many other European countries.

Posted by at 6:26 AM

Labels: Inclusive Growth

Thursday, July 7, 2016

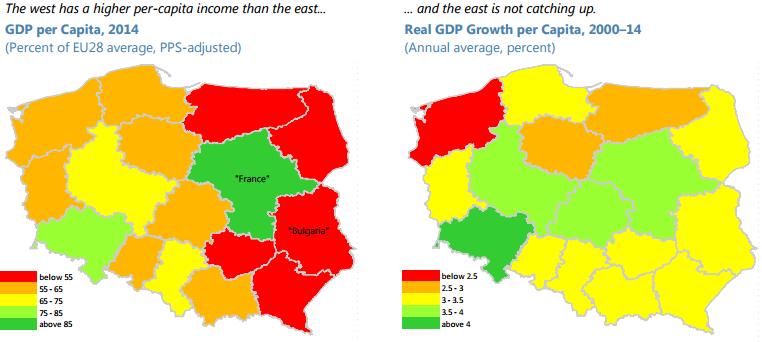

The Role of Productivity Growth in Reducing Regional Economic Disparities in Poland

Below are extracts from a report written by IMF colleagues: Krzysztof Krogulski, Robert Sierhej, and Aaron Thegeya.

Although Poland has enjoyed strong growth and steady income convergence with the EU over the last two decades, important disparities persist at the regional level. Per-capita income is higher in the west—which is integrated into the German supply chain and enjoys higher levels of FDI—than in the east—where the economy depends more on less productive agriculture. Despite strong overall economic growth, the east has not been catching up to the west. This chapter identifies policies to increase productivity in the east, reduce regional income disparities, and promote overall income convergence. This would require improving educational attainment and reducing skill mismatches in the east, scaling up public infrastructure to attract investment to less productive regions, and facilitating labor mobility.

Despite strong economic performance over the last two decades, there are significant and enduring income disparities between western and eastern regions of Poland. These disparities are strongly correlated with labor productivity differences. While labor productivity growth in poorer eastern regions has been driven significantly by structural transformation, in wealthier western regions it has been driven by higher investment and integration with the German supply chain. Education and labor market conditions had a significant impact on labor productivity growth across regions. Similar growth rates in labor productivity across regions have prevented eastern regions from catching up to western regions.

The analysis of regional productivity determinants points to policies that could be conducive to regional productivity convergence.

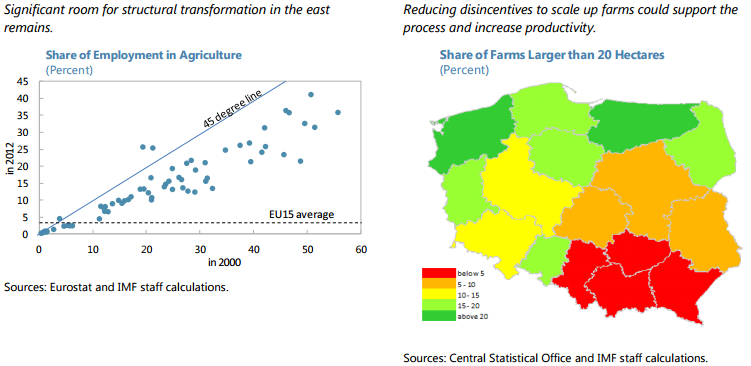

- Support structural transformation and boost productivity in agriculture: Significant room remains to boost labor productivity growth within poorer regions by supporting the reallocation of labor from low-productivity agriculture to higher-productivity industry and service sectors. To unleash the potential for such structural transformation, a review of incentives pertaining to employment in agriculture would be appropriate to identify mechanisms that may encourage people to stay in low productivity farms. In particular, the highly subsidized pension scheme for farmers could be reformed to gradually align it with the regular system to discourage inefficient farming motivated by pension arbitrage. The more productive farms in western regions tend to be larger, so there may be merit in promoting consolidation of agricultural production also in the poorer eastern regions to exploit the economies of scale. In this regard, moving from the current agricultural taxation based on farm size and quality of land to an income-based tax would reduce disincentives to scale up farms and help define the base for social security contributions. To facilitate structural transformation, such reforms should be accompanied with measures to address skill mismatches and bottlenecks in labor mobility, as described below.

- Encourage labor mobility and reduce structural unemployment: Decomposition of productivity growth shows that the contribution from reallocating labor across regions has been relatively minor. This suggests bottlenecks in labor market mobility that could be addressed with proper policies, for example, by improving the functioning of the housing rental market. Currently, the rental housing market in Poland is shallow, discouraging labor relocation. Econometric analysis also suggests that high structural unemployment negatively affects regional productivity growth. While a declining working age population should generally reduce the unemployment rate, addressing high structural unemployment in less productive regions would require greater investment in active labor market policies to improve job searching efficiency across regions, upgrade skills, and reduce skill mismatches.

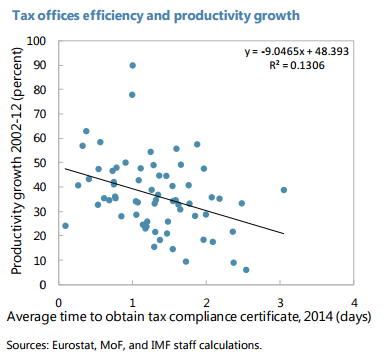

- Attract investments to less productive regions: Empirical findings show that higher FDI is associated with faster regional productivity growth. FDI is more prevalent in wealthier regions, and this pattern needs to change to support regional productivity catch-up. Some factors important for investors could be altered by government policies to support such a change. Specifically, strengthening transportation networks in poorer regions would help, and better targeting of EU funds could support this process. Furthermore, investor surveys suggest that access to skilled labor is important for location of projects. In this context, investing in education and tailoring it to local development needs is important; aligning vocational curricula closely to the needs of industry would facilitate the absorption of new production methods and technologies. While local governments’ role in boosting productivity appears less statistically significant, it does not imply that quality of local administration is irrelevant. For example, data suggest a positive correlation between regional productivity and the efficiency of local tax administration.

Below are extracts from a report written by IMF colleagues: Krzysztof Krogulski, Robert Sierhej, and Aaron Thegeya.

Although Poland has enjoyed strong growth and steady income convergence with the EU over the last two decades, important disparities persist at the regional level. Per-capita income is higher in the west—which is integrated into the German supply chain and enjoys higher levels of FDI—than in the east—where the economy depends more on less productive agriculture.

Posted by at 11:13 AM

Labels: Inclusive Growth

Tuesday, April 12, 2016

Openness, Austerity and Inequality

My talk at Bielefeld University at a workshop on inequality.

Posted by at 2:05 PM

Labels: Inclusive Growth

Subscribe to: Posts